Capital Gains Exemption: Sections And Strategies To Reduce Tax

Selling a long-term asset - whether a house, a plot of land, or equity shares - can result in a sizable Long-Term Capital Gain (LTCG). Under the Income Tax Act, 1961, LTCG on immovable property is taxed at 20% with indexation, and LTCG on listed equities beyond INR 1.25 lakh (post-Budget 2024) is taxed at 12.5% without indexation. That can eat deeply into the returns you have worked years to build.

But here is the good news: the Indian tax code is not just about collecting tax - it is also about channelling savings into productive assets. Several provisions under the Income Tax Act offer a capital gains exemption when you reinvest your proceeds in specified assets. Used wisely, these exemptions can legally reduce your tax outgo to zero.

This blog walks you through the key capital gains exemption sections - Section 54, Section 54EC, and Section 54F - explains how real investors use them, and shows you how to build a tax-efficient investment strategy for FY 2025-26.

Before exploring exemptions, it’s important to understand how capital gains tax works in India. Learn in depth about Capital Gains Tax, how to calculate it and more

What Is Capital Gains Exemption?

A capital gains exemption allows a taxpayer to reduce or eliminate the capital gains tax liability that would otherwise arise on the sale of a capital asset, provided certain reinvestment conditions are met. These are not tax deductions under Chapter VI-A; they are stand-alone exemptions built into Sections 54 to 54GB of the Income Tax Act.

The fundamental logic is straightforward: if you have not converted your investment into consumable wealth - and instead have ploughed it back into another productive asset - the government is willing to defer or waive the capital gains tax.

Key distinction: Exemptions under Sections 54, 54EC, and 54F apply only to Long-Term Capital Gains (LTCG). Short-term capital gains are taxed at normal slab rates (or 20% for listed equity under Section 111A) and generally do not qualify for these exemptions.

Let's understand this with the help of an example- Ramesh, a retired teacher in Pune, sells his ancestral house in January 2025 for INR 1.2 crore. He had purchased it in 2002 for INR 15 lakh. After indexation, his LTCG works out to approximately INR 75 lakh. At 20%, his tax liability would be INR 15 lakh. By reinvesting in a new house under Section 54, he can legally claim the entire INR 75 lakh as exempt - bringing his tax to zero.

Sections Offering Capital Gains Exemption

Section 54 - Capital Gains Exemption on Residential Property

Now, the question is, Who it applies to: Individuals and Hindu Undivided Families (HUFs) who sell a residential house property and purchase or construct another residential house in India.

Section 54 is the most widely used capital gains exemption. It has been a cornerstone of Indian property tax planning since the Act was enacted.

Conditions (as amended by Finance Act 2023):

- Long-term: The capital gain must be a

- Type: The property sold must be a

- New property limit: Exemption capped at INR 10 crore of capital gain (from FY 2023-24 onwards).

- One property only: You can claim this exemption for only one new residential property.

- Lock-in: The new house must not be sold within 3 years of purchase/construction.

Some of the Tips: If you are unable to reinvest before the income tax return filing deadline, deposit the unutilised capital gains in a Capital Gains Account Scheme (CGAS) with a scheduled bank before the due date (usually July 31). This preserves your exemption while you search for a suitable property.

Section 54EC - Exemption via Specified Bonds

Who it applies to: Any taxpayer - individual, HUF, company, or firm-selling any long-term capital asset

Section 54EC is arguably the most flexible of the three major exemptions, because it is not restricted to property sellers. If you have sold shares, mutual funds (debt), land, or any long-term capital asset, you can invest in specified bonds and claim exemption.

Key conditions:

- Invest in NHAI (National Highways Authority of India) or REC (Rural Electrification Corporation) bonds within 6 months of the date of transfer.

- Maximum investment: INR 50 lakh in a financial year (and INR 50 lakh in the next FY if the gain arises near year-end).

- Lock-in period: 5 years (extended from 3 years by Finance Act 2018).

- If bonds are transferred or converted into money before 5 years, the exempted gain becomes taxable.

Section 54F - LTCG Exemption for Non-Property Assets

Who it applies to: Individuals and HUFs who sell any long-term capital asset other than a residential house and invest the net sale consideration in a new residential house.

Section 54F is often underutilised, yet it is extremely powerful for investors who have generated large capital gains from stocks, gold, or commercial property.

Key conditions:

- The entire net consideration (not just the gain) must be reinvested to claim full exemption.

- If only part of the consideration is reinvested, the exemption is proportionate: Exempt LTCG = LTCG × (New House Cost / Net Consideration).

- You must not own more than one residential house on the date of transfer.

