Inflation Vs Deflation: How Each Impacts Your Money And Investments

Characterised by falling and rising prices, inflation and deflation are two opposing forces that significantly impact the economic system of India.

When inflation occurs, prices rise gradually, eating away the value of your savings. When deflation occurs, prices decrease over time, resulting in an apparent lack of demand for goods and services.

Central banks also consider inflation as a means of securing price stability. This is done by finding a way to balance the opposing forces of inflation and deflation in their target rates.

In this blog, we will share specific examples that illustrate how inflation vs deflation are impacting both consumers' and investors, as well as the long-term growth of wealth.

What Is Inflation?

Market fluctuation and rising prices leads to inflation. It is when your money does not stretch quite and the purchasing power gets affected.

For example, the price of a loaf of bread is ten rupees today, but will be twelve rupees tomorrow, which means the increased cost has the potential of hurting consumers' ability to save money.

The method that central banks use to combat extreme inflation is to raise interest rates. This can lower inflation's effects on different assets, and will affect each type of asset slightly uniquely.

What Is Deflation?

Deflation is defined as a decrease in overall price levels. Your ability to spend money increases because everything is cheaper. If a loaf of bread was priced at 12 rupees yesterday and is now 8 rupees, your ability to purchase increases temporarily.

The negative impact of deflation economy effects can result in decreased economic growth due to consumers delaying purchases until the price drops further. Companies respond to declining sales by reducing staffing levels, which creates a cycle of further decline.

