Convexity Adjustment: Meaning And Importance In Bond Pricing

Interest rates in India set the tone for debt valuations. The Union government plans to borrow INR 17.2 trillion in 2026–27, so even small rate moves can ripple prices across the curve1.

Corporate bonds add another layer of sensitivity. Outstanding bonds have risen from INR 17.5 trillion in FY2014-15 to ~INR 53.6 trillion in FY2024-25, taking the market to roughly 15-16% of GDP1.

When market rates change, bond prices do not move linearly. Duration gives a useful first estimate, but it can miss the curve that shows up when moves get bigger. That curve is a convexity adjustment, and this blog breaks down what it is, why it matters, and how to use it in real-world bond decisions.

What Is Convexity In Bonds?

Bond prices and interest rates move in opposite directions.

- If rates go up, bond prices go down.

- If rates go down, bond prices go up.

Duration gives you a good first estimate of price change, but it assumes the price-yield relationship is a straight line. In real life, it’s curved, and bond convexity measures that curve.

Because of this curve, a bond’s price typically:

- Rises a bit more when yields fall, and

- Falls a bit less when yields rise.

The curve gives you a small “cushion” on the downside and a small boost on the upside for the same size yield move.

Understanding Convexity Adjustment

When interest rates move, bond prices move the other way. Here is duration vs convexity at a glance3:

Aspect | Modified duration | Convexity |

What it measures | Straight-line (first-order) price sensitivity to yield | Curve (second-order) in the price-yield relationship |

Best used for | Small yield moves | Improves estimates when yield moves are larger |

What it does to your estimate | Gives the main price change | Adds a correction term that duration misses |

How to read it | Higher value means the price reacts more to yield changes | Higher positive value usually means a better cushion in rate swings |

Typical sign | Positive | Positive for many non-callable bonds, can be negative for callable bonds |

What investors use it for | Quick sensitivity check, comparing bonds | Stress checks, comparing bonds with similar duration, spotting option risk |

Common limitation | Can overstate losses and understate gains when moves are bigger | Still an approximation, changes as yield and time change |

Therefore

- Duration tells you the main effect on price.

- Convexity tells you the extra curve effect that duration misses.

That extra part is called the Convexity adjustment.

What duration tells

Modified duration is a quick measure of bond price sensitivity in India.

It estimates how much a bond price may change for a small change in yield.

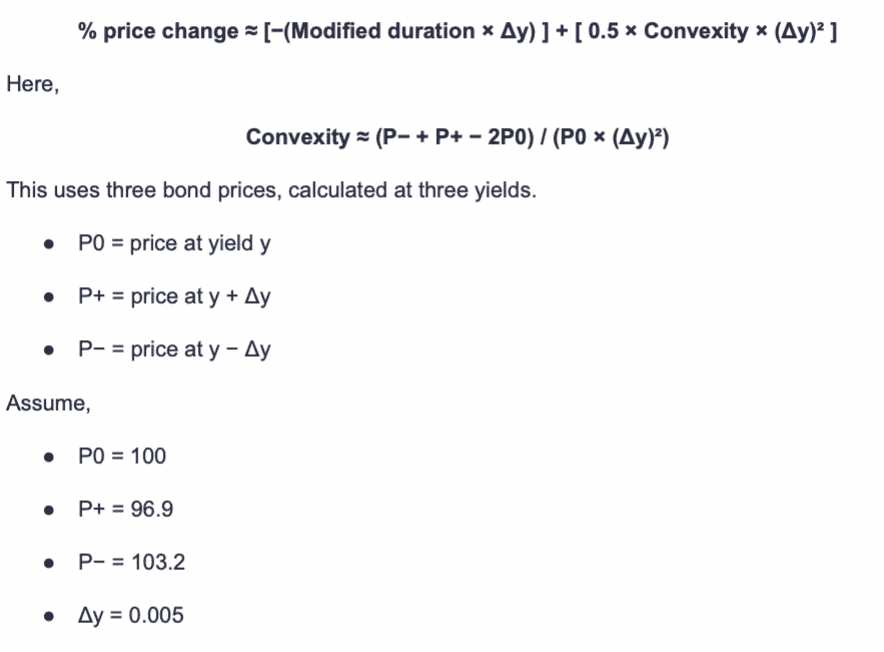

Use this formula:

However, duration is not enough. As noted earlier, it treats the price move like a straight line. Real bond pricing behaves like a curve, especially when yields move more. So duration can slightly overstate losses when yields rise, and it can also slightly understate gains when yields fall.

What convexity adds

Convexity measures the curve in the price-yield relationship. It refines the duration estimate by adding a correction term. This correction is the Convexity adjustment.

Bond convexity formula:

Convexity = (103.2 + 96.9 - 200) / (100 × 0.000025)

= (0.1) / (0.0025)

= 40

So the bond’s convexity is about 40.

