CRIF Score vs CIBIL Score: Key Differences Explained (India Guide)

If you have recently applied for a loan or a new credit card, your credit score was most likely accessed by the relevant financial institution. Most institutions consider either the CIBIL or CRIF score as the benchmark for evaluating an individual's creditworthiness. However, you might wonder what the difference between these two scores is, which agency calculates them and what the most critical differences are.

What Is A CIBIL Score And Who Calculates It?

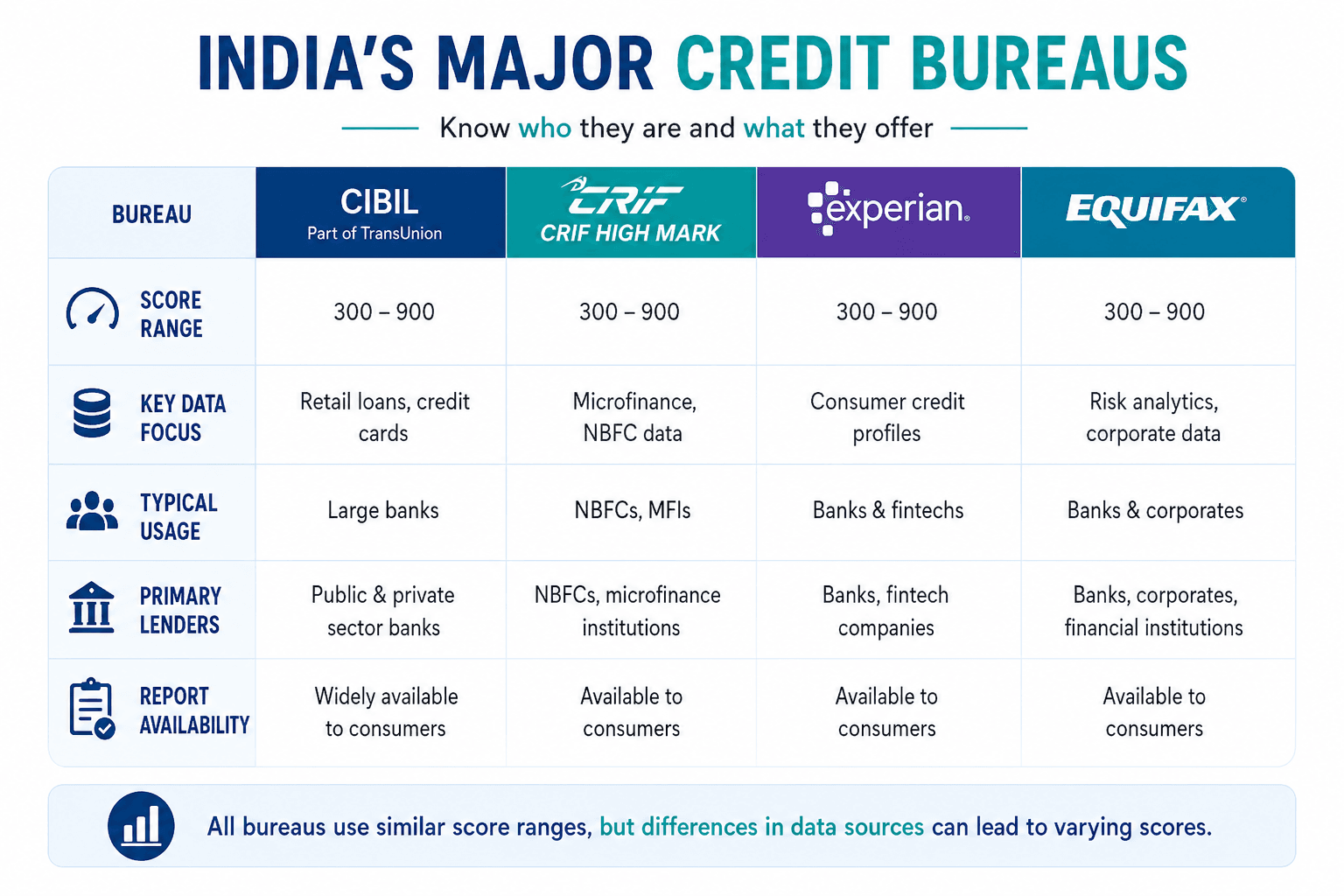

CIBIL is one of the most widely used credit scores in India by a wide range of financial institutions and banks. It is issued by TransUnion CIBIL, and the score ranges from 300 to 900, with a higher range indicating better financial health.

