Demand Deposit Vs Fixed Deposit: Key Differences, Returns, And When To Use Each

When Most Indian investors invest their money in long-term deposits with safe and high-yield accounts. Bank deposits are the preferred method of saving for many individuals in India because they are secure, predictable, and simple to access. However, not all bank deposits function similarly. Understanding the demand deposit vs fixed deposit will enable you to identify which type of deposit best meets your requirements, whether those are daily liquidity, preparedness for emergencies, or long-term wealth preservation.

The right type of deposit allows your money to work productively rather than remaining idle or being unavailable when you require it most. When you understand the difference between demand deposit and fixed deposit, it can boost your confidence and secure every bit of your hard-earned money.

What’s A Demand Deposit?

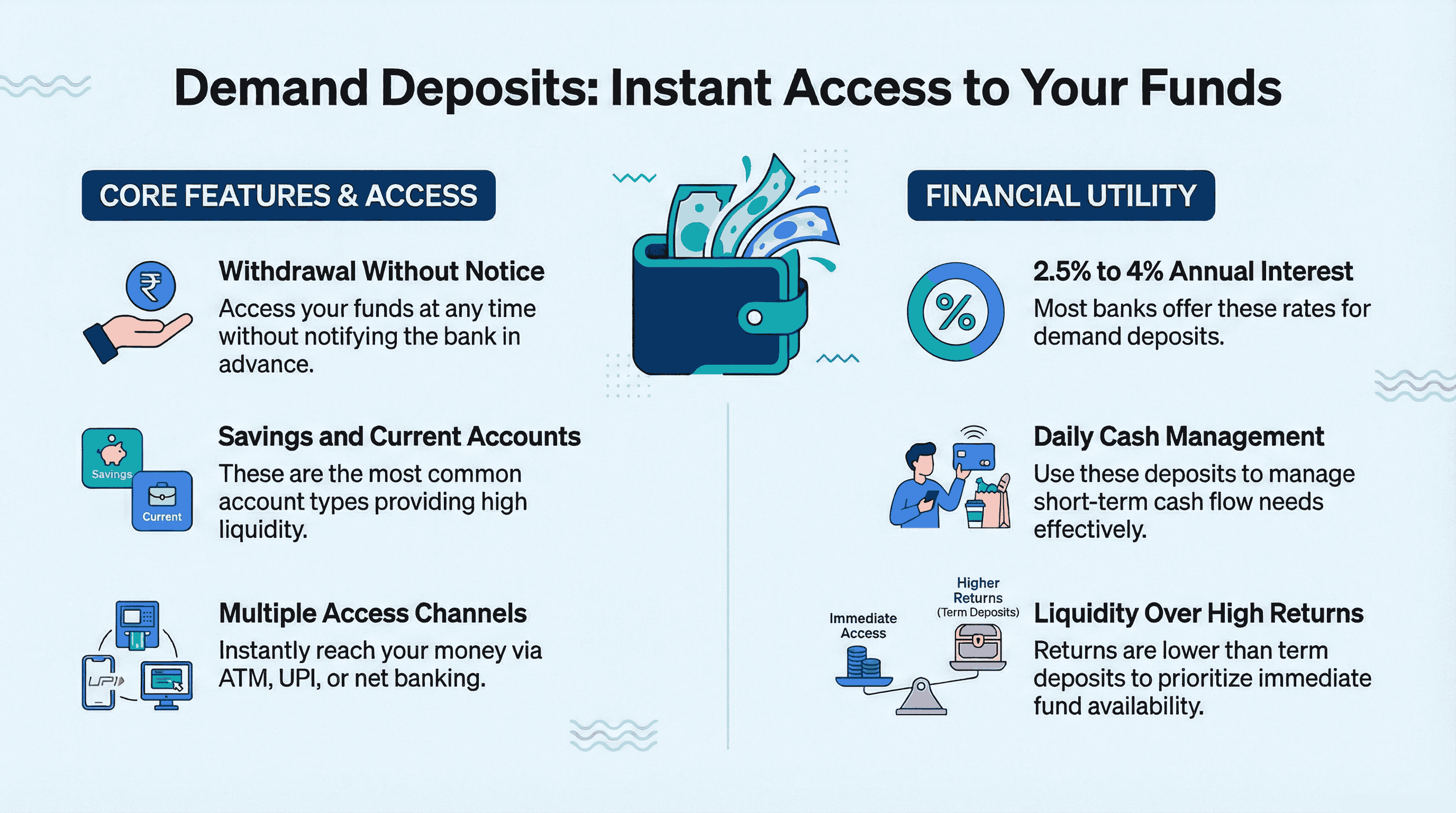

A demand deposit is one of the types of bank deposits India that allows you to withdraw funds at any time without notifying your bank in advance. The most common examples of demand deposits are savings accounts and current accounts. Liquidity is the key attribute of a demand deposit. Your funds are available for you on demand.

You can easily access your money through an ATM, UPI, or net banking. This requires no pre-notice to the bank and involves no other facilities.

