HRA Exemption & Calculation 2026: Rules, Eligibility, Benefits and Tax Savings

House Rent Allowance (HRA) is a common part of the pay structure offered to employees for meeting rental expenses. Moreover, it also comes with a potential tax relief.

The eligibility depends on the tax regime you prefer. The old regime allows a specific exemption on HRA, subject to conditions and limits. But under the new regime, this benefit is not available. Hence making the choice of regime an important decision for taxpayers.

Understanding the details behind the HRA tax benefit can lower your taxable income and provide meaningful savings each year. Now, let us dive into more details!

What Is HRA (House Rent Allowance)?

House Rent Allowance, commonly referred to as HRA, is a component of the compensation package offered by employers. It is meant to help employees meet housing expenses when they stay in rented accommodation.

The allowance is not uniform for everyone. It is influenced by factors such as the employee’s basic salary, the actual rent paid, and whether the residence is in a metro or non-metro city. These variations exist because the cost of living differs across regions.

HRA also provides a tax advantage under the old regime. The HRA exemption rules ensure that only a part of the allowance is taxable, giving employees relief if they satisfy the prescribed conditions.

What Is HRA Exemption And Its Eligibility Criteria?

Here, we will cover HRA for salaried individuals. HRA exemption is an amount deducted from your taxable income under Section 10 (13A), rule 2A of the Income Tax Act if you meet specific eligibility criteria1:

- You are a salaried individual.

- You have the HRA component in your salary.

- You are paying rent for a house you live in.

- You and your landlord have a valid rental agreement in your name.

How Much Amount Can You Claim For HRA Exemption?

You can claim HRA exemption that is the minimum of:

- Actual HRA received by your employer or

- Annual rent paid minus 10% of your salary or

- 50% of your salary if you live in a metro city, i.e. Delhi, Kolkata, Mumbai, and Chennai, while 40% is for non-metro cities.

The remaining amount of HRA will be a part of your taxable income. It is important to note that this calculation applies to HRA for salaried individuals under

Note: The "salary" mentioned above includes basic salary, dearness allowance and sales commissions. No other allowances are considered for the calculation of HRA exemption.

How To Use The HRA Calculator To Calculate HRA Exemption

Below is an HRA exemption calculator that will help you calculate your HRA exemption. This HRA calculator works following the above-mentioned income tax rules of section 10 (13A).

To ensure that you get the perfect results for your HRA exemption, provide the accurate information in the HRA exemption calculator as per the instructions mentioned below each parameter.

Example Of HRA Exemption Calculation

Mr X lives in Delhi and pays INR 20,000 per month as rent. He works as a salaried employee in Delhi, getting INR 40,000 as a basic salary and INR 15,000 as an HRA monthly.

Let us calculate the HRA deduction amount for Mr X using this information.

HRA Calculation Table:

Basis of Calculation | Calculation | Amount (INR) |

Annual HRA received | 15,000 × 12 | 1,80,000 |

Rent paid annually – 10% of basic pay | (20,000 × 12) – (40,000 × 12 × 10%) = 2,40,000 – 48,000 | 1,92,000 |

50% of basic pay (metro city) | 40,000 × 12 × 50% | 2,40,000 |

Exempted HRA | Lowest of the above | 1,80,000 |

The minimum amount is for "Actual HRA received" of INR 1,80,000, which you can deduct from your annual taxable income. In this case, there will be no remaining amount for tax exemption from HRA (HRA received).

You can also use a calculator by the Income Tax Department for an easy and quick estimate of the HRA tax benefit.

HRA Benefits Other Than Salaried Person

There might be a situation where your employer does not provide HRA, or you are a self-employed tax-paying individual.

In such a case, taxpayers can still claim a deduction through HRA for self employed category under Section 80GG (Income Tax Act) provisions if they pay house rent2. However, a taxpayer needs to fulfil certain conditions:

- You are salaried or self-employed.

- You have not claimed the HRA benefit at any time during the year for which you claim 80 GG. It means you are ineligible even if you received HRA for one month in the entire year.

- You and your spouse do not own a residential property in your workplace for employment.

To claim a deduction under this provision, an individual must file a declaration in Form 10BA. It includes rent details like the amount, landlord's name, etc.

