Food Inflation In India: Causes, Impact, And What It Means For Households

Food inflation in the country is more than just a macro-economic indicator; it is a reality that affects many families. As the prices of basic requirements such as vegetables, cereals, milk products, and pulses reached new highs, the effect took effect immediately and is impossible to escape.

Unlike other expenditure requirements, the requirement for food cannot be postponed; therefore, food-related inflation is the most sensitive and important indicator in the country's overall inflation measure.

The blog provides definitions of food inflation and its impact on India's economy, and discusses the major factors that cause it. We will also shed light on the effects of food inflation in India on savings and investment, as well as on general ways to preserve one's purchasing power in times of high inflation.

Why Food Inflation Hits Indian Households The Hardest

Food accounts for a disproportionately large share of household expenditure in India. According to official consumption data, on average, 35-40% of the total household spending goes toward food. The share is even larger for lower-income families and often remains a tad below 50%1. This condition makes Indian households far more vulnerable to food price shocks than households in the developed economies of Europe and North America, where food spending constitutes less than 15% of expenses2.

Recent years have pointed to this vulnerability. Even as headline inflation has remained moderate, sharp spikes in food prices, particularly vegetables and cereals, have put pressure on household budgets. For instance, a rise in the price of tomatoes or onions increases grocery bills by 15–20% in a month, reducing the headroom available for savings, healthcare, education, or discretionary spending.

Food inflation directly reduces the purchasing power of one-day wage earners and fixed-income families. Because food inflation is both immediate and recurring, unlike other forms of inflation, it remains the most emotionally and financially stressful economic pressure Indian families face.

What Is Food Inflation?

Food inflation is the rate at which the prices of food items rise over time. In India, it is measured as a component of the Consumer Price Index, via a component called the CPI food inflation, or the Consumer Food Price Index.

The main items included in the food CPI basket are :

- Cereals and cereal preparations

- Pulses and pulse products

- Vegetables and fruits

- Milk and dairy products

- Eggs, meat, and fish

- Vegetable oils and animal fats

- Sugar and spices

As food accounts for almost 39% of the overall CPI basket, a rise or fall in its prices has a strong bearing on the headline inflation rate3. Even if the prices of other items do not increase, a sharp rise in food prices sends the headline number upwards.

Put simply, when the inflation impact in India increases, households have to spend more money to buy the same amount of food, reducing real income.

Key Causes Of Food Inflation In India

Food inflation in India is driven by a mix of structural, cyclical, and policy-related factors.

1. Weather Dependency

Indian agriculture is too heavily reliant on the monsoon. An irregularity in rainfall, droughts, floods, or weather conditions at the wrong time of the year has an immediate impact on crop production. In fact, a good example is that vegetables are wasted due to excess rain; similarly, a weak monsoon reduces the production of cereals and pulses. More often than not, such supply shocks very rapidly translate into higher prices.

2. Supply Chain Disruptions

Inefficiency in storage, transportation, and distribution adds to food inflation in India. Fruits and vegetables are especially those that suffer from poor cold storage infrastructure, resulting in high wastage of these products. Food costs rise further due to transport disruptions, increases in fuel prices, and regional bottlenecks, even before the food reaches consumers.

3. Policy and MSP Impact

Government policies play a crucial role in the pricing of food items. Minimum support prices (MSPs) are designed to shield farmers from declines in their incomes, yet their continuous increases add to procurement costs and affect market prices. Restrictions on exports, import duties, and limits on stocks that are introduced to stabilise domestic prices may result in temporary anomalies.

How Food Inflation Affects Savings And Investments

Food inflation directly and indirectly affects household finances.

1. Decreased Disposable Income

With the rise in food costs, the savings amounts of the households have to be reduced. Take, for example, a middle-class family with a monthly income of INR 60,000. If the food expenses, due to inflation, increase from INR 15,000 to INR 18,000, the savings amount decreases by INR 36,000.

2. Impact on Real Returns

Food prices also impact the return on savings. For example, if a

fixed deposit is providing 6% return on the savings but the average food inflation rate India is 3-5% (which has been considerably lower in the past couple of quarters), then the actual return on savings is decreasing. This is even more detrimental to the person who takes a conservative approach when investing his savings.

Protecting Purchasing Power During High Inflation

Food inflation in India cannot be controlled, but it can be effectively managed through proper financial planning.

1. Role of Inflation-Beating Instruments

To maintain purchasing power, one requires investment instruments that generate returns in excess of inflation. Such instruments include inflation-indexed bonds, diversified mutual funds, and selected real assets.

2. Fixed Income Options with Predictable Cash Flows

However, not all fixed-income options are ineffective during a period of inflation. Some tools, like short-term debt funds, ladder portfolios, and tax-effective options, are able to provide stability and predictable income as well as help manage risk. The trick is to match investment decisions to inflation trends.

Conclusion

Food inflation in India is not just a headline number. It shows up every month in household budgets, quietly eating into savings and reducing financial flexibility. When a large share of income goes toward essentials like food, even small price increases can disrupt long-term plans, especially for families dependent on fixed or predictable incomes. What this really means is that ignoring inflation while planning savings and investments comes at a real cost.

