Fiscal Policy vs Monetary Policy: How They Shape India’s Economic Growth

When you zoom out and look at what truly drives an economy’s direction whether prices rise, borrowing gets cheaper, or markets pick up steam, it all comes down to two powerful levers: fiscal policy and monetary policy. Together, they form the foundation of macroeconomic management.

Fiscal policy, crafted by the Ministry of Finance, focuses on how the government earns and spends money through taxation and expenditure. Monetary policy, steered by the Reserve Bank of India, works in parallel to maintain price stability and support sustainable growth. While they serve different purposes, both policies ultimately shape the investment landscape that influences every Indian investor.

For an investor, it is important to understand how these policies influence market movements because they not only provide short-term growth opportunities but also set a tone for a particular period. Investors having a long-term outlook should have a clear idea about the implications of fiscal and monetary policy on portfolio management and investment as a whole.

Understanding Fiscal And Monetary Policy

Investors often talk about fiscal and monetary policies, especially when there is a change in these that has a direct implication on the market movement. For instance, the recent change in repo rate had sent markets into a bullish mode, even when the geopolitical situations were not too favourable. Let us understand the two concepts.

Fiscal policy is driven by the Finance Ministry and uses tools such as government spending, taxation, subsidies, and capital expenditure to support growth and employment. These fiscal policy tools help shape long-term development and demand.

Monetary policy, controlled by the RBI, focuses on price stability by adjusting interest rates, liquidity, and the money supply. Its monetary policy tools influence inflation, credit availability, and financial stability. Together, these frameworks guide consumption, borrowing costs, and overall economic momentum in India.