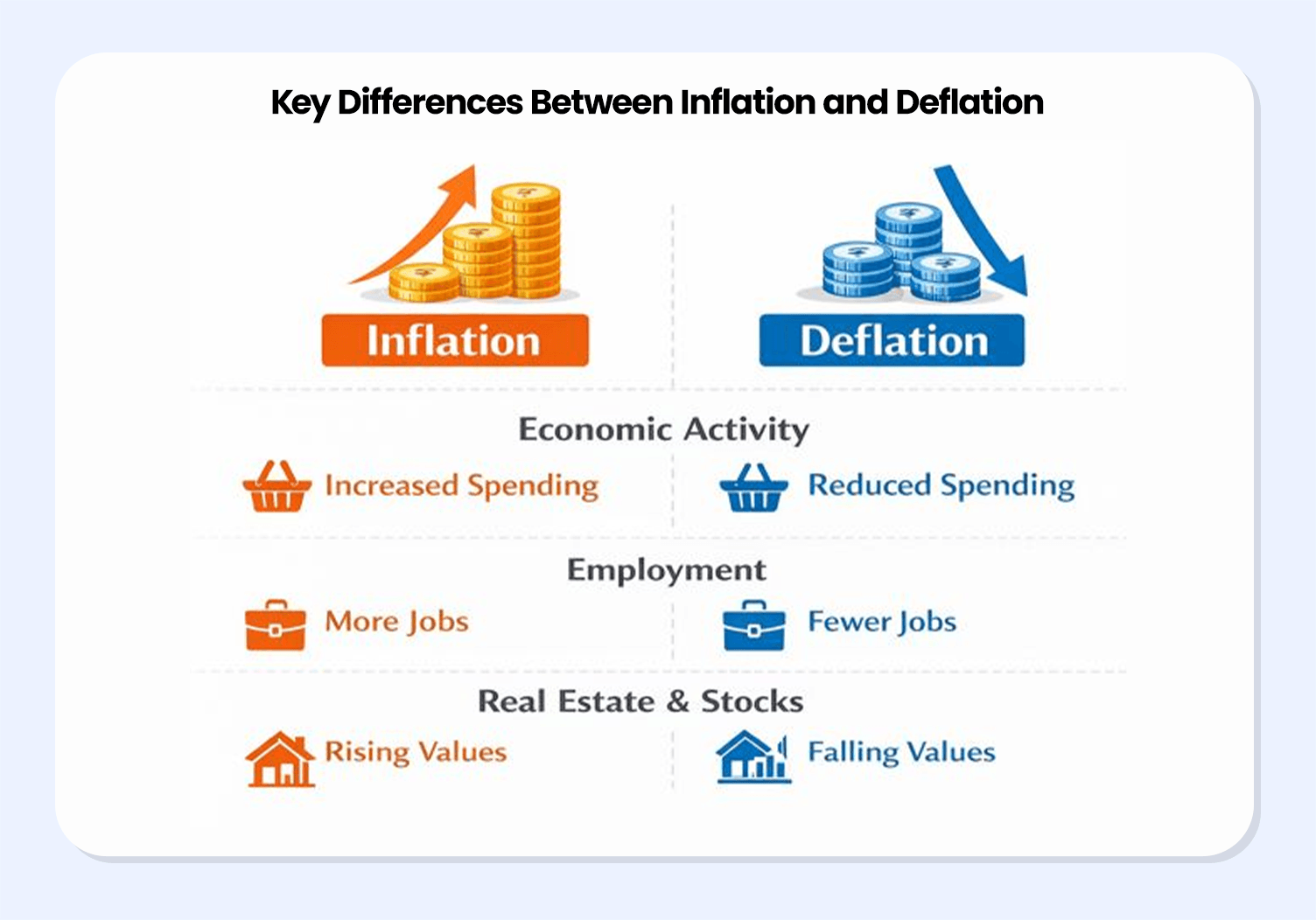

Key Differences Between Inflation And Deflation

As explained above, deflation is the opposite of inflation and provides opposite stimuli to the economy. Where inflation acts as an incentive to spend because of price increases, deflation creates a barrier to consumption.

The following breakdown illustrates deflation's impact on some of the main drivers of economic activity, but in layman's terms.

1. Economic Activity

Consumers will spend when their future debts will increase. When inflation exists, companies can anticipate higher prices and increase their output. Conversely, deflation leads consumers to postpone purchase until prices fall further, which negatively impacts the level of manufacturing as well.

For example, when inflation is mild, retailers will increase their inventory levels, while in the deflationary period, their shelves are full of stock but no customers.

2. Employment

Employment opportunities increase during inflationary periods as firms hire additional employees to meet higher customer demand and increase salaries. Conversely, during a period of deflation, firms experience a reduction in sales and must reduce their number of employees.

A worker who had a secure job due to an increase in demand may be discharged in a deflationary environment. Inflation creates and supports a more stable economy and helps to mitigate the negative impact of deflation on employment.

3. Real Estate and Stock Values

Inflation increases the value of both real estate and stocks due to rising costs. As a result, many investors in a deflationary economy will invest in growth stocks to offset the devaluation of their purchasing power inflation.

Conversely, during a deflationary economy, there will be an overall decline in the value of both homes and stocks due to a decline in demand. The effect of inflation on a home purchased at the peak of inflation will be much better than if it were purchased at a time of deflation.

| Aspect | Inflation Impact On Investments | Deflation Impact | Affected Groups |

| Consumers | Higher costs, less buying power | Cheaper goods, delayed purchases | Consumers lose short-term |

| Businesses | More sales, higher profits | Fewer sales, cost cuts | Businesses struggle |

| Investors | Stocks, property rise | Bonds gain, equities fall | Investors shift assets |

How Inflation and Deflation Affect Different Investments

Inflation and deflation affect investments differently. While stocks can perform well in inflationary environments, they typically perform poorly in deflationary environments. The opposite is true with fixed income assets. Here's how.

1. Fixed Deposits (FDs)

Fixed Deposits (FDs) provide a fixed rate of return over a predetermined period. The impact of inflation on your investment in terms of real returns is reduced to 0 when the interest earned from FDs is less than the rate of inflation. During deflationary environments, FDs perform better than any other fixed income asset class, since cash will grow in deflationary periods.

For example, a 7% FD will yield greater returns compared to a 5% return due to raised inflation but will outperform a 2% yield in a deflationary environment when inflation is raised. The inflationary rate affects the purchasing power of FDs for long-term investments.

2. Bonds

Bonds pay an interest rate which remains constant regardless of changes in the economy. Rising interest rates and dropping bond prices during inflationary cycles will negatively impact bonds, as investors will be able to purchase new bonds at higher rates, compared to older bonds. During deflation, bond prices increase since the yield goes down.

Imagine a 6% bond in an inflationary environment, it is better to own bonds than it is to buy new bonds with a yield of 5%. The control of inflation via the central banking system directly affects the prices of bonds. In deflation related events, the higher quality bonds will also be in greater demand.