Section 80GG- Amount Deduction Limit

The income tax department will consider the minimum of the following amounts for deduction:

- INR 5,000 per month, i.e. INR 60,000 per year

- 25% of total adjusted income

- Actual rent minus 10% of adjusted income

HRA For Salaried vs HRA For Self-Employed

Aspect | Salaried Individuals | Self-Employed Individuals |

Section | 10(13A) | 80GG |

Who can claim | Those receiving HRA as part of salary | Self-employed/ those without HRA, but paying rent |

Calculation | Least of: HRA received, rent paid minus 10% of salary, 50% of salary in metro or 40% in non-metro | Least of: INR 5,000 per month, 25% of adjusted income, rent paid minus 10% of adjusted income |

Key requirement | Must live in rented house, not owned property | Must file Form 10BA and not own residential property in place of work |

Things To Keep In Mind While Making HRA Tax Deductions

Here are a few points to consider for a deduction:

- You cannot claim deductions if you pay rent to your spouse.

- Submitting your landlord's PAN details is mandatory if you pay more than INR 1 lakh as annual rent.

- You can claim HRA even if you live with your parents by paying them rent.

- It would help if you deducted TDS of 30% when paying rent in case your landlord is NRI.

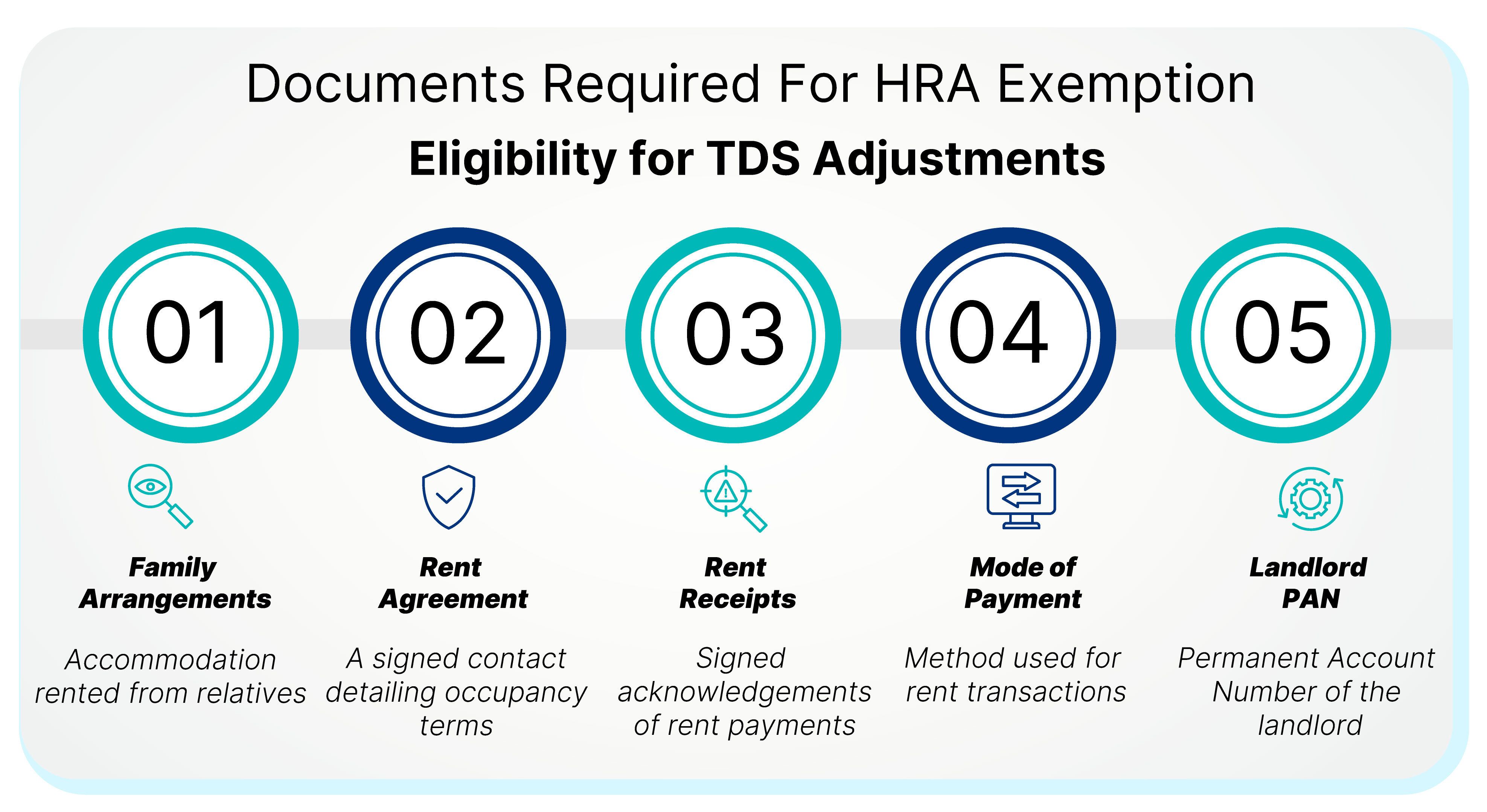

Documents Required for HRA Exemption

Supporting evidence is essential to establish eligibility. Organisations often request these papers before adjusting TDS and authorities may also review them during assessments.

