FII Outflows vs DII Support: The Anatomy Of India's May 2026 Market Moves

Indian markets in 2026 have turned into a tug-of-war between global caution and domestic confidence.

While FII investment in India has witnessed aggressive selling due to global uncertainties, strong domestic inflows from mutual funds and insurance players prevented a deeper market correction. The result was a surprisingly resilient market despite record foreign outflows.

What Are FII And DII?

Foreign Institutional Investors (FIIs), now commonly called Foreign Portfolio Investors (FPIs), are overseas entities that invest in Indian financial markets. These include foreign mutual funds, pension funds, sovereign wealth funds, hedge funds, and investment banks. Some of the biggest FII investors in India include global names such as BlackRock, Vanguard Group, and Government Pension Fund Global.

These firms are often counted among the biggest FII in India due to their large equity holdings and strong participation across Indian markets.

On the other side are Domestic Institutional Investors (DIIs). These are Indian institutions investing in domestic markets. Major DII companies in India include mutual fund houses, insurance companies, banks, and pension funds, all of which contribute significantly to long-term DII investment in India. Institutions such as Life Insurance Corporation of India and large AMCs play a major role in stabilising markets during volatile phases.

The activity of FII and DII in India acts as a market health indicator. The heavy foreign buying usually signals global confidence in India’s growth story, while strong domestic buying reflects growing retail participation and long-term faith in the economy.

The Scale of FII Outflows In 2026

The foreign portfolio investor India scale of selling in 2026 has been extraordinary. The FII in India pulled out nearly INR 1.92 lakh crore from Indian equities between January and April 2026, already exceeding the total outflows seen in all of 2025.1

The month of April, in 2026, alone witnessed outflows of INR 60,847 crore, while May continued the trend with selling crossing INR 70,000 crore in the secondary market.

The global factors that have influenced the FII investment in India:

- The rising US bond yields reduced the appeal of emerging markets.

- A stronger US dollar pressured capital flows into Asia.

- The escalating tensions in West Asia increased geopolitical uncertainty.

- The concerns over global tariffs and inflation added to risk aversion.

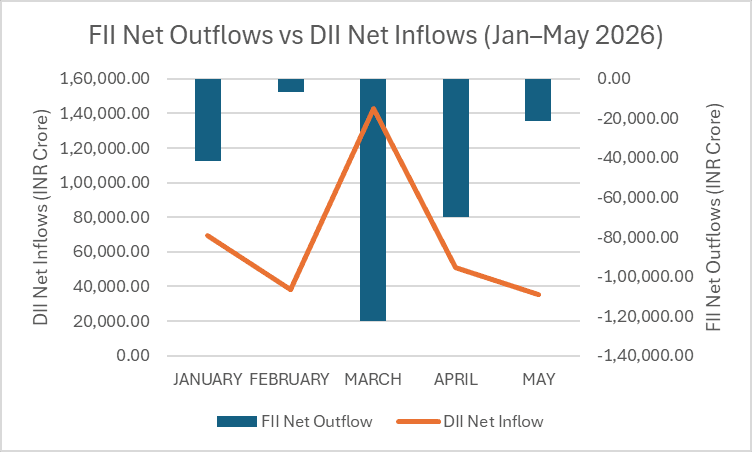

The following chart represents FII net outflows vs DII net inflows for the period January–May 2026 on a monthly basis:

DII Firepower: India's New Market Backstop

While FIIs sold aggressively, DII investment in India emerged as the market’s shock absorber.

The domestic institutional investor in India segment invested around INR 1.7 lakh crore during the same period, absorbing close to 90% of foreign selling pressure.3

A major reason behind this resilience has been India’s growing SIP culture, with the monthly equity SIP inflows crossing INR 30,000 crore in April 2026.4 This creates a steady stream of domestic liquidity into equities.

This shift has also changed market ownership patterns. While Foreign ownership in Indian equities has slipped to multi-year lows of 14.7%, the DII in India has overtaken the FII in India holdings for the first time. The reports indicate that DII holdings now stand above 18.9%. 5

This marks a structural transition in the Indian market, where domestic capital is gradually becoming the dominant force.

Day By Day: What Happened In May 2026?

