Types Of Inflation Explained: What Rising Prices Really Mean For Indian Investors

Imagine sipping your morning tea, only to notice the packet costs INR 10 more than last month. That's inflation at work—not just a price tag hike, but a silent thief eroding your savings and dreams of that dream home or retirement freedom. For Indian investors juggling EMIs, SIPs, and family goals, grasping the inflation meaning in India isn't optional; it's your first line of defense against losing real wealth1. This sets the stage for why different types of inflation demand tailored investment moves, as we'll explore next.

As prices climb, your fixed salary or FD interest buys less—bridging us to the core question: what exactly is inflation, and how does it ripple through everyday life

Inflation Meaning In India: The Basics Unpacked

At its heart, inflation measures how fast prices for essentials like rice, rent, and petrol rise, shrinking the rupee's buying power over time. The RBI tracks this via CPI inflation, targeting 4% with a 2% band, stepping in with rate hikes when it spikes—directly linking to the inflation and interest rates dance that affects your loans and deposits2.

But here is the twist: this average hides personal pain points, flowing naturally into why inflation feels like a heavier burden on your cost of living than headlines suggest3. Urban millennials paying sky-high rents or school fees often battle 7-8% "felt" inflation, even if CPI reads lower—pushing us toward dissecting its varied types of inflation.

