ITC Share Price Analysis: Dividends, Business Segments, And Growth Outlook

ITC Limited is a company that you have probably heard of, even in a casual follow up of the Indian stock market. ITC is a Kolkata based conglomerate listed under the ticker name ITC on both the BSE (500875) and the NSE, and is among the most heavily held and discussed stocks in the nation.

On any given trading day, ITC sees over 2 crore shares change hands on the NSE alone — as of March 2026, its 20-day average daily volume stands at approximately 2.09 crore shares , a testament to how deeply embedded this stock is in the Indian investor's portfolio.

ITC was established in 1910 and was known as the Imperial Tobacco Company of India Limited; the company has reinvented itself many times throughout the past century. It is much more than a cigarette company these days. It has activity in FMCG foods, personal care, hotels, agribusiness, paperboards and information technology - with it being one of the largest-caps that are structurally unique in India.

As of mid-March 2026, ITC's share price is around INR 306, approximately 42% below its all-time high of INR 528.50. The stock has seen a significant correction from its peak levels, driven by post-demerger earnings recalibration, sector rotation, and broader market headwinds.

The stock is also trading at a trailing PE of approximately 19x with dividend yield of more than 6% a combination that is still appealing to income oriented investors despite the correction.

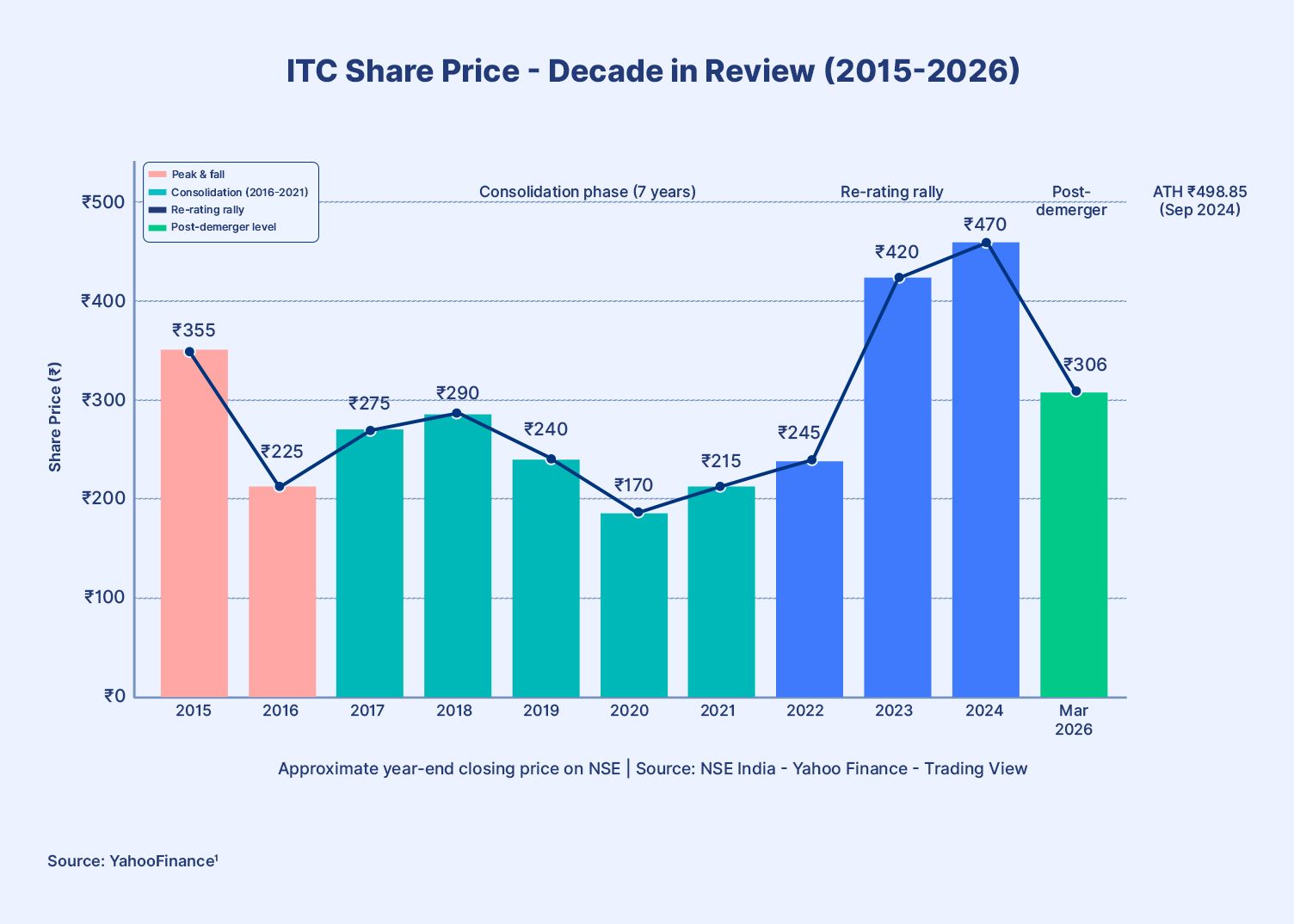

ITC Share Price Movement – Last Decade (2015–2026)

The chart above captures the dramatic arc of ITC's price journey, from INR 380 highs in 2015, a steep fall through GST-era fears, years of sideways movement, a sharp re-rating rally to INR 498, and the subsequent correction to current levels.

ITC Share Price History: A Tale Of Two Phases