3. Equities

Equities perform best in environments with moderate inflation because a company can easily pass any increase in their input cost(s) onto their customer(s). However, excessive inflation will harm the profitability of those companies.

Conversely, low demand will regress equity values when a company fails to convert sales into profits, as in the case of a technology company that has (grown) via the sale of products during an inflationary economic environment and has failed to continue selling products during a deflationary environment. In summary, equities are favoured in a growth phase of economic cycles.

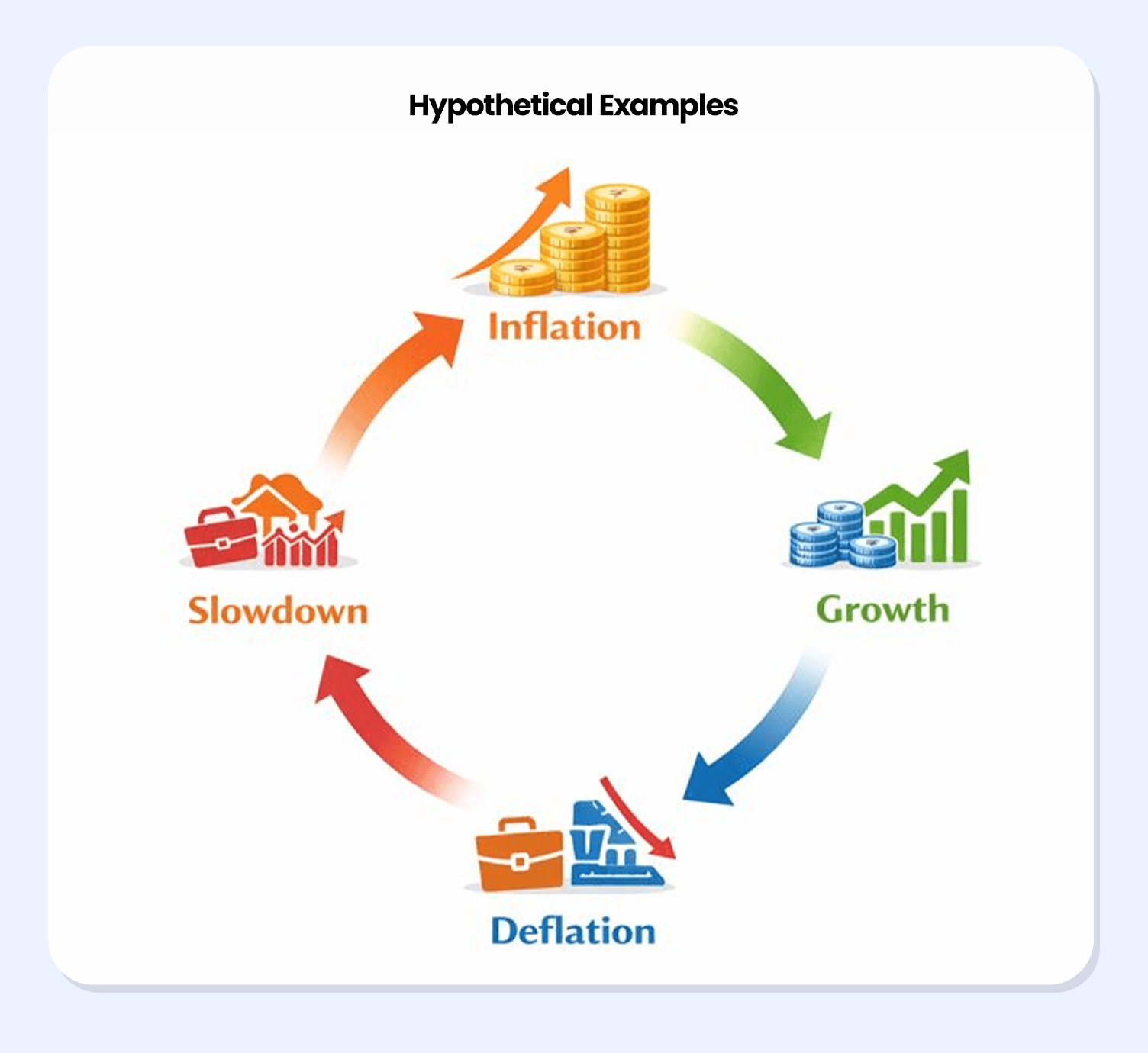

Hypothetical Examples

For instance, in 2010, India experienced a sharp inflationary phase, driven largely by rising food prices. This period of high inflation eroded the purchasing power of money, prompting investors to shift towards inflation hedges such as gold, which is traditionally viewed as a store of value during periods of rising prices.