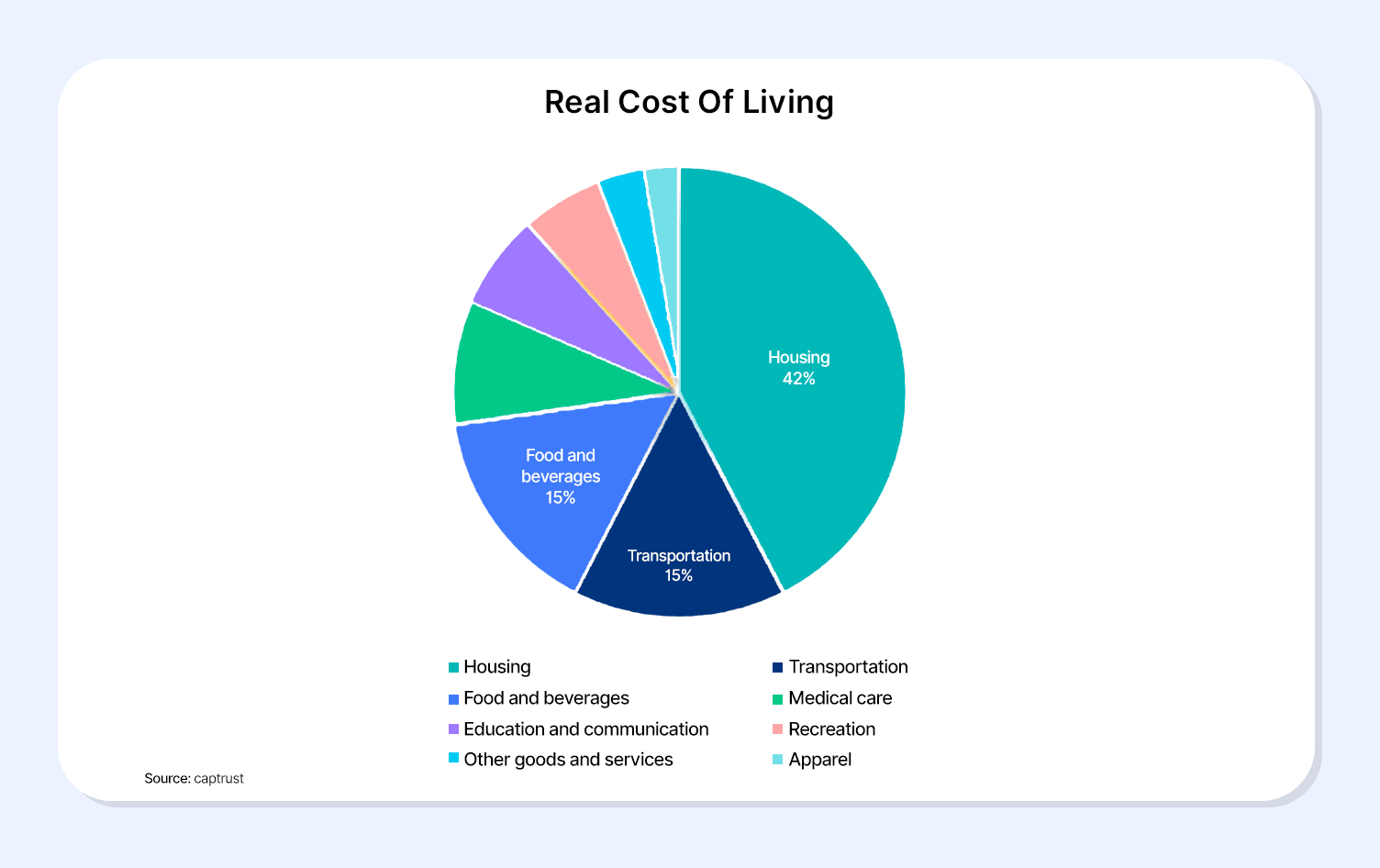

Inflation Vs. Your Real Cost Of Living

Headline inflation is the big number on news tickers, but your cost of living is the gritty reality: groceries up 10%, fuel jacking cab fares, and healthcare bills ballooning. Services like education often outpace the CPI basket, meaning a 5% salary hike feels like a pay cut if inflation hits 6%—a gap that demands savvy investing4.

Source: captrust5

This disconnect explains why investors must chase real returns (nominal minus inflation), teeing up our deep dive into types of inflation that fuel these mismatches. From demand surges to supply shocks, each type hits your portfolio uniquely, as the next sections reveal.

The Spectrum Of Types Of Inflation

Types of inflation ar not one-size-fits-all; they are like weather patterns—some bring growth rains, others destructive storms. Categorized by cause (demand-pull vs. cost-push), speed (creeping to hyper), or components (headline vs. core), they dictate RBI moves and market swings.

Starting with the growth-friendly one, demand pull inflation kicks off the chain reaction, pulling prices up as wallets open wider—and setting up why cost push inflation flips the script6.

1. Demand Pull Inflation: When Demand Outruns Supply

Picture Diwali markets buzzing—shoppers splurge on gold and gadgets, demand explodes, but factories can not keep up, so prices soar. That demand pulls inflation in action, fueled by booming incomes, festive spending, or RBI's low-rate stimulus7.

Great for early equity rallies as companies sell more, but if unchecked, it invites RBI rate hikes, transitioning us to cost push inflation where supply woes steal the show. In India, post-pandemic rebounds often sparked this, linking back to RBI's inflation and interest rates balancing act.

Also Read: Demand and Push Inflation: What It Means For Investors in 2026?

2. Cost Push Inflation: Supply Shocks Hit Hard

Flip the coin: global oil jumps to $90/barrel, truckers strike, or monsoons fail—input costs rocket, and producers pass the pain to you via higher veggie or petrol bills. Unlike demand-pull, this stagflation cousin squeezes profits without growth joy, forcing RBI to pick between curbing prices or sparking slowdowns8.

India's oil import reliance makes this a frequent villain, amplifying food woes and paving the way for structural inflation's deeper roots.

3. Structural And Food-Driven Inflation: India's Persistent Puzzle

Beyond shocks, structural inflation lurks in rusty supply chains—think farmer-to-fork delays causing onion prices to double overnight. Food's 46% CPI weight means tomato spikes derail RBI targets, blending into stagflation risks when growth stalls.

This chronic issue connects to headline vs. core debates, as volatile food masks stubborn service price creeps—urging investors toward hedges we will cover soon.

Also Read: Food Inflation In India

4. Stagflation: The Nightmare Combo Investors Dread

Worst of all Stagflation—sky-high prices with job losses and limp GDP, like 1970s oil crises. RBI faces a dilemma: hike rates to tame inflation and risk recession, or ease and ignite fires.

Tying back to prior types, it often stems from prolonged cost-push or structural woes, crushing broad markets and spotlighting why asset-specific impacts matter next.

5. Headline Vs. Core: Reading Between The Lines

Headline inflation swings with food-fuel drama; core strips them for the "true" trend in rents and meds. RBI eyes both—spiking core signals entrenched inflation and interest rates hikes, hurting long bonds first.

This clarity flows into our investment impact table, showing how these types of inflation reshape your portfolio.

Inflation's Grip on Investments: A Clear Table

There are different types of inflation rewrite asset rules—use this to rebalance and these are discussed below-

| Type of Inflation | Equities Impact | FDs Impact | Bonds Impact |

| Demand Pull | Revenue boost, but rate hikes cap gains | Rates rise, yet real yields lag | Prices dip on rising yields |

| Cost Push | Margins squeezed in input sectors | Erosion if rates do not match | Duration risk amplifies losses |

| Structural/Food | Rural stocks volatile | Steady nominal, poor real | Yield spikes on expectations |

| Stagflation | Broad pain, defensives shine | Nominal ok, real negative | Growth fears + inflation hurt |

| High Core | Valuations compress | Lagged rate upside | Short-term preferred |

The Inflation-Interest Rate Tango in India

RBI's repo rate is inflation's leash—hikes cool demand-pull fires but sting borrowers, boosting FD rates while denting bond prices. Recent FY25 forecasts at 4.8% underscore this link, flowing into hedge strategies. Understanding this repo rate–inflation dynamic is the first step—now let us translate it into action by Building Your Inflation Hedge in India.