Estimate price change for a 50 bps rise in yield:

Duration part = -(6 × 0.005) = -0.03 = -3.00%

Convexity adjustment = 0.5 × 40 × (0.005)²

= 20 × 0.000025

= 0.0005 = +0.05%

Net change = -3.00% + 0.05% = -2.95%

Estimated price = INR 100 × (1 - 0.0295) = INR 97.05

Estimate price change for a 50 bps fall in yield:

Duration part becomes +3.00%

Convexity adjustment stays +0.05%

Net change = +3.05%

Estimated price = INR 103.05

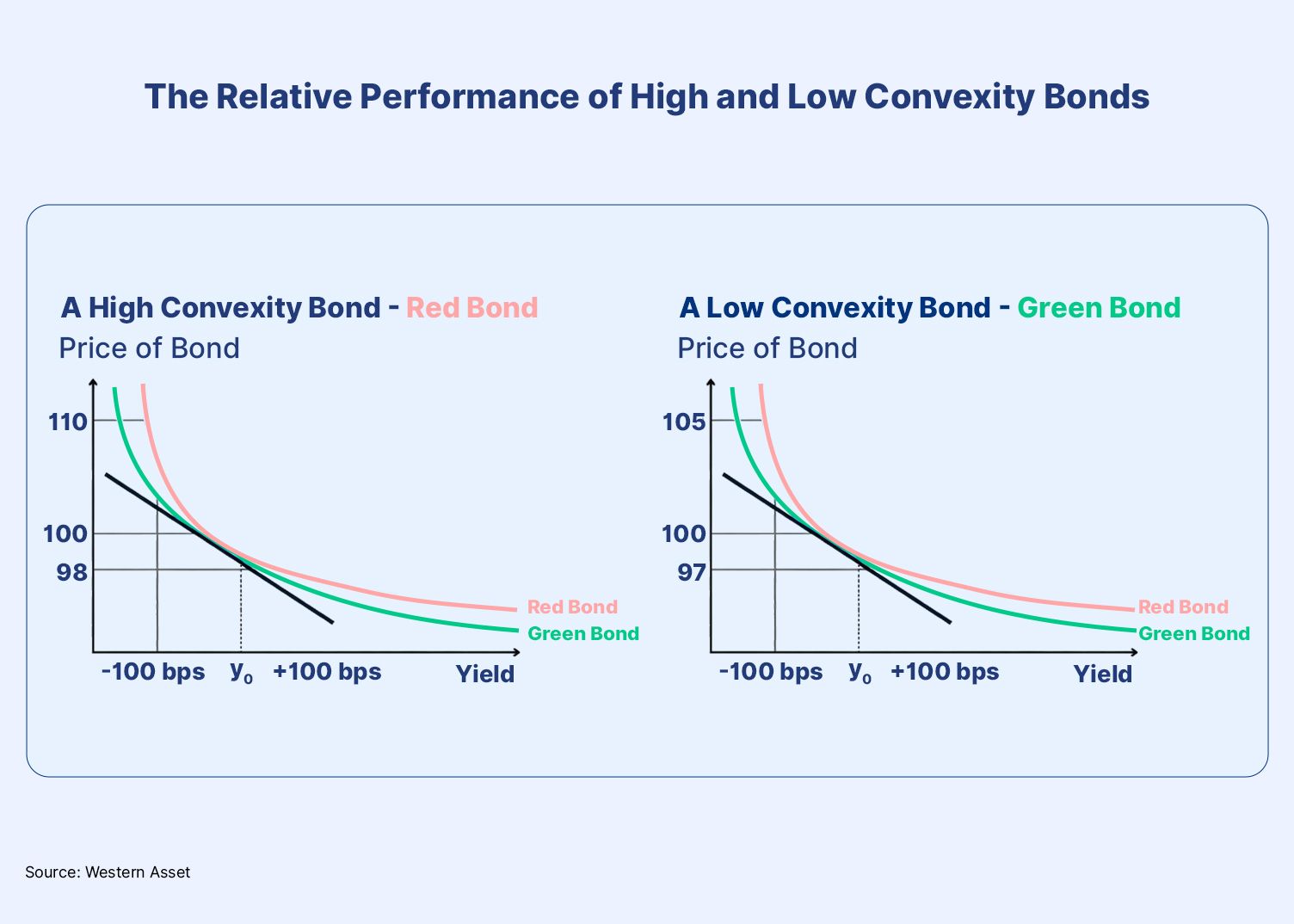

Why Convexity Matters For Bond Investors

Convexity is about how curved a bond’s price–yield relationship is. Because the relationship is curved, bond prices don’t move up and down in a perfectly even way as yields change. That curve is the reason convexity matters.

- Better estimates than duration alone

Convexity improves the duration estimate by adding a second term, so you capture some of the curvature that duration ignores.

- A useful “tilt” for plain bonds

For many non-callable, fixed-rate bonds, convexity is positive. That usually means losses from a yield rise are slightly smaller than what the straight-line estimate suggests, and gains from a yield fall are slightly larger.