If you have a CIBIL score of more than 750, it is categorised as ‘strong’ and your chances of obtaining a loan or credit card at a favourable term increase. The score is based on your credit history, repayment details, credit utilisation and existing loan obligations. Each factor has several benchmarks based on which a comprehensive score is calculated.

What Is A CRIF Score And Who Calculates It?

Even though CIBIL is quite popular among lenders and financial institutions, there are other credit scoring mechanisms, including CRIF High Mark. It has its own credit-scoring system based on data submitted by lenders, including banks, NBFCs, and microfinance institutions.

The CRIF High Mark score reflects the credit behaviour in a similar manner to CIBIL, but there might be some variations due to different data sources and reporting frequencies. It is most generally used by NBFCs and institutions in the microfinance segment.

While it may not have the same brand recall as CIBIL, the CRIF High Mark score plays a crucial role in lending decisions, especially for borrowers in semi-urban and rural segments.

Are The Scoring Ranges The Same?

One common question concerns the scoring ranges of the two systems. CRIF and CIBIL both have a similar range of 300-900, but identical ranges do not mean that the eventual score will also be the same.

Each bureau receives input from different lenders, and records are updated at different intervals. Hence, if you are looking for a comprehensive creditworthiness report, it is always better to consider more than one bureau score.

Key Differences: CIBIL vs CRIF (Head to Head)

Here are the most critical differences between the two scores:

Basis | CIBIL Score | CRIF Score |

Credit Bureau | TransUnion CIBIL | CRIF High Mark |

Score Range | 300–900 | Same |

Primary Data Sources | Banks, financial institutions and credit cards | NBFCs, microfinance institutions |

Lender Preference | Used by banks and financial institutions for new loan queries and evaluating creditworthiness | It is commonly used by new lenders and NBFCs |

Microfinance Coverage | There is only limited information available related to microfinance data | There is a strong presence in microfinance |

Report Depth | It provides a detailed customer report with wide accessibility | It is mostly preferred by lenders and is less customer-friendly (the report) |

Market Recognition | It is one of the most recognised credit scores in India | The lender usage is high, but the popularity among the general public is limited |

Score Variability | May differ due to specific lender reporting | Difference due to a broader data inclusion |

Comparison of India’s Major Credit Bureaus

How To Check Your CRIF Score For Free?

You can check the CRIF score through the official platform or via authorised partners. Here is the process:

- Visit the CRIF High Mark website or a partnered financial platform

- Register using your mobile number and basic details

- Complete identity verification (OTP-based)

- Access your credit report and score

As per regulatory guidelines, you are entitled to receive one free credit report from each bureau. It is always good to check your credit report periodically to ensure you catch any errors or incorrect information and report them to the relevant bureau.

How To Improve Either Score?

If your credit score is low, you might not be offered loans and credit cards at favourable terms. It is important to develop financial discipline over a long period and build your credit score. Please ensure you do not miss EMI or credit card bill payments, as financial institutions report such incidents directly to the bureaus.

In addition, if you are given a total credit of INR 10 lakh, you should try to utilize around 30%. Please avoid making constant inquiries and maintain a balanced mix of secured and unsecured credit.

Conclusion

CIBIL is one of the most widely used credit scores in India by a wide range of banks and financial institutions. However, there are numerous other bodies that utilise credit scores issued by other bureaus. One such popular choice is the CRIF score. The score range is identical for both bureaus.

However, the data sources and lender preferences are distinct. If you have a low credit score, your loan applications might be rejected, or you might be offered a loan at unfavourable terms. To improve your score, it is critical to maintain financial discipline over the years.

Platforms like Grip Invest help investors explore curated options across fixed income, bonds, and alternative assets based on their risk appetite.

FAQs On CRIF vs CIBIL Score

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001