1. Rent Agreement: A signed contract sets out the terms of occupancy and mentions critical details such as address, amount payable, and duration. When monthly outgo crosses INR 50,000, provisions for TDS deduction must also be included, as per Section 194-I (effective from April-2025)3.

2. Rent Receipts: Signed acknowledgements from the property owner serve as evidence of payment. Even if transfers are through electronic modes, these acknowledgements confirm the sum and the period covered.

3. Mode of Payment: Using bank transfer, UPI, or cheque creates a clear audit trail. Cash settlements above INR 2,00,000 are discouraged, as they may attract penalties under income tax law4.

4. Landlord PAN: When annual payout exceeds INR 1,00,000, the owner’s PAN- Permanent Account Number has to be furnished both to the company and in ITR filing. If your landlord doesn’t have a PAN, then he must provide a self-declaration confirming the same.

5. Family Arrangements: Accommodation rented from parents or relatives is permissible if the arrangement is genuine. A contract, acknowledgements, and visible transfer records are necessary, and the recipient must report the income in their annual declaration.

Conclusion

Maximising your HRA exemption isn’t just about tax savings, it’s about smart financial planning. By understanding the rules, eligibility, and documentation, you can reduce your taxable income and free up more resources for your goals. Whether you are salaried or self-employed, optimising HRA can make a meaningful difference in your annual finances.

To make the most of such opportunities and explore more ways to strengthen your financial planning, stay updated with Grip Invest.

Frequently Asked Questions On HRA Exemption

1. What is adjusted income in Section 80GG exemption calculation?Adjusted gross income, also known as (AGI), is defined as total income minus deductions or "adjustments" to your eligible income.

Adjusted income = Total income - long-term capital gain - short-term capital gain subject to tax at 10% - deductions under 80C to 80U* - income under section 115A or 115D.

*You should not include 80GG deduction in 80C to 80U. This adjusted income is before making a deduction under 80 GG.

2. Can you claim HRA if you are staying with your parents?

Yes, you can claim HRA by paying rent to your parents if:

- Your parents are the house's owner, and you are not the joint owner.

- You have proof of rent payments in the form of receipts. You should deposit the rent in your parent's bank account, preferably via cheque or online bank transfer.

- You have a valid rent agreement with your parents.

It is also essential to know that your parent's total income will include your rental income. It will be taxable under the category 'income from house property'.

In cases where a parent's income falls under a lower tax bracket than you, it can help save taxes for a family as a whole.

3. Can I claim both HRA exemption and home loan tax benefits together?

It is possible to use both, provided all the conditions are met. Suppose you are staying in rent and also paying interest on a loan for another property, both the claims can be considered. But what matters is that the property you own should not be the same one you live in on rent. In that case both cannot be claimed together.

4. Is rent receipt mandatory to claim HRA exemption?

Rent receipt is not mandatory for small amounts. If the annual rent is less than INR 36,000, receipts are usually not required. However, for higher rent, especially above INR 1 lakh a year, you have to share receipts, payment proof and the landlord’s PAN.

5. Can HRA exemption be claimed if rent is paid to parents or relatives?

Yes, HRA can be claimed, if the arrangement is genuine and backed by proper proofs. A written agreement, bank transfers and signed receipts strengthen the claim. The family member must also show the rent as income in their tax return. Without these, the claim may not hold up if scrutinised.

6. What is the difference between HRA exemption under Section 10(13A) and Section 80GG?

Section 10(13A) applies when your salary has a specific HRA component, and the relief depends on rent, basic pay, and city of residence. Section 80GG is meant for those who do not get HRA from an employer but still live in rented accommodation. The limits and conditions under 80GG are tighter, and you need to file a declaration to claim it.

7. How does the HRA exemption change under the old vs new tax regime?

Under the old regime, relief is available u/s 10(13A) for rent paid if your salary includes HRA. The calculation depends on rent, salary and location of stay. In the new regime, this benefit has been removed. No separate relief is allowed for HRA there.

References:

1. Central Board of Direct Taxes, accessed from: https://tinyurl.com/5bh7kjcz>

2. Central Board of Direct Taxes, accessed from: https://tinyurl.com/3kynjd7m>

3. Income Tax India, accessed from: https://tinyurl.com/3wu4zbwa

4. Income Tax India, accessed from: https://incometaxindia.gov.in/Tutorials/47.Disallowance-of-cash-expenses-or-limit-on-cash-transactions.pdf

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001