Buy Now Pay Later: Meaning, Benefits, And Risks In India

Riya was stressed as she talked on the phone. “My laptop broke, and I need it urgently for work. I don’t have the cash right now, as it’s the end of the month.” On the other end, her brother Karan sighed. “I wish I could help, Riya, but I’m stuck too. Rent, bills, everything’s already lined up.” Then he spoke again. “Wait. Have you checked if there’s a Buy Now, Pay Later option?” Riya hesitated. “BNPL? Isn’t that risky?”

“Only if you misuse it,” Karan replied. “This is exactly the kind of situation it’s meant for. You can handle the emergency without needing cash immediately and pay it back once your salary comes in.” Riya thought for a moment and said, “That actually makes sense. By using it, I won't have to postpone work or borrow money.” “Exactly,” Karan said. “Just make sure you choose a plan you can comfortably repay.”

The help Riya got from BNPL is real, and in such situations, a blessing as well. But that doesn’t change the fact that BNPL can be quite risky if used recklessly. Without careful use, it can quickly turn into a crushing cycle of buy now pay later EMI.

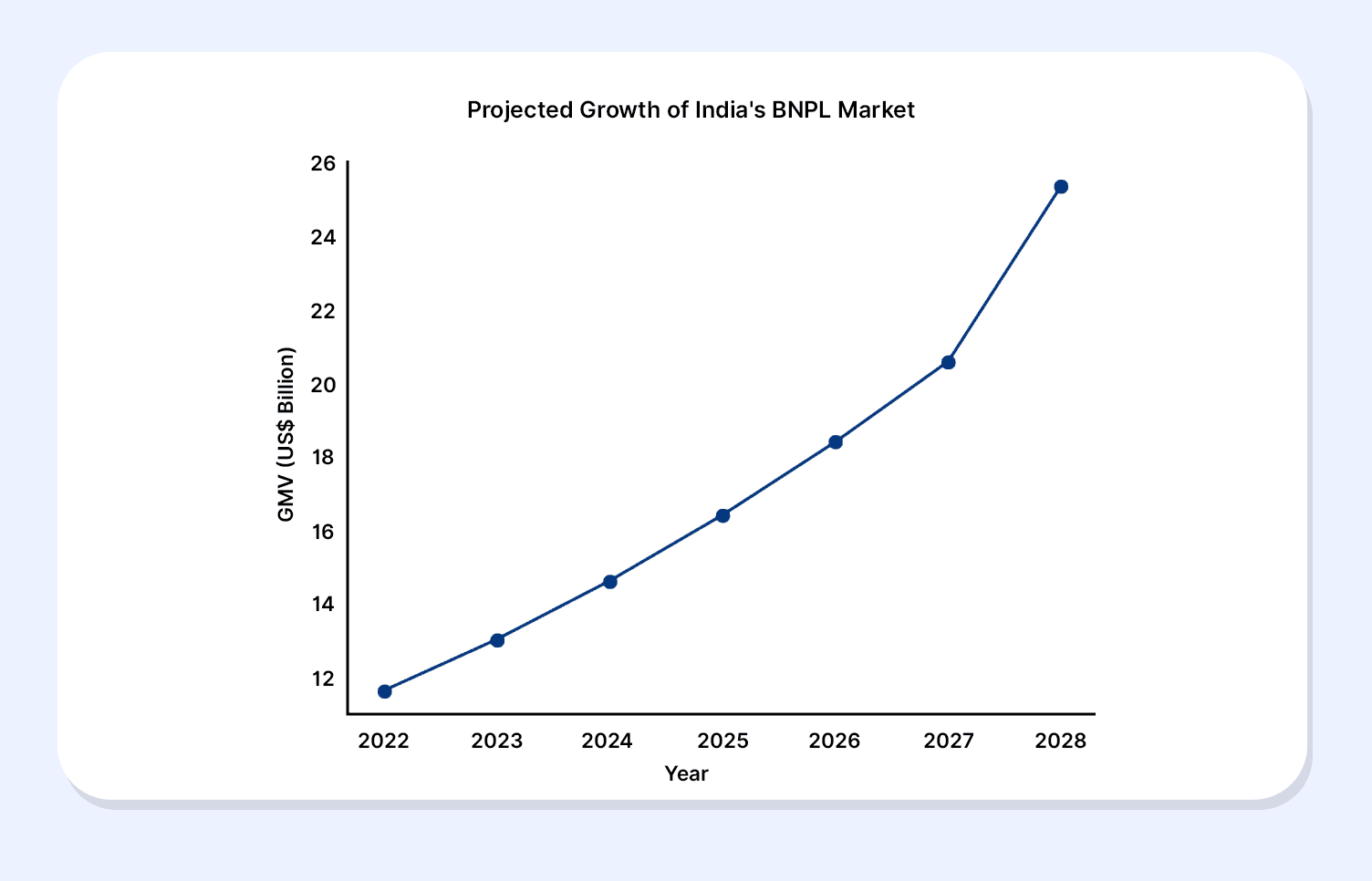

Buy Now Pay Later has gained momentum in the Indian market recently. So much so that India’s BNPL industry is projected to grow at a CAGR of 12% between 2023 and 2028, with its gross merchandise value rising from US$11.6 billion in 2022 to approximately US$25.4 billion by 20281. It is because, with no upfront payment and a relatively easy process, it definitely gives the illusion of being free and painless. However, that is what it is, an illusion.