As the cost of essentials increased, holding cash or low-yield savings became less attractive, reinforcing the move towards assets that could potentially preserve real value.

In contrast, during the global financial crisis of 2008, the dominant concern across economies was deflation. With demand weakening and prices expected to fall, investors preferred holding cash and highly liquid assets over riskier investments. In a deflationary environment, the real value of money tends to increase, making liquidity more attractive than asset growth.

To illustrate the impact on purchasing power, consider an investment of Rs 1 lakh. In an inflationary economy with 6% annual inflation, the real value of this amount would decline meaningfully over a five-year period, reducing what the investor can actually buy in the future. Conversely, in a deflationary scenario with -2% annual deflation, the same Rs 1 lakh would gain purchasing power over five years, allowing the investor to afford more goods and services despite earning no nominal returns.

Together, these examples highlight why maintaining a balance between inflation and deflation is critical for economic stability. Moderate inflation supports consumption, investment, and growth, while prolonged inflation or deflation can distort investment decisions and weaken long-term wealth creation.

Portfolio Strategy For Inflationary And Deflationary Phases

The economic cycles experienced by India usually account for the shifts between inflation and deflation. The best way to protect yourself from falling into either category is through diversification. This allows for risk dispersion among multiple assets.

- Stocks are generally the best asset class to use for long-term growth if you expect inflation, while more conservative assets, such as bonds, would provide the most protection during deflationary environments.

- It is advisable to have an equal amount of fixed deposits (FDs) and equity in your portfolio to create a balance between the two extremes of price increase due to inflation and price decrease due to deflation.

- You should also rebalance your portfolio every 12 months, as the central bank will change interest rates as part of their efforts to control inflation.

- Bonds by Grip provide a source of reliable, predictable income over the course of economic cycles, while the subtle advantage of these types of bonds becomes more apparent during economic turmoil.

The diversified investor who maintains a consistent portfolio of both bonds and stocks will be able to withstand the pressure created by a deflationary cycle better than an investor who is solely invested in stocks.

Conclusion

Inflation and deflation are inevitable parts of economic cycles, but their impact on your wealth depends on how prepared your portfolio is. Inflation slowly chips away at purchasing power, while deflation can stall growth and reduce income opportunities. The real risk lies in being overexposed to just one type of asset during either phase.

What this really means is that investors need balance, not predictions. A well-diversified mix of equities for growth and fixed income instruments for stability helps smooth returns across cycles. Platforms like Grip Invest make this easier by giving investors access to curated bonds and fixed income opportunities that offer predictable cash flows, especially during volatile or deflationary periods. When combined with long-term equity exposure, such investments help protect capital, maintain income, and build resilience no matter which way prices move.

FAQs On Inflation vs Deflation Impact On Investments

1. Is inflation always bad for investors?

No. Moderate inflation often supports economic growth and corporate profits, which can benefit equities and real assets. The problem arises when inflation becomes too high and starts eroding real returns.

2. Why is deflation considered more dangerous than inflation?

Deflation discourages spending and investment, slows business activity, and can lead to job losses. Over time, this weakens economic growth and reduces overall income levels.

3. Which investments perform best during inflation?

Equities, real estate, and inflation-linked assets tend to perform better during moderate inflation, as companies can pass higher costs to consumers.

4. How should investors prepare for both inflation and deflation?

The safest approach is diversification. A balanced portfolio of equities for growth and fixed-income instruments like bonds or FDs for stability helps manage risks across economic cycles.

References:

1. Investopedia, accessed from: https://www.investopedia.com/ask/answers/111414/what-difference-between-inflation-and-deflation.asp

2. Smart asset, accessed from: https://smartasset.com/financial-advisor/inflation-vs-deflation

3. Clear tax, accessed from: https://cleartax.in/s/inflation-deflation

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001