1. The history of ITC Share Price: A two-phase Story.

The stock price history of ITC can be characterized as two wide periods, the first being a long and exasperating period of consolidation of almost seven years and then followed by a steep and decisive re-rating that would eventually see a record high.

- Long Consolidation Phase (2015-2022)

ITC stock reached its highest point of 355 in 2015 on a positive backdrop of high cigarette volumes and positive projections of growth in earnings. The structural overhang on the stock was however created by the introduction of GST in 2017 and consecutive increase in excise duties imposed on tobacco products. Between 2015 and 2020, the price of ITC was either in a INR 200-300 range, moving sideways yet Nifty 50 increased over 2 times more.

In March 2020, the COVID-19 crash saw the stock fall down to almost 170, its lowest in more than ten years. A large number of long term investors who had been holding till the consolidating stage were left to sit at massive losses.

- The Re-Rating Phase (2022–2024)

A sudden re-rating followed a set of factors in the end of 2022. To start with, the EBITDA margins within the FMCG segment continued to grow substantially with the input costs being moderated. Second, institutional investors started enjoying the multi-segment cash-generation machine at ITC anew.

Third, the demerger of the hotels was announced (finalized in January 2025) and this created hidden value. ITC stock has moved up as high as 498.85 in September 2024, an all time high of almost 2x up since the first days of 2022, less than three years ago.

Since the time the stock has been on a downward trend of about 39% since its high to its present value of around 306 as a result of sector rotation, world macro factors, and re-calibration of the post-demerger earnings.

ITC Share Price – Key Milestones (Approximate)