How Buy Now Pay Later Works

Buy Now Pay Later is the latest pillar of the digital payment world. BNPL meaning is what its name says, a payment option that allows you to purchase without paying up front. It is a short-term loan in which you can defer payment on your current purchase to a later date, allowing you to repay the loan amount in small instalments over a set period.

The buy now pay later EMI repayment cycle usually ranges from a few weeks to a few months. Users can easily access the option through buy now pay later apps India. Some credit cards also now offer BNPL options. Most common BNPL for shopping India includes gadgets and luxury items, which, even though minor, are expensive.

Is It Similar To A Credit Card

From a surface level, BNPL services India 2025, might look like a credit card, but there are several key differences between the two.

Aspect | BNPL (Buy Now, Pay Later) | Credit Card |

Payment structure | Splits the cost of a specific purchase into fixed instalments. | Offers a revolving credit limit usable for multiple purchases. |

Interest | Often the interest is low or there are zero interest payments made on time. | Interest is charged on unpaid balances after the billing cycle. |

Usage | Usually available only with select partner merchants. | Widely accepted across online and offline merchants. |

The Real Cost of BNPL On Personal Finance

While buy now pay later apps India come with many benefits, they are not magic apps that are completely free. The payment option comes with a cost, which, for many, shows up gradually and then drastically all at once.

- The first and foremost downside of not using BNPL wisely is that it can lead to reckless purchases. As it makes purchases feel more affordable than they actually are, BNPL encourages overconsumption.

- With a habit of shopping recklessly, users end up with piling bills that are usually damning. The liability of managing multiple instalment plans at once ends up straining the monthly cash flow.

- As people struggle to pay the accumulated buy now pay later EMI, they inevitably miss or delay payments. These missed or late payments lead to penalties and fees, which add even more financial pressure.

- Even though initially there is no negative BNPL credit score impact, over time, these payment issues affect the user’s credit profile, especially as some BNPL providers report repayment behaviour, causing long-term harm.

What begins as short-term flexibility can quietly turn into long-term financial stress if spending and repayments are not carefully managed.

Smarter Alternatives To BNPL For Managing Expenses

BNPL has proven to be a good option in case of emergencies when a person does not have enough funds to cover an emergency, these no cost EMI apps are not a good choice for daily financial dealings. There are several more sustainable financial habits that can reduce the need for it altogether.

1. Budgeting

Budgeting helps track income and expenses clearly, ensuring spending stays within manageable limits and reducing reliance on deferred payments.

2. Emergency Funds

Building an emergency fund, even gradually, creates a safety net for unexpected costs, allowing emergencies to be handled without borrowing.

3. Low-Risk Investment Planning

Low-risk investment planning can also play a role by helping idle money grow steadily while remaining accessible when needed.

Together, these approaches focus on preparedness rather than postponement, offering greater financial stability and control compared to repeatedly depending on Buy Now, Pay Later solutions.

Does BNPL Always Hurt

The corporate motive for introducing BNPL might be to stimulate overspending, but it would still be an injustice to say the payment option is pure evil. It has, in many instances, helped out people in difficult situations, covering for emergencies. However, the problems arise when people fail to draw a line between emergency and discretionary spending.

One should not be using BNPL as a lifestyle upgrade fund. Moreover, one should also actively consider overseeing and managing their finances, using a healthy mix of best BNPL apps India and options like Grip that help users in developing strong long-term investing discipline and avoid short-term credit habits.

Conclusion

Buy Now, Pay Later has carved out a clear space in India’s digital payments ecosystem by offering short-term flexibility when cash is tight. Used thoughtfully, BNPL can help manage genuine emergencies without disrupting daily life. However, its ease of use and deferred payment structure can also blur spending boundaries, quietly encouraging overconsumption and future financial strain.

The real risk with BNPL lies not in the product itself, but in habitual reliance. Missed EMIs, mounting penalties, and potential credit score damage can turn short-term convenience into long-term stress. That is why BNPL works best as an occasional tool, not a default spending habit.

Building buffers through budgeting, emergency funds, and low-risk investments reduces the need to borrow for routine expenses and brings more control over money decisions. For those looking to shift from short-term credit dependence to long-term financial stability, platforms like Grip Invest help investors channel surplus cash into curated fixed-income and alternative investment options designed for steady, predictable returns.

FAQs

1. Is buy now pay later bad for credit score?

While BNPL in itself is not a bad credit score, missing or delaying buy now pay later EMI does negatively impact the user's credit score over time, especially when the BNPL provider reports repayment behaviour.

2. How is BNPL different from credit cards?

BNPL enables people to pay for a single item in regular payments, usually with little or no interest if they pay on time. It is usually only available at partner merchants. Credit cards let you borrow money for multiple purchases, charge interest on unpaid amounts, and are accepted by more merchants.

3. What happens if BNPL payments are missed?

If users fail to make payment of the buy now pay later EMI, they will be liable to pay late fees and penalties. If there are several missed or late payments, they also risk accumulating them over time, creating a trap that negatively impacts their credit.

Reference:

1. Payments CMI, accessed from: https://paymentscmi.com/insights/bnpl-india-market-research/

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001