On 8 May 2026, foreign investors remained cautious as FIIs recorded a net outflow of INR 4,110 crore. However, domestic institutions countered the pressure with net purchases worth INR 6,748 crore, helping the market maintain stability despite weak global sentiment.

The selling intensified again on 11 May when FIIs offloaded equities worth INR 8,437 crore. Even as foreign institutions reduced their positions aggressively, DIIs continued accumulating stocks and invested INR 5,939 crore, reflecting confidence in long-term domestic growth prospects.

By 12 May, FII selling moderated slightly, with net outflows standing at INR 1,959 crore. DIIs, meanwhile, strengthened their buying activity further with net inflows of INR 7,990 crore, reinforcing their role as a key support system for Indian equities during volatile market phases.6

During this volatile phase, the Nifty moved sharply between 24,176 and 23,379, while India VIX climbed to a high of 19.46, as of 12 May 2026, indicating rising fear in the market.7,8

The following table highlights day-wise FII vs DII activity for May 2026 (week of May 5–12):

Date | FII/FPI Net Purchase/Sale (in INR crore) | DII Net Purchase/Sale (in INR crore) |

| 12 May 2026 | -1,959.39 | 7,990.32 |

| 11 May 2026 | -8,437.56 | 5,939.65 |

| 08 May 2026 | -4,110.60 | 6,748.13 |

| 07 May 2026 | -340.89 | 441.07 |

| 06 May 2026 | -5,834.90 | 6,836.87 |

| 05 May 2026 | -3,621.58 | 2,602.62 |

Source: Money control,9

Why Did FIIs Sell? The Global Macro Picture

The reasons behind the FII exodus were influenced globally rather than being India-specific.10

- Hawkish US Federal Reserve: The US Federal Reserve maintained a hawkish stance, keeping interest rates elevated. The higher U.S. Treasury yields made dollar assets more attractive relative to emerging markets such as India.

- Rising crude oil prices: At the same time, crude oil prices surged above USD 100 due to tensions in West Asia. Since India imports a large share of its crude oil, rising energy prices created fears around inflation and trade deficits.

- Geopolitical uncertainty: Geopolitical risks further pushed investors towards safer assets. Many foreign investors reduced allocations to emerging markets as risk appetite weakened globally.

- Economic reopening of China: The partial reopening and improving economic outlook of China attracted global funds back into Chinese equities after years of underperformance. It reduced the allocations to India, where valuations remained relatively expensive.11

How Markets Held Up Despite The Selling?

One of the biggest surprises of 2026 has been the market’s resilience despite massive foreign outflows.

The Nifty largely managed to hold within the 23,000 to 24,000 range even during peak selling pressure. This stability came largely from sustained domestic participation.12

Financial stocks and IT companies were relatively supported because DIIs accumulated quality large-cap names during corrections.13

Retail investors also played an important role through SIPs with investments of INR 38,440 crore into equity-oriented mutual funds in the month of April. Unlike previous cycles where panic selling dominated, long-term retail flows continued steadily.14

For example, a retail investor investing INR 500 every month through SIPs during the correction phase would have accumulated more units at lower prices. This rupee-cost-averaging effect can improve long-term returns if markets recover later.

The growing participation of domestic investors is changing the nature of Indian markets from being heavily foreign-driven to increasingly domestically anchored.

Fixed Income As A Hedge

Such periods of equity volatility often increase interest in fixed-income instruments.

During phases of heavy foreign portfolio investor India outflows, many investors shift towards bonds, NCDs, and securitised debt for relatively stable returns and lower volatility.

Platforms such as Grip Invest provide access to curated fixed-income opportunities that may help investors diversify beyond equities during uncertain market phases, with a minimum investment of INR 1,000, and fixed returns ranging from 8% to 12.5%.15

A DII-driven market environment helps in stabilising debt demand because domestic institutions continue participating actively across asset classes, supporting corporate bond markets and yields.

Conclusion

The market movements in May 2026 reflected a changing balance within Indian equities. While heavy FII selling created short-term volatility, strong domestic participation prevented deeper market weakness.

Additionally, the rise of SIP inflows and the growing dominance of the DIIs highlight how Indian markets are becoming increasingly supported by local capital rather than depending entirely on foreign institutional flows.

FAQs On FII Outflow vs DII Support

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001