- Critical for bonds with embedded options

Callable bonds and some mortgage-style structures can show negative convexity. Price upside can be capped when yields fall, while downside can worsen when yields rise. Duration can look fine on paper, but convexity reveals the catch.

- Helps compare bonds with similar duration

Two bonds can have the same duration but different convexity. In practice, the one with higher convexity can behave better when rates swing, all else equal.

Role In Interest Rate Risk Management

Interest rate risk is the risk that bond prices change when yields move. It is usually managed by measuring sensitivity and then reducing it, spreading it, or hedging it.

Convexity plays a practical role in interest rate risk management because it tells you how a bond, behaves when yields move by more than a tiny amount.

1) Better estimates for P&L when rates move

Investors often use duration to estimate how much the price might change. Convexity improves that estimate, especially for bigger shifts (say 50–100 bps+) and in volatile rate markets. Without it, you can systematically under- or over-estimate risk.

2) Stress testing and scenario analysis

When you run scenarios like “yields up 1%” or “down 1%”, convexity helps capture how losses and gains won’t be symmetric. Portfolios with higher positive convexity typically lose less in rising-rate shocks and gain more in falling-rate shocks, compared with the same duration.

3) Hedging

If you hedge with instruments that mainly target duration (like interest rate futures or plain swaps), you’re mostly hedging the first-order risk. Convexity explains why a duration-matched hedge can still drift when rates move. Adding convexity-aware hedges can reduce that mismatch.

4) Managing negative convexity exposures

Some assets have negative convexity, such as callable bonds and many mortgage-like instruments. These can behave differently, like limited upside when yields fall, but full downside when yields rise. Risk management here is often about:

- Sizing the exposure,

- Setting tighter limits,

- And using hedges that perform better when yields fall

Limitations And Misinterpretations

Duration and convexity are useful, but they are still approximations. They describe how a bond may react to yield changes, not everything that can move its price.

Key limitations to keep in mind:

- Best for small yield moves: Modified duration is a linear estimate, and convexity is a second-order fix. If yields move a lot, the relationship can change further, so the estimate can drift.

- Assumes a simple yield shift: Many duration measures work cleanly when the yield curve shifts in a broadly parallel way. Real curves often twist, steepen, or flatten. Key rate duration is designed for this type of non-parallel risk.

- Not all price moves are “rates”: Credit spreads, liquidity, and changes in perceived default risk can move bond prices even if the risk-free curve is steady. Duration and convexity do not isolate those drivers.

- Convexity is not a single permanent number: Convexity changes with yield levels, time to maturity, and bond features. Treating it as fixed in every scenario can cause false precision.

Common misinterpretations:

- “Higher convexity is always better”- Positive convexity is often helpful in rate swings, but it can come with trade-offs such as lower yield or different risk exposures. Convexity is one input, not a stamp of quality.

- Mixing units and conventions - Errors often come from using basis points and decimals inconsistently, or using a convexity definition that is not paired correctly with the price change formula. A quick unit check usually prevents this.

Conclusion

Convexity adjustment may sound technical, but here’s what it really means for investors: bond prices don’t move in a straight line when interest rates change. Duration gives you the first estimate, but convexity refines it, especially when rate moves are meaningful. That extra correction can make a difference in how you assess downside risk, upside potential, and portfolio stability.

In a market like India, where government borrowing is large and corporate bond markets are deepening, even small shifts in yields can move valuations. Investors who understand duration and convexity are better equipped to evaluate interest rate risk, compare bonds more intelligently, and avoid surprises during volatile rate cycles.

For investors exploring fixed-income opportunities through platforms like Grip Invest, understanding convexity can help in comparing different bond structures, especially when looking at longer-tenure instruments or those with embedded features. It adds another layer of clarity beyond headline yields and duration numbers.

In short, convexity adjustment is not just a formula. It is a practical tool that sharpens your bond pricing estimates and strengthens your interest rate risk management approach.

FAQs

1. What is convexity in bonds?

It describes how a bond’s price sensitivity can change as yields shift. Used with duration, it helps capture the curved price-yield relationship.

2. Why is convexity important?

It improves rate risk estimates when yields move by more than a tiny amount. It also highlights whether gains and losses may be uneven, which is useful when comparing bonds with similar duration.

3. Does higher convexity always mean lower risk?

Not necessarily. While higher positive convexity can cushion price swings when rates move, it may come with trade-offs like lower yield or longer maturity. Always assess it alongside duration, credit risk, and overall portfolio goals.

References:

1. PIB, accessed from: https://www.pib.gov.in/PressReleasePage.aspx?PRID=2221455&lang=1®=3

2. NITI, accessed from: https://niti.gov.in/sites/default/files/2025-12/Deepening_the_Corporate_Bond_Market_in_India.pdf

3. Investopedia, accessed from: https://www.investopedia.com/terms/c/convexity-adjustment.asp

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001