You receive interest on your demand deposits; the interest on demand deposits is relatively low compared to term deposits, with most banks offering interest rates of between 2.5% and 4% p.a. The actual amount will vary depending on the bank. Although you will earn a relatively low return with demand deposits, they are important for managing daily cash flow and short-term cash flow needs.

What Is A Fixed Deposit?

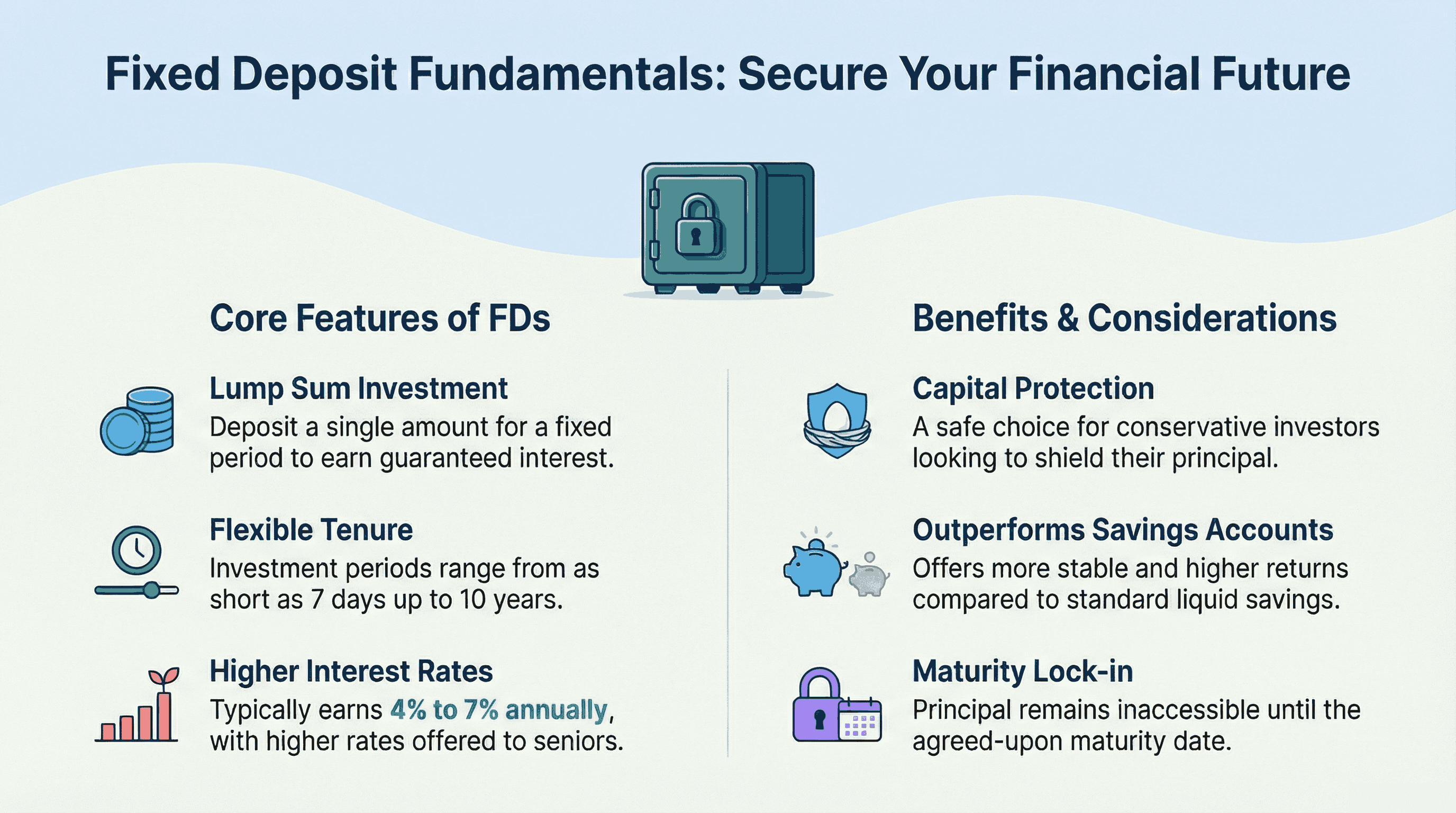

A fixed deposit, or FD, is a type of time deposit where you place a lump sum of money with a bank for a specified period at an agreed-upon interest rate. With bank deposit comparison India, fixed deposits have a deposit period that varies from 7 days to 10 years in India. The interest earned on fixed deposits is typically greater than the interest earned on savings accounts. The interest rates are usually between 4% and 7% per year for ordinary citizens and slightly higher for seniors.

Fixed deposits are popular choices for conservative investors. Fixed deposits provide stable returns, protect your capital, and offer you steady income if you look at FD vs savings account interest rates. However, fixed deposits do not allow you to access your principal until it matures.

Demand Deposit Vs Fixed Deposit: Key Differences

It's crucial to understand the difference between demand deposits and fixed deposits when managing finances. The best choice depends on your liquidity needs, time frame, and financial goals. Let's understand them based on the following elements:

1. Liquidity

The primary distinction is liquidity; demand deposits provide for immediate access to your money, while fixed deposits restrict access to your deposits until the maturity period. If you were to withdraw your funds before the maturity date of a fixed deposit, you would incur an early withdrawal fee.

