Inflation-Indexed Bonds In India: Meaning, Benefits, And How To Invest

Inflation is one of the biggest motivations for investing, as the value of money declines each year. For example, something that costs INR 100 today may cost INR 105 a year later due to inflation, reducing your purchasing power. While saving and investing, your return on investment (ROI) should ideally exceed the prevailing inflation rate. However, aiming for higher ROI often comes with higher risk.

This is where Inflation-Indexed Bonds (IIBs) become valuable. These government-backed bonds are designed to protect investors from the erosion of investment value caused by inflation.

IIBs adjust their principal or interest payments in line with the prevailing inflation rate, ensuring stable real returns over time. Linked to benchmarks like the Consumer Price Index (CPI), they are a strong option for investors seeking lower-risk alternatives in high-inflation environments.

How Inflation-Indexed Bonds Function In Practice

Link Between Inflation And Bond Returns

IIBs operate differently from conventional bonds (which offer fixed payouts). These debt instruments’ returns are tied to the inflation rate, derived from the CPI (Consumer Price Index). The CPI is a measure of the average change in prices of baskets of goods and services over a given period.

When the inflation rate is rising, these inflation-protected securities increase the payouts to preserve the purchasing power. This means that the real return of the investment remains stable throughout the bond tenure.

On the other hand, when the inflation rate is low (or even in deflation), the adjustment is minimal, thereby ensuring that the investor is still shielded from erosion in investment value.

How Principal And Interest Are Calculated

In these bonds, either the principal amount, the interest payment, or both are adjusted periodically to reflect changes in the inflation index.

For example, if an investor holds INR 10,000 in IIBs and inflation for the year is 6%, the principal is revised to INR 10,600. Interest for the next period is then calculated on the revised principal, creating a compounding inflation-protection effect.

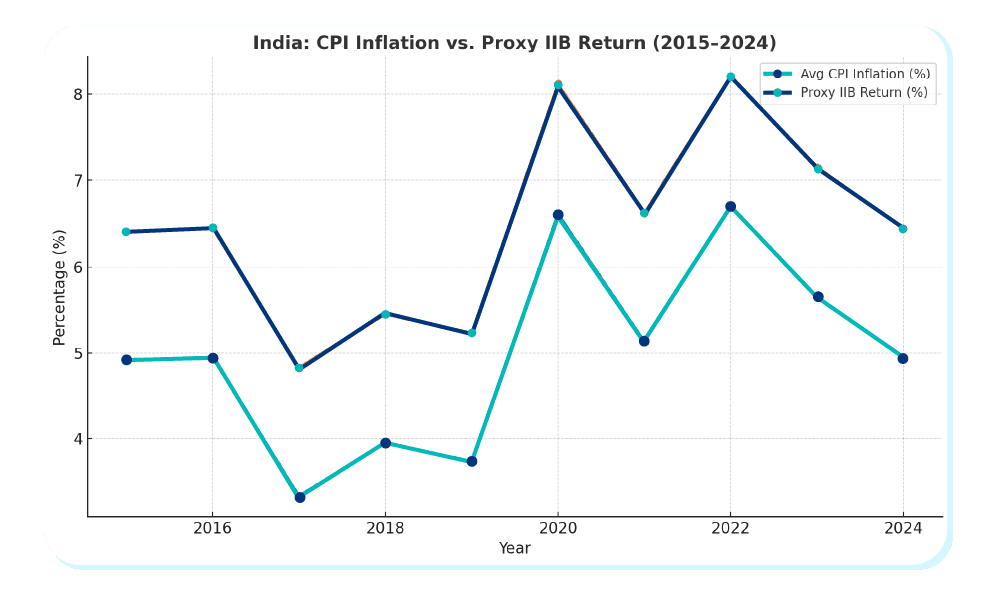

IIB Returns Vs. Inflation Rates (10-Year Period)

Here is a chart depicting the comparison between IIB Returns and Inflation Rates in the past ten years:

Figure 1.0: CPI Rate vs. Proxy IIB Return

Proxy IIB Return refers to the Rate of Return (ROR) on IIBs in India. As per the RBI’s clarification, there is no separate data about IIBs published1. As per RBI’s retail IINSS-C formula: fixed 1.5% + inflation, it is a clean proxy for what a CPI-linked bond’s nominal return would approximate. For CPI data, we have opted for the information published by the World Bank2.

The chart shows that RBI Bonds returns consistently stay about 1.5 percentage points above CPI inflation across 2015–2024, reflecting the fixed-plus-inflation structure that preserves real purchasing power.

Types Of Inflation-Indexed Bonds

1. Capital-Indexed Bonds

Capital-indexed bonds adjust only the principal value in line with inflation, while the interest (coupon) rate remains consistent. At maturity, the investor receives fixed income inflation protection through inflation-adjusted principal, ensuring that the real value of the investment is preserved. This type is particularly suitable for investors who prioritise capital protection over regular income.