- The new house must not be sold within 3 years; and you must not purchase another house (other than the new one) within 2 years.

| Important: Section 54F exemption is NOT available if you own more than one residential house (other than the new one) on the date of the transfer. Plan your holdings accordingly. |

Comparison of Capital Gains Exemption Sections

| Feature | Section 54 | Section 54EC | Section 54F |

| Asset Sold | Residential House | Any Long-term Asset | Any Asset (not house) |

| Reinvest In | Residential House | NHAI / REC Bonds | Residential House |

| Max Exemption | Full LTCG (1 house) | INR 50 Lakh | Proportionate |

| Time Limit | 2 yrs buy / 3 yrs construct | 6 months from transfer | 2 yrs buy / 3 yrs construct |

| Lock-in | 3 years | 5 years | 3 years |

| Applicable Tax | LTCG | LTCG (any asset) | LTCG |

Source:ClearTax1

Other Notable Capital Gains Exemption Sections

Section 54B - Agricultural Land: If you sell agricultural land used for farming for the past 2 years, and reinvest in new agricultural land within 2 years, the capital gain is exempt. Applicable to individuals and HUFs only.

Section 54GB - Startup Investment Exemption: Introduced to boost India's startup ecosystem, Section 54GB allows exemption on LTCG from sale of residential property if the proceeds are invested in a notified startup (eligible company under Section 80-IAC) within the prescribed timelines. (Source: CBDT Circular No. 13/2017)

Section 54EE - Compulsory Acquisition: If your land or building is compulsorily acquired by the government and the compensation is received as capital gains, Section 54EE and related provisions offer specific exemptions and deferral options.

