Short Term Capital Gains Tax In India: Rates, Rules, And Examples

Every rupee you earn from selling an investment is not entirely yours to keep - the government takes its share through capital gains tax. For millions of Indian investors active in equity markets, mutual funds, real estate, or gold, understanding how capital gains are taxed is not optional; it is foundational to sound financial planning.

Capital gains tax in India is broadly divided into two categories: Short Term Capital Gains (STCG) and Long Term Capital Gains (LTCG). The classification depends not on the amount of profit, but on how long you held the asset before selling. Sell too soon, and you land in the short-term bracket - typically attracting a higher tax burden.

This guide focuses specifically on Short Term Capital Gains Tax in India - what it is, the applicable rates across different asset classes, how it is calculated, and everything you need to know to stay compliant and plan your investments intelligently.

Important: The Finance Act 2024 (Union Budget 2024) revised the STCG tax rate on listed equity shares and equity-oriented mutual funds from 15% to 20%, effective 23 July 2024 (Section 111A).

What Is Short Term Capital Gains Tax?

Definition

A capital gain arises when you sell a capital asset for more than its purchase price. When this sale happens within a specified holding period - defined differently for each asset class - the profit is classified as a Short Term Capital Gain (STCG). The tax levied on this gain is called Short Term Capital Gains Tax

In simple terms:

Short Term Capital Gain = Net Sale Consideration - Cost of Acquisition - Cost of Improvement - Transfer Expenses

Legal Basis: STCG is governed under Sections 2(42A), 111A, and 115AD of the Income Tax Act, 1961. The Central Board of Direct Taxes (CBDT) issues circulars and notifications to clarify its application from time to time.

Holding Period: The Key Distinguisher

- The holding period varies by asset class. Here is what the Income Tax Act specifies:

- Listed equity shares and equity mutual funds: Held for 24 months or less (revised from 12 months post Budget 2024)

- Immovable property (real estate): Held for 24 months or less

- Debt mutual funds, gold, and other assets: Held for 36 months or less

- Bonds and debentures: Held for 12 months or less

Short Term Capital Gains Tax Rates In India (FY 2025–26)

The tax rate applicable to your short-term capital gain depends entirely on the type of asset. There are two broad tax treatment categories:

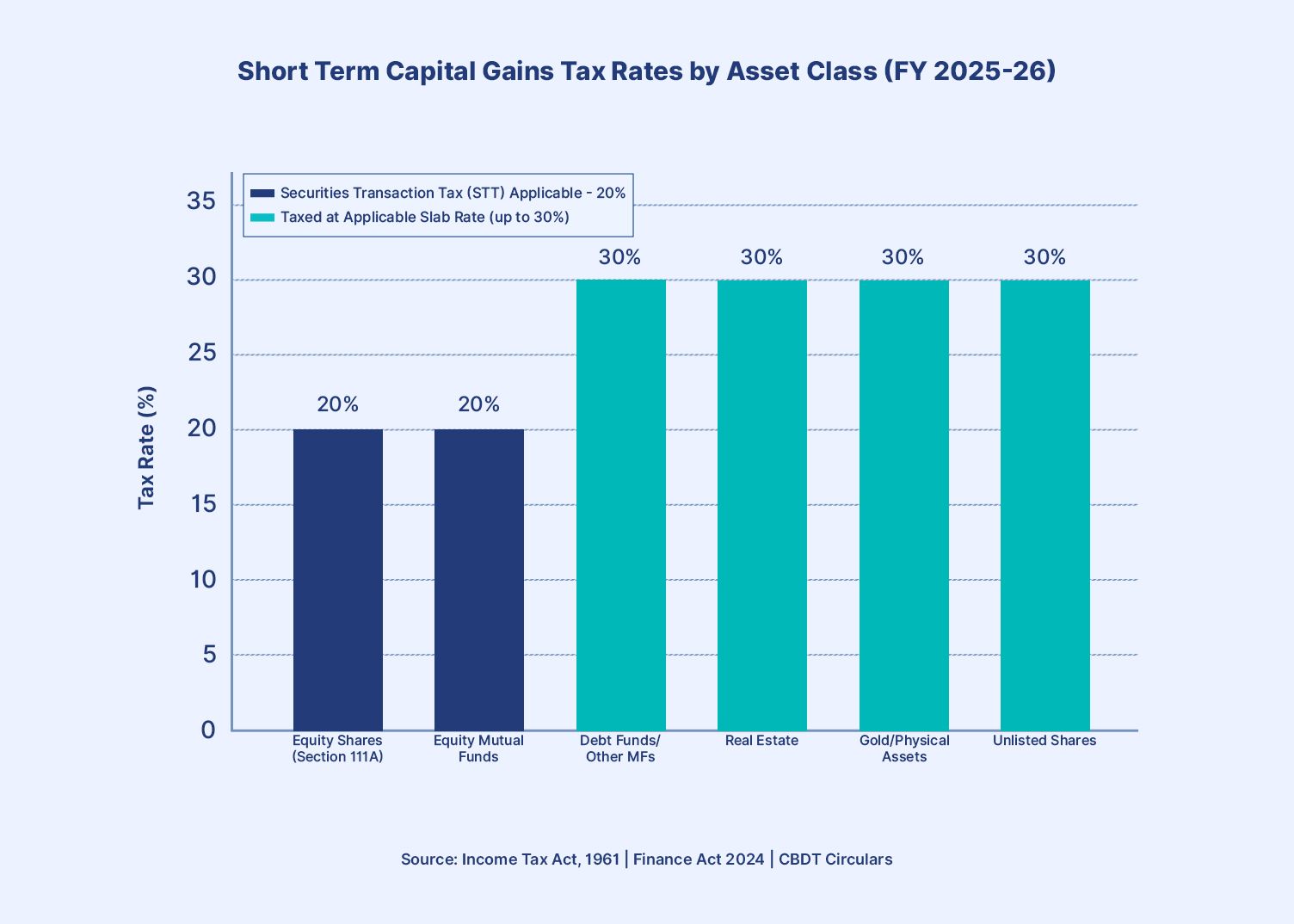

- Flat rate of 20% under Section 111A - applicable to listed equity and equity mutual funds where STT has been paid

- Slab rate taxation - applicable to all other assets such as real estate, gold, debt funds, and unlisted shares

STCG Tax Rates - Comprehensive Table

Table 1: STCG Tax Rates Across Asset Classes in India (FY 2025–26)

| Asset Class | Holding Period (Short Term) | Applicable Section | STCG Tax Rate | Remarks |

| Equity Shares (Listed) | Up to 24 months | Section 111A | 20% | STT applicable |

| Equity Mutual Funds | Up to 24 months | Section 111A | 20% | STT applicable |

| Debt Mutual Funds | Up to 36 months | Normal slab | Slab Rate | Up to 30% |

| Real Estate / Property | Up to 24 months | Normal slab | Slab Rate | Up to 30% |

| Gold / Physical Assets | Up to 36 months | Normal slab | Slab Rate | Up to 30% |

| Unlisted Shares | Up to 24 months | Normal slab | Slab Rate | Up to 30% |

| Bonds / Debentures | Up to 12 months | Normal slab | Slab Rate | Up to 30% |

Source: Bajajfinserv1

Section 111A - The Equity STCG Framework

Section 111A is the cornerstone of equity taxation in India. It applies when:

- The asset is a listed equity share, a unit of an equity-oriented mutual fund, or a unit of a business trust

- The Securities Transaction Tax (STT) has been paid at the time of sale

- The holding period does not exceed 24 months

Under these conditions, the entire short-term capital gain is taxed at a flat 20% - irrespective of your income tax slab. This is notably significant for taxpayers in the 5% or nil tax bracket, as even they must pay 20% STCG on equity profits.

STCG Tax Rate Visualised

Chart 1: Short Term Capital Gains Tax Rates by Asset Class (FY 2025–26)

How Short Term Capital Gains Tax Is Calculated

The Step-by-Step Formula

Calculating STCG involves three steps:

1. Calculate Net Sale Consideration: Sale Price minus Brokerage / Transfer Expenses

2. Subtract Cost of Acquisition (and cost of improvement, if any)

3. Apply the applicable tax rate to the resulting Short Term Capital Gain

Hypothetical Example 1: STCG on Listed Equity Shares

Scenario: Rajesh buys 500 shares of a listed company at INR 400 each on 1 January 2025. He sells all of them at INR 560 each on 15 October 2025. He pays INR 2,000 in brokerage. STT has been paid. Holding period: approximately 9 months - qualifies as short term.

Table 2: STCG Calculation - Listed Equity Shares

| Component | Amount ( INR ) | Note |

| Purchase Price (Cost of Acquisition) | INR 2,00,000 | |

| Sale Price | INR 2,80,000 | |

| Brokerage / Transfer Charges | INR 2,000 | Deductible expense |

| Net Sale Consideration | INR 2,78,000 | (INR 2,80,000 - INR 2,000) |

| Short Term Capital Gain | INR 78,000 | (INR 2,78,000 - INR 2,00,000) |

| STCG Tax @ 20% (Section 111A) | INR 15,600 | Surcharge + cess extra |

Additional 4% Health & Education Cess applies on the tax amount. Total effective outgo = INR 15,600 + INR 624 (cess) = INR 16,224.