2. Inflation-Indexed Savings Bonds

These bonds, such as India’s Inflation-Indexed National Savings Securities-Cumulative (IINSS-C), adjust both the principal and interest payments according to inflation. They typically pay a fixed rate (e.g., 1.5% p.a.) above the inflation rate (as discussed in the chart), ensuring a consistent real return. Interest is compounded periodically, making them ideal for long-term savers seeking steady growth with inflation-proof investments.

3. International Examples

Globally, similar capital-indexed bond instruments include the U.S. Treasury Inflation-Protected Securities (TIPS), which adjust the principal based on the Consumer Price Index (CPI-U) and pay interest semi-annually, and the U.K.’s Index-Linked Gilts, which link both principal and coupon to the Retail Price Index (RPI). Other economies, such as Canada and Australia, also issue inflation-linked bonds as part of their government securities portfolio.

Benefits Of Inflation-Indexed Bonds

1. Inflation Protection: The primary advantage is the protection offered against inflation, ensuring that the purchasing power of the investment is preserved.

2. Stable Real Returns: IIBs provide a more stable real rate of return (return above inflation) compared to traditional bonds, which can be eroded by inflation.

3. Low Risk: Typically issued by governments or top-rated entities, IIBs are considered safe investments with low default risk.

4. Diversification: They can enhance portfolio diversification by offering a unique asset class with a low correlation to other assets like equities.

Drawbacks Of Inflation-Indexed Bonds

1. Lower Starting Yields: IIBs generally offer lower initial interest rates compared to traditional bonds due to the added inflation protection feature.

2. Complexity: The adjustments to principal and interest payments can be complex for some investors to understand.

3. Tax Implications: Inflation adjustments to the principal may be considered taxable income in some regions, even though the investor may not receive this cash until maturity or sale.

4. Market Risk: IIBs are still subject to market risks such as interest rate fluctuations and shifts in inflation expectations.

Also Read: Demand and Push Inflation: What It Means For Investors in 2026?

How To Invest In Inflation-Indexed Bonds In India

Inflation-indexed bonds in India are primarily issued by the Reserve Bank of India (RBI) on the CG’s behalf. These can be accessed through primary auctions or purchased in the secondary market via banks, stock exchanges, or authorised dealers. RBI’s retail-focused product, the Inflation-Indexed National Savings Securities, Cumulative (IINSS-C), is available to resident individuals, HUFs, and select institutions and works as a great option for investors seeking investment in the RBI inflation bond scheme.

Availability And RBI’s Role

The RBI determines the issue size, auction process, and inflation benchmark (typically CPI). It also ensures periodic adjustment of principal and/or interest in line with inflation.

Steps To Purchase

- Open an account with a bank or demat service provider linked to RBI’s e-Kuber platform or a recognised exchange.

- Participate in RBI auctions (for institutional/large buyers) or buy through stock exchanges (for retail).

- Pay the issue price; bonds are credited to your demat account.

Minimum Investment And Tenure

For IINSS-C, the minimum investment is INR 5,000, with multiples of INR 1,000 thereafter, and a tenure of 10 years3. Institutional bonds may have different terms. Interest is typically compounded half-yearly and paid at maturity or periodically, depending on the product structure.

Conclusion

Inflation-indexed bonds offer a reliable way to safeguard wealth from the silent erosion caused by rising prices. By linking returns to inflation, they ensure that investors maintain their purchasing power while earning a modest real yield. Products like the RBI’s IINSS-C make this asset class accessible to retail investors, while global equivalents like TIPS and index-linked gilts highlight their broader relevance.

For those seeking portfolio stability and predictable, inflation-adjusted growth, IIBs present a prudent choice for investment in government securities. However, as with any investment, assessing one’s risk tolerance, time horizon, and market conditions remains essential before committing funds. To learn more about Inflation-Indexed Bonds, log in to Grip Invest today.

FAQs On Inflation-Indexed Bonds

1. Are inflation-indexed bonds a good investment in India?

Yes, they are suitable for conservative investors seeking protection against inflation. They help preserve real purchasing power and offer predictable, inflation-adjusted returns, though liquidity can be limited.

2. How are inflation-indexed bonds taxed?

There is no special tax exemption for these bonds4. The interest is taxable as per the investor’s slab rate, and any capital gains are also potentially taxable, depending on prevailing tax laws.

3. Can retail investors buy inflation-indexed bonds directly?

Yes, retail investors can invest through products like the RBI’s IINSS-C via banks, demat accounts, or authorised exchanges, subject to minimum investment rules.

References:

1. RBI, accessed from: https://www.rbi.org.in/commonperson/English/scripts/FAQs.aspx

2. World Bank Group, accessed from: https://data.worldbank.org/indicator/FP.CPI.TOTL.ZG

3. RBI, accessed from: https://www.rbi.org.in/commonperson/English/scripts/FAQs.aspx

4. Bajaj Finserv, accessed from: https://www.bajajfinserv.in/what-are-inflation-indexed-bonds

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001