How To Invest in Corporate FD: Step By Step Guide For Beginners

Introduction

Fixed deposits are one of the most sought-after investment choices for risk-averse investors in India. However, despite being an extremely safe investment option, the real rate of return (post-tax) can be extremely low, especially for the investors falling in the highest slab rate. As an investor, you might want an option which has the benefits of an FD but also provides you with enough returns to beat inflation.

In addition to learning how to invest in corporate FD, it is critical to understand the associated risks with corporate fixed deposits. This article will help you understand how corporate FDs work, their advantages and disadvantages, taxation, and a step-by-step guide on how to invest in corporate FD, especially through Grip.

What Is A Corporate Fixed Deposit?

A corporate fixed deposit safety is a fixed-income instrument offered by companies (NBFCs or corporates) where investors lend money for a fixed tenure in exchange for a predetermined interest rate.

How It Works

Suppose Company XYZ offers a 3-year corporate FD at 9% per annum. If you invest INR 1,00,000; you would earn INR 9,000 annually (before tax). At maturity, you receive your principal along with accumulated interest, depending on payout frequency (monthly, quarterly, cumulative).

Corporate FDs are governed by the Companies Act, 2013, and regulated by the Ministry of Corporate Affairs. NBFC deposits are additionally monitored by RBI.

Difference Between Bank FD And Corporate FD

Bank FDs are offered by banks and are insured up to INR 5 lakh under DICGC insurance. Corporate FDs are not insured. However, corporate FD interest rates are generally 1–3% higher than bank FDs.

For example (illustrative, Feb 2025 trend):

Large bank 3-year FD: 6.5%–7.0%

Highly rated NBFC corporate FD: 8.5%–9.5%

Higher return reflects higher credit risk.

Benefits and Risks Of Corporate FDs

- Higher Interest Rates

One of the main reasons investors look at the best corporate FD India options is higher yield. If inflation moderates around 5% and bank FDs offer 6.5%, a corporate FD at 9% significantly improves real return potential.

For example:

INR 5,00,000 invested at 6.5% earns INR 32,500 annually.

INR 5,00,000 invested at 9% earns INR 45,000 annually.

That’s INR 12,500 extra per year.

- Credit Risk Factor

Corporate FDs carry credit risk: the possibility that the company may default. Therefore, checking credit ratings (CRISIL, ICRA, CARE) is critical.

AAA-rated FDs carry lower risk than A-rated ones. Higher returns usually mean lower ratings.

- Liquidity Issues

Corporate FDs might come with a lock-in period. Early withdrawal may invite charges or may not be possible in the initial months. Investors should match their tenure, with their financial objectives.