Building Your Inflation Hedge in India

Inflation does not affect all assets in the same way. The key is to match investment types with the nature of inflation while avoiding over dependence on fixed deposits alone.

1. Match Assets to Different Types of Inflation

Not all inflation is driven by the same factors. Your portfolio should reflect this.

Demand pull inflation (strong consumption, rising incomes):

- Equities tend to perform better as companies pass higher costs to consumers

- Equity mutual funds and sectoral funds linked to consumption or banking can benefit

Cost push inflation (fuel, food, supply shocks):

- Short duration debt funds adjust faster to rising interest rates

- Inflation linked assets like gold help preserve purchasing power

This combination reduces the risk of relying on one inflation outcome.

2. Move Beyond Fixed Deposits for Inflation Protection

While FDs provide stability, post tax returns often struggle to beat CPI inflation in India.

- FDs are best used for capital protection, not inflation hedging

- Over exposure to FDs can lead to negative real returns during high inflation periods

Diversifying into inflation hedging assets can help maintain real wealth.

3. Add Inflation Hedge Assets to the Portfolio

Certain assets historically perform better during inflationary phases in India.

- Gold acts as a store of value when currency purchasing power declines

- REITs and InvITs benefit from rental income that often adjusts with inflation

- Commodities and energy linked funds offer indirect inflation protection

These assets also reduce correlation with equity markets.

4. Use Short Duration and Floating Rate Debt Strategically

Rising inflation usually leads to higher interest rates.

- Short duration funds reset yields faster compared to long duration bonds

- Floating rate instruments benefit from periodic coupon resets

- This limits mark to market losses during rate hike cycles

Such debt strategies improve stability in volatile inflation environments.

5. Consider Alternative Fixed Income for Real Returns

Alternatives can complement traditional debt by offering predictable cash flows.

- Lease backed and asset backed products offer relatively stable income streams

- Platforms like Grip provide access to alternative fixed income, which can exceed average CPI inflation over time

- These instruments are suited for investors seeking inflation adjusted income without equity level volatility

They work best as a portfolio diversifier rather than a replacement for core assets.

Conclusion

Inflation is not just an economic term you hear on the news; it is a real force quietly shaping your purchasing power, savings, and long-term goals. What really matters is understanding which type of inflation you are dealing with and how it affects different assets, from equities and bonds to FDs and alternatives. Once you see inflation this way, investment decisions become more intentional rather than reactive. That is where smart diversification and a focus on real returns come in.

Platforms like Grip Invest help investors look beyond traditional options and build portfolios that are better aligned with inflation realities, not just headline numbers. In an environment where prices keep rising, informed choices are what truly protect and grow wealth.

FAQs: Quick Wins on Inflation Worries

1. Which type of inflation is most dangerous?

Stagflation—growth stalls amid price surges, trapping RBI and tanking returns.

2. Does inflation reduce FD returns?

Absolutely—7% FD at 6% CPI nets 1% real; flip it, and you're losing ground.

3. Are bonds good during inflation?

Long ones no; shorts or floaters yes, especially with equity balance.

4. How can investors protect their portfolio during high inflation periods?

Focusing on assets that adjust faster to rising prices helps. Equities with pricing power, short-duration debt, gold, and alternative investments can offer better protection than long-term fixed returns.

5. Is inflation always bad for investors?

Not necessarily. Moderate inflation often signals economic growth and can support equity returns. Problems arise when inflation stays high without matching income or growth, which is why asset selection matters.

References:

1. Drishti IAS, accessed from:

https://www.drishtiias.com/daily-updates/daily-news-analysis/inflation-in-india-demand-vs-supply

2. PMF IAS, accessed from: https://www.pmfias.com/inflation/

3. Vajiram and Ravi, accessed from: https://vajiramandravi.com/upsc-exam/inflation/

4. Shri Ram Finance, accessed from: https://www.shriramfinance.in/articles/deposits/2025/fixed-deposits-still-a-worthwhile-investment

5. Cap trust, accessed from: https://www.captrust.com/resources/inflation-whats-in-the-basket/

6. Vedantu, accessed from: https://www.vedantu.com/commerce/difference-between-demand-pull-and-cost-push-inflation

7. Economic times, accessed from: https://economictimes.indiatimes.com/news/economy/indicators/rbi-mpc-meeting-inflation-forecast-india-rbi-governor-shaktikanta-das-rbi-raises-inflation-forecast-for-fy25-to-4-8-should-you-brace-for-higher-prices/articleshow/116029153.cms

8. Ecoholics, accessed from: https://ecoholics.in/rbi-monetary-policy-committee-meet-2024/

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001