The way forward is not to react emotionally to price spikes, but to plan with inflation in mind. Aligning savings with instruments that balance stability and inflation-adjusted returns becomes critical over time. Platforms like Grip Invest help investors explore regulated, fixed-return investment options that can complement traditional savings and support more resilient financial planning during inflationary phases.

With the right mix of awareness and disciplined investing, households can protect their purchasing power even when food inflation remains unpredictable

FAQs

1. Why is food inflation high in India?

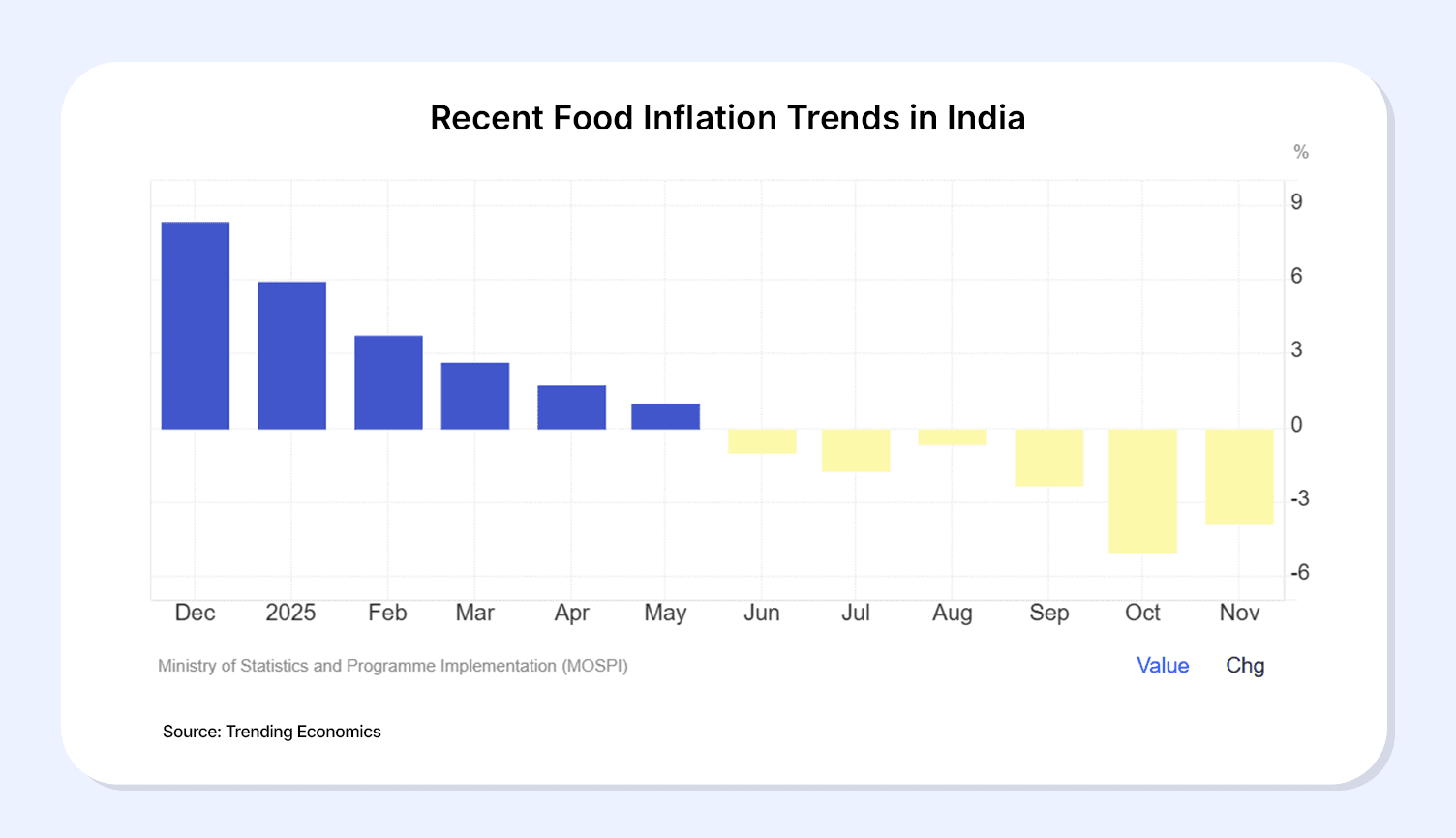

Food inflation in India is driven by reliance on monsoons, the unorganised supply chain, rising input costs, and government measures such as MSP increases. However, the food inflation rate has dropped considerably in the past few months and quarters.

2. What is the effect of food inflation on savings?

A higher food cost affects disposable income, resulting in less savings. Additionally, increased inflation will reduce the future value of any savings that may have been created.

3. Can investments safeguard against food inflation?

Yes. Investments that yield returns above inflation can help maintain the value of our purchasing power over time.

4. Are bonds a good investment during inflationary years?

Some types of bonds, such as short-term bonds and/or index-linked bonds, can be useful, but fixed-rate long-term bonds might fall short in high inflation periods.

References:

1. Money control, accessed from: https://www.moneycontrol.com/news/business/economy/households-spend-more-on-food-in-2023-24-but-its-share-remains-below-50-12899060.html

2. AJPM, accessed from: https://tinyurl.com/mr4xz5f9

3. PREPP, accessed from: https://tinyurl.com/45usd7b3

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001