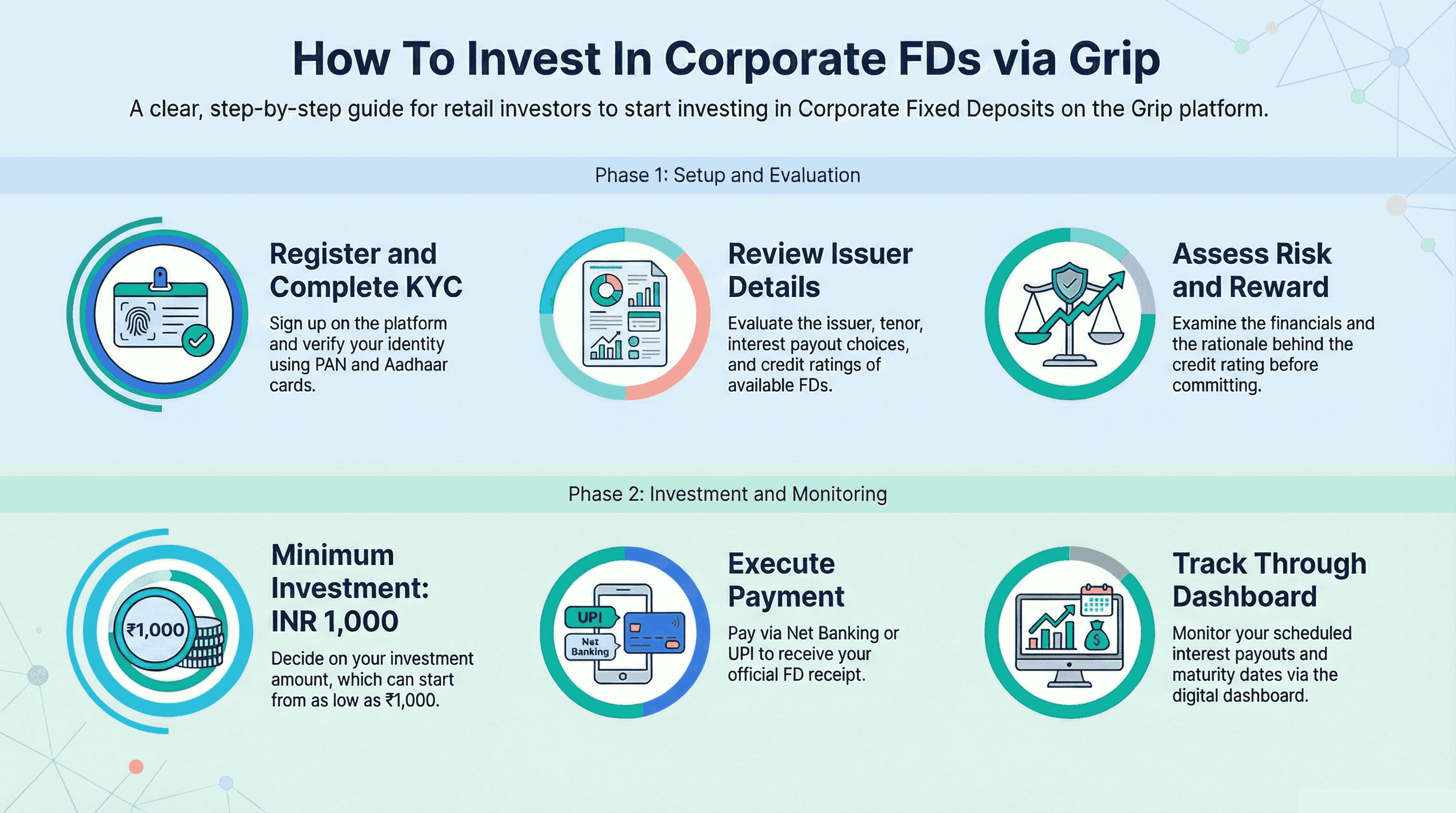

Step By Step Procedure To Invest In Corporate FD On Grip

Here's a basic guide on how to invest in corporate FD through an online investment platform such as Grip.

Step 1: Sign Up

Register yourself on the online investment platform and verify your identity to complete KYC; using PAN and Aadhaar cards.

Step 2: Look at the Corporate FDs Offered

Check the details of the issuer, the tenor, the interest payout choices, and the credit ratings.

Step 3: Assess Risk and Reward

Check financials, rationale behind the credit rating, and the conditions of interest payouts (monthly, quarterly, cumulative).

Step 4: Decide How Much to Invest

The minimum investment amount starts from INR 1,000

Step 5: Make Payment

Invest through net banking or UPI. After that, you will be issued an FD receipt.

Step 6: Monitor and Track

Interest payouts will be credited as per schedule. Monitor the maturity date through the dashboard.

It is always necessary to read the offer documents before making any investment.

Taxation On Corporate FD Returns

Corporate FD taxation in India is an important consideration.

Interest income is liable for taxation as, “Income from Other Sources” based on your applicable income tax rate.

For example:

If you fall under the 30% tax bracket and earn INR 45,000 interest annually, tax liability = INR 13,500 (excluding cess).

TDS is applicable if interest exceeds INR 5,000 per year (for NBFC deposits). You must report total interest in ITR even if TDS is deducted.

Unlike equity investments, there are no capital gains benefits.

Things To Consider Before Investing

- First, check the credit rating (of the issuer) carefully. Avoid chasing the highest rate without assessing issuer credibility.

- Second, diversify across issuers. Avoid putting all capital into one company FD.

- Third, match tenure with financial goals. Corporate FDs are suitable for medium-term allocation (1–5 years).

- Fourth, compare post-tax returns. A 9% FD may effectively become 6.3% post-tax - for someone in the highest slab.

- Fifth, assess liquidity needs. Ensure emergency funds remain in bank FDs or liquid funds.

Conclusion

Corporate fixed deposits can be a smart option for investors who want higher returns than traditional bank FDs while still staying within the fixed-income space. The key is balance. Higher corporate FD interest rates often come with higher credit risk, so careful issuer selection and diversification become essential.

Before investing, always evaluate the company’s credit rating, understand corporate FD taxation in India, and calculate your post-tax returns. A slightly higher rate may not always translate into better real returns once taxes and risk are considered.

If you prefer a more structured and transparent way to explore corporate fixed deposit opportunities, platforms like Grip Invest allow you to compare issuers, review risk details, and track investments digitally. With the right analysis and platform support, corporate FDs can become a meaningful part of a diversified fixed-income portfolio.

FAQs

1. Are corporate FDs secure?

Corporate FDs are quite secure if they are issued by highly rated companies; but they are not insured by the government like bank FDs.

2. What is the minimum investment amount?

The minimum amount of investment is typically between INR 10,000 and INR 25,000; depending on the company that issues the corporate FD.

3. How are corporate FD returns taxed?

The interest income is taxed according to your tax slab in the “Income from Other Sources” section. TDS will be applicable if the annual interest income exceeds a certain amount.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001