Key Differences Between Fiscal And Monetary Policy

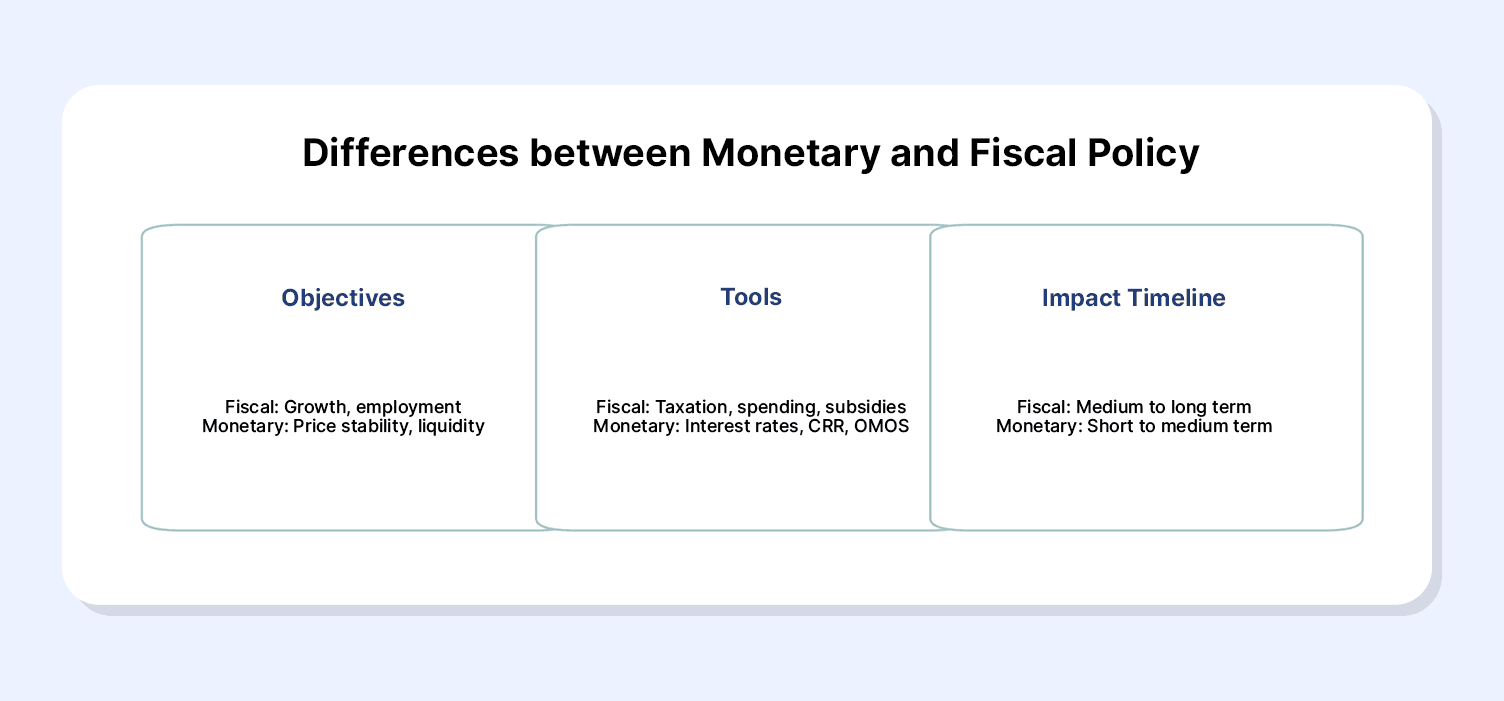

Fiscal policy and monetary policy differ fundamentally in who controls them, the tools they use, and the speed at which they influence the economy. Fiscal policy, driven by the Ministry of Finance, relies on taxation, government spending, subsidies, and capital expenditure to steer demand and support long-term development. Because fiscal actions require budget approvals and political consensus, their impact unfolds gradually, shaping employment, infrastructure creation, and structural growth over a medium- to long-term horizon.

In contrast, monetary policy, managed by the Reserve Bank of India (RBI), operates with significantly more agility.

It is a combination of repo rate adjustments, liquidity operations, cash reserve requirements, and open market operations that directly affects borrowing costs, credit conditions, and inflation expectations. Monetary actions transmit faster through the financial system, influencing interest rates, loan demand, and market sentiment in the short to medium term.

Here is a summary of the differences between monetary and fiscal policy from the Indian economy’s perspective:

How Fiscal And Monetary Policy Work Together In India

The authorities issuing monetary and fiscal policies are distinct, but the overall effectiveness depends on the coordination between the two. The Ministry of Finance drives fiscal decisions through taxation, capital expenditure, and welfare spending, while the RBI manages monetary policy by adjusting interest rates, liquidity, and credit conditions. Individually, each influences the economy differently, but together they determine how well India balances growth and inflation.

For example, if the government decides to increase capital expenditure for stimulating economic activity, the central bank needs to assess if the additional demand will result in an increase in inflation. In case the RBI finds that the action can result in increasing inflationary pressure, it may tighten liquidity or raise policy rates to maintain price stability.

This synergy is essential because India’s economic priorities often shift quickly. Growth-focused fiscal interventions require supportive monetary conditions to transmit effectively into investment and credit expansion. It is critical that both policies work closely together, even though these are issued by different apex bodies.

Also Read: Fiscal Deficit India 2025

Real-World Examples (Post-COVID India)

In the post-COVID scenario, there are clear fiscal policy examples from India and monetary policy examples in India that show how both frameworks work together to support recovery. From the fiscal side, the central government has introduced a range of packages (such as the Atmanirbhar Package), expanded capital expenditure, offered credit guarantees to MSMEs, and used fiscal policy taxation measures and subsidies to revive demand. There was a recent change in the GST regulations (GST 2.0) where tax rates were dramatically cut down to stimulate demand.

These fiscal policy tools helped stabilise employment, strengthen consumption, and build long-term capacity through infrastructure spending and PLIs. Coming to the monetary policy tools, the RBI had recently reduced the repo rate by 50 basis points (at 5.50%), which coincided with the fiscal decisions by the government.

As inflation pressures rose post-2022, the RBI reversed course by increasing monetary policy interest rates to anchor price stability. This is one of the reasons why the country has experienced one of the lowest inflation rates in years, as the two policymakers have worked in perfect coordination.

A key outcome of this coordination was reflected in bond yields. While higher fiscal borrowing placed upward pressure on yields, the RBI’s liquidity operations helped moderate volatility.

For investors, this interplay created opportunities in high-quality fixed-income products, an area where platforms like Grip curate structured yield-focused options. These could be an excellent addition to your portfolio, especially when you are looking for low-risk alternatives that provide a consistent return.

Conclusion

A healthy balance between fiscal and monetary policies is essential for maintaining economic growth, controlling inflation, and ensuring steady market expansion. Fiscal policy contributes to long-term development by building capacity and supporting productive sectors, while monetary policy stabilises prices, interest rates, and credit availability. When both move in harmony, India is better equipped to handle fluctuations in demand, inflation pressures, and capital flows, creating a stable, growth-oriented environment for investors.

For those looking to make informed, long-term investment decisions in such an evolving macroeconomic landscape, exploring reliable fixed income options can be a strong starting point.

Visit Grip Invest today!

FAQs On Fiscal Policy Vs Monetary Policy

1. What is the main difference between fiscal and monetary policy?

Fiscal policy is managed by the government and uses taxation and spending to influence economic growth, while monetary policy is managed by the RBI and uses interest rates and liquidity tools to control inflation and credit conditions.

2. Who controls monetary policy in India?

Monetary policy in India is controlled by the Reserve Bank of India (RBI) through the Monetary Policy Committee (MPC).

3. How do these policies affect inflation and interest rates?

Fiscal policy influences inflation through government spending and taxation, which can increase or reduce demand. Monetary policy directly affects interest rates and liquidity, raising rates to curb inflation and lowering them to stimulate borrowing and growth.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001