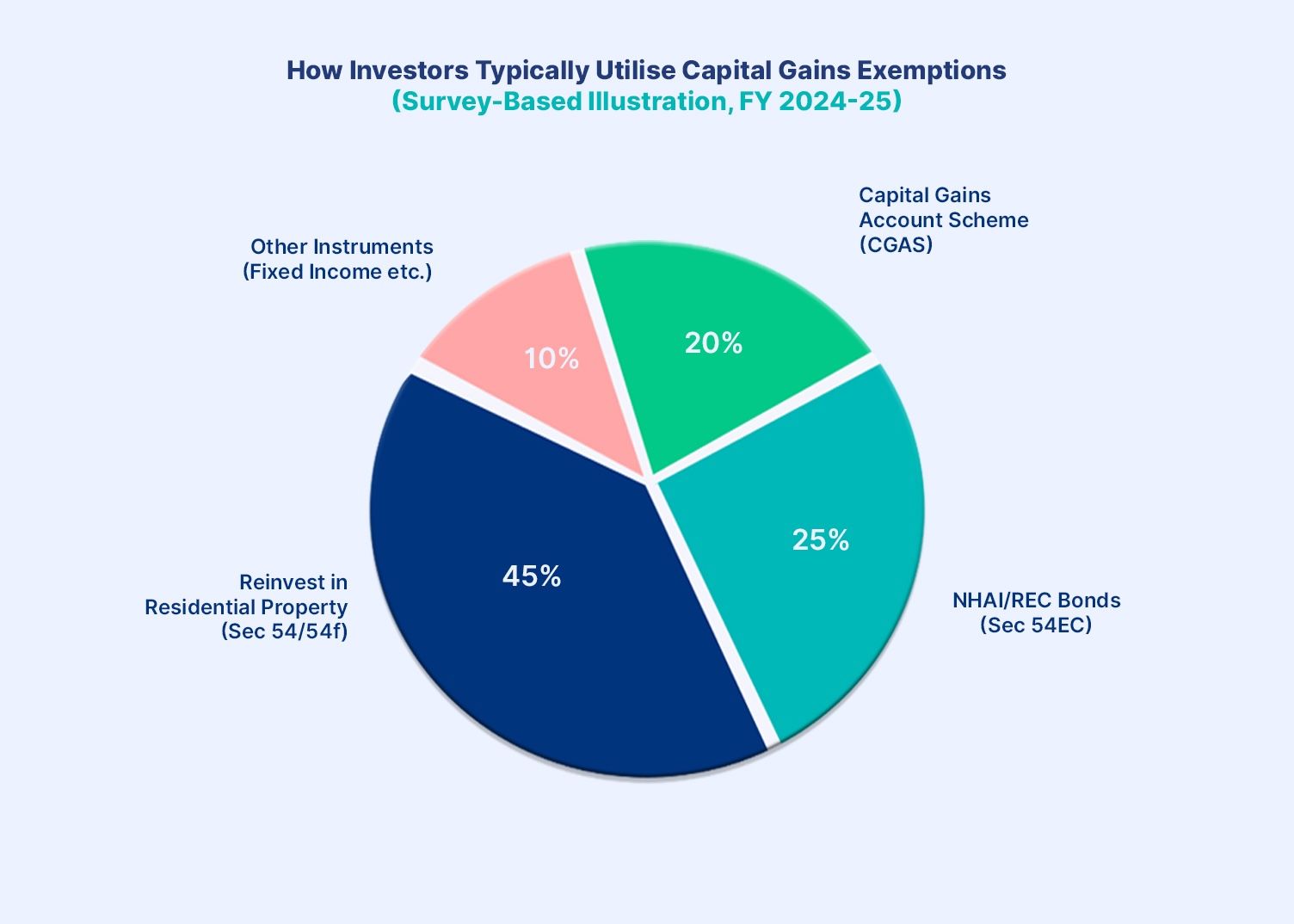

How Investors Use These Exemptions

1. Real Estate Reinvestment - The Most Popular Route

The majority of capital gains tax planning in India revolves around reinvestment in residential property (Sections 54 and 54F). When property prices are rising and you are already planning to upgrade your home, these sections offer a natural and powerful overlap between lifestyle decisions and tax efficiency.

Strategy tip: If you are selling multiple properties or assets in the same financial year, sequence your transactions carefully. You can claim Section 54 for gains from a house sale and Section 54F for gains from shares or gold in the same year - provided you invest in the same new residential house.

2. Specified Bonds - The Flexible, Lock-in Route

Section 54EC bonds are popular among investors who do not wish to buy another property but need a reliable, legally-backed way to park capital gains. They are particularly popular among senior citizens, NRIs liquidating Indian assets, and business owners who have sold commercial real estate.

3. Fixed income investment context: Bonds used for capital gains exemption (NHAI, REC) are low-yield but extremely low-risk instruments. They should be viewed as a tax-planning tool first, income tool second. If you are looking for higher yield within the fixed income space - after complying with capital gains tax obligations - platforms that specialise in curated fixed income products can help you deploy remaining capital more efficiently.

For example, once INR 50 lakh is locked into 54EC bonds and your capital gains tax liability is resolved, the remaining investable surplus can be channelled into higher-yielding instruments depending on your risk profile. (Note: Always consult a registered financial advisor before making investment decisions.)

Chart 2: How Investors Typically Utilise Capital Gains Exemptions

Capital Gains Account Scheme (CGAS) - The Safety Net

Many taxpayers are caught in a bind: they have sold an asset and generated capital gains, but have not yet identified the reinvestment property. The Capital Gains Account Scheme (CGAS), introduced under the Capital Gains Accounts Scheme, 1988, and notified under Section 54(2), 54F(4), etc., allows you to:

- Deposit the unutilised capital gains in a scheduled bank before the return filing due date.

- Use this deposit to complete the reinvestment within the prescribed timeline (2–3 years).

- Earn interest on the deposit while you search for the right property.

Conclusion

Capital gains exemptions are among the most powerful - and most underutilised - provisions in the Indian Income Tax Act. Whether you are a homeowner upgrading your residence, an investor liquidating equity holdings, or a business owner selling commercial property, the law offers a structured, legal path to significantly reduce or eliminate your capital gains tax liability.

The key is timing. Reinvestment deadlines are non-negotiable. Missing the 6-month window for Section 54EC bonds, or failing to deposit into CGAS before your return filing date, can result in the entire gain becoming taxable.

Sections 54, 54EC, and 54F are not loopholes - they are deliberate policy instruments designed to direct private capital into housing, infrastructure, and productive assets. Understanding them is not just tax-smart; it is financially prudent.

Once your capital gains tax obligations are met or minimised, the next priority is making your remaining investable surplus work harder. This is where curated fixed income platforms come in. If you are looking to deploy your post-tax or exempted capital into high-quality fixed income instruments - beyond the low-yield 54EC bonds - Grip Invest offers a curated marketplace of bonds, securitised debt instruments, and other regulated fixed income products. These can help you build a diversified, yield-optimised portfolio while managing risk.

FAQs

1. What are capital gains exemptions in India?

Capital gains exemptions are provisions under the Income Tax Act, 1961 (primarily Sections 54 to 54GB) that allow taxpayers to reduce or eliminate Long-Term Capital Gains (LTCG) tax by reinvesting the sale proceeds or capital gains into specified assets such as residential property or notified bonds within prescribed timelines.

2. Which sections provide exemption from capital gains tax?

The primary sections are: Section 54 (sale of residential house -> new house), Section 54EC (any LTCG -> NHAI/REC bonds), Section 54F (sale of any non-house asset -> new house), Section 54B (agricultural land), and Section 54GB (gains from property -> startup investment).

3. Can capital gains exemption be claimed if the reinvestment is not completed before filing the tax return?

Yes. If you have not completed the reinvestment before the income tax return filing deadline, you can deposit the unutilised capital gains in the Capital Gains Account Scheme (CGAS) with a scheduled bank before the due date of filing the return. This allows you to retain eligibility for exemptions under Sections 54 or 54F while completing the investment within the prescribed timelines.

References:

1. ClearTax, accessed from: https://cleartax.in/s/section-54-capital-gains-exemption

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001