One major difference between demand deposit and fixed deposit is interest rates. Usually, demand deposits have lower interest rates because banks must keep a large amount of liquidity available. In contrast, banks are able to pay higher interest rates on fixed deposits because they have access to those funds for an extended period.

In liquid deposits vs time deposits, there is no lock-in period on demand deposits. There is a required lock-in period for fixed deposits, so fixed deposits are often a better option for planned savings than for unplanned expenses.

4. Risk And Returns

Fixed deposits, promoted by the Reserve Bank of India and insured by DICGC, are low risk. They offer stable, predictable returns, unlike demand deposits, which are more flexible but less predictable.

Comparison Table: Demand Deposit vs Fixed Deposit

| Feature | Demand Deposit | Fixed Deposit |

| Liquidity | High, instant withdrawal | Low to moderate, subject to tenure |

| Interest Rates | 2.5%–4% | 2.75%-6.50% |

| Lock-in Period | None | Fixed tenure |

| Risk Level | Very low | Very low |

| Ideal Use | Daily expenses, emergencies | Long-term savings, income planning |

When Should You Choose A Demand Deposit?

Demand deposit can mean keeping a fund for your emergency and providing quick access to short-term cash when you need some liquidity. Generally, it is worth keeping at least three to six months' worth of expenses in liquid accounts such as savings. For instance, if your monthly expenses are INR 40,000. Then, you should aim to keep INR 150,000 to INR 250,000 in liquid demand deposits so that you have quick access should unexpected events occur.

Demand deposits are ideal for payroll, bill payments, and daily transactions where immediate access to funds is prioritised over earning higher interest. They offer greater flexibility compared to savings and fixed deposits.

When Should You Choose A Fixed Deposit?

Fixed deposit accounts are ideal for long-term savings and income planning, such as saving for a child's college or a house down payment. FDs secure your capital and provide a safe, readily accessible, uniform income.

In addition to providing a steady income to retirees and conservative investors, fixed deposits may also provide a way to create regular monthly or quarterly payments of interest income. Generally, in bank deposit comparison India, fixed deposits exhibit greater stability compared to other financial market-linked products. The result provides a level of security during times of uncertainty in the economy.

Beyond Traditional Deposits: Other Fixed-Income Alternatives

Although bank deposits are still in style, some investors are beginning to consider alternatives to traditional bank deposits to maximise the interest earned. Bonds, government bonds, and structured fixed-income investments provide opportunities for investors to achieve potentially higher yields with a consistent risk profile. There are also modern platforms, such as structured bond marketplaces like Grip Invest, which enable investors to discover curated fixed-income solutions that provide diversification and potentially an improved overall rate of return than would be produced through a bank deposit. Even though these are not as liquid as the demand deposits, they work extremely well as an emergency fund, for portfolio diversification, and attaining financial goals.

FAQs On Demand Deposits Vs FDs

1. What is the difference between a demand deposit and a fixed deposit?

Liquidity and interest rates are the key distinctions. Demand deposits can be withdrawn immediately but at a lower rate, whereas fixed deposits keep funds locked in for a given period in favour of a higher, more predictable rate of return.

2. Which is better: demand deposit or FD?

Neither is universally superior. Demand deposits are best suited for liquidity and emergencies, while fixed deposits are best suited for long-term savings and fixed income. This decision will depend on your financial objectives.

3. Are demand deposits risk-free?

In India, demand deposits are considered very low risk because they are regulated and insured up to 5 lakh per depositor per bank, making them one of the safest options for depositing short-term funds.

4. Can you break a fixed deposit before maturity?

Yes, most banks allow premature withdrawal of a fixed deposit. However, the bank usually charges a penalty and pays interest at a lower applicable rate for the period the money was held.

5. Do demand deposits and fixed deposits have tax implications?

Interest earned on both demand deposits and fixed deposits is taxable as per your income tax slab. For FDs, banks may deduct TDS if interest crosses the annual threshold unless exemptions are submitted.

6. Are fixed deposits and demand deposits safe in India?

Yes. Both are regulated by the Reserve Bank of India and insured by the Deposit Insurance and Credit Guarantee Corporation up to INR 5 lakh per depositor per bank, making them among the safest savings options.

References:

1. Airtel, accessed from: https://www.airtel.in/blog/fixed-deposit/demand-deposit-vs-fixed-deposit-which-banking-option-suits-your-financial-goals/

2. DICGC, accessed from: https://www.dicgc.org.in/FAQs

3. Ujjivan bank, accessed from: https://www.ujjivansfb.bank.in/banking-blogs/deposits/advantages-of-fixed-deposits-during-economic-uncertainty

4. Cleartax, accessed from: https://cleartax.in/s/liquid-funds-vs-fixed-deposits

5. Airtel, accessed from: https://www.airtel.in/blog/fixed-deposit/demand-deposit-vs-fixed-deposit-which-banking-option-suits-your-financial-goals/

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001