Hypothetical Example 2: STCG on Real Estate

Scenario: Priya purchases a residential flat in Pune for INR 45,00,000 in March 2024 and sells it for INR 58,00,000 in November 2025 - holding it for approximately 20 months, which qualifies as short term for real estate (held under 24 months). Her registration and transfer charges at sale were INR 50,000.

- Net Sale Consideration: INR 58,00,000 - INR 50,000 = INR 57,50,000

- STCG = INR 57,50,000 - INR 45,00,000 = INR 12,50,000

- Tax Rate: Applicable income tax slab (assume she is in the 30% bracket)

- STCG Tax Payable: INR 12,50,000 × 30% = INR 3,75,000 + cess @ 4% = INR 3,90,000 (approx)

Assets Subject To Short Term Capital Gains Tax

1. Equity Shares

Equity shares listed on a recognised stock exchange in India are subject to Section 111A if sold within 24 months of purchase and STT has been paid. The flat 20% rate means no slab rate benefit - even a taxpayer in the 0% bracket pays this rate. Unlisted equity shares do not enjoy Section 111A protection. STCG on unlisted shares is added to your total income and taxed at your applicable slab rate.

2. Real Estate / Property

Immovable property sold within 24 months of acquisition attracts STCG at the taxpayer's slab rate. There is no indexation, no INR 1 lakh exemption (as available for LTCG on equity), and no flat rate benefit. The full gain is added to income.

However, Section 50C provides that if the sale consideration is less than the stamp duty value (circle rate), the stamp duty value is treated as the full sale consideration for STCG calculation - preventing under-reporting.

3. Debt Investments - Mutual Funds, Bonds, and Fixed Income

Debt mutual funds, bonds, debentures, and similar fixed income instruments have their own holding period thresholds for short-term classification - typically 12 to 36 months depending on the instrument type.

Fixed Income STCG - Key Distinction

From 1 April 2023, debt mutual funds where equity exposure is 35% or less are taxed at the investor's slab rate regardless of holding period - there is no separate LTCG rate for these funds. Short-term gains on bonds and NCDs (held under 12 months) are also fully taxable at slab rates. This makes debt funds less tax-efficient than equity funds for short holding periods.

4. Gold and Physical Assets

Physical gold, silver, and other physical assets held for fewer than 36 months attract STCG at the applicable income tax slab rate. Sovereign Gold Bonds (SGBs) have special treatment - redemption on maturity is exempt from capital gains tax.

STCG Vs. LTCG- A Quick Comparison

Understanding where STCG ends and LTCG begins helps you make holding-period decisions that directly affect your post-tax returns.

| Parameter | STCG | LTCG |

| Equity Tax Rate | 20% (Sec. 111A) | 12.5% (Sec. 112A, above INR 1.25L) |

| Real Estate Tax Rate | Slab rate (up to 30%) | 12.5% without indexation |

| Indexation Benefit | Not available | Available for select assets |

| Basic Exemption | None | INR 1.25L on equity LTCG |

| Debt Funds | Slab rate | Slab rate (post Apr 2023) |

| Filing ITR Schedule | Schedule CG | Schedule CG |

Source: Bajajfinserv1

Conclusion

Short-term capital gains tax plays a significant role in determining the actual returns investors take home after selling an asset. Because the holding period directly affects whether gains are taxed at 20% under Section 111A or at slab rates, understanding these rules can help investors make smarter decisions about when to sell and how to structure their portfolio.

For many investors, short holding periods are common in equity trading, debt instruments, or opportunistic real estate transactions. However, the tax impact can meaningfully reduce profits if it is not factored into the investment strategy. Careful planning around holding periods, asset allocation, and transaction costs can help minimise the tax burden while improving overall portfolio efficiency.

Platforms like Grip Invest aim to make fixed-income investing simpler by providing access to curated investment opportunities such as corporate bonds, structured debt, and other income-generating assets. By combining clear investment insights with diversified fixed-income options, investors can build portfolios that focus not only on returns but also on tax awareness and long-term financial stability.

Ultimately, understanding short-term capital gains tax rules is not just about compliance with tax laws. It is about making more informed investment decisions, managing risk, and ensuring that the returns you earn translate into sustainable wealth creation over time.

FAQs On Short-Term Capital Gains Tax

Reference:

1. Bajajfinserv, accessed from: https://www.bajajfinserv.in/investments/understanding-short-term-capital-gains-tax

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001