| Year | Approx. Share Price (INR ) | Key Event |

| 2015 | ~330–380 | Peak pre-GST; high investor enthusiasm |

| 2016 | ~200–250 | GST fears trigger sharp decline |

| 2017–2019 | ~240–310 | Consolidation; GST settled, slow re-rating |

| 2020 | ~155–200 | COVID-19 crash; touched multi-year lows |

| 2021–2022 | ~195–240 | Recovery; FMCG re-rating begins |

| 2023 | ~370–450 | Strong bull run; Hotels demerger buzz |

| 2024 (Peak) | ~498 | All-time high on NSE (Sep 2024) |

| Mar 2026 | ~306 | Post-demerger correction; near 52-wk low |

Source: MoneyControl2

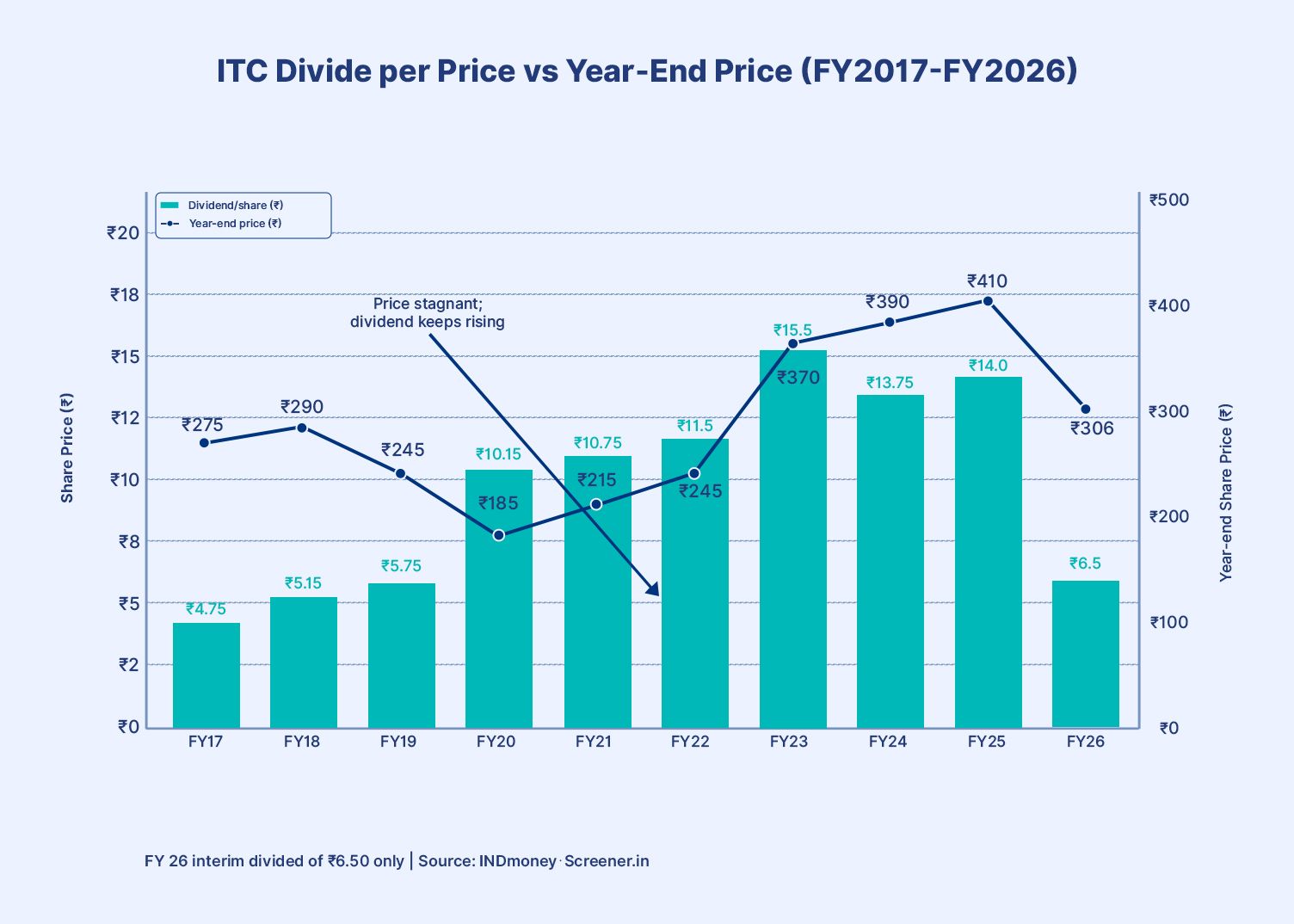

ITC Dividend Payout Vs. Share Price (FY2017–FY2026)

The chart above plots ITC's annual dividend per share (left axis) against its year-end share price (right axis).

Notice how dividends have risen consistently even in years when the price was stagnant — a key reason income-seeking investors continue to hold.

| Financial Year | Total Dividend/Share (INR ) | Approx. Dividend Yield (%) |

| FY 2016–17 | 4.75 | ~1.6% |

| FY 2017–18 | 5.15 | ~2.0% |

| FY 2018–19 | 5.75 | ~2.1% |

| FY 2019–20 | 10.15 | ~5.0% |

| FY 2020–21 | 10.75 | ~4.8% |

| FY 2021–22 | 11.50 | ~5.2% |

| FY 2022–23 | 15.50 | ~4.0% |

| FY 2023–24 | 13.75 | ~3.5% |

| FY 2024–25 | 14.00 | ~4.5% |

| FY 2025–26 (interim) | 6.50* | ~6.7% (trailing) |

Source: indmoney3

Why Investors Love ITC Stock

1 A Dividend Yield That Stands Out

At current ITC share price levels, the trailing dividend yield is approximately 6–7% — which is among the highest for a Nifty 50 large-cap stock. In the financial year 2022–23, ITC distributed a record INR 15.50 per share, and in FY2024–25, it paid INR 14 per share.

For context, FD rates at major banks hover around 6.5–7% currently — making ITC's dividend yield surprisingly competitive for a growth stock.

2 A Cash-Generating Business Machine

ITC's cigarettes segment — while often criticised. It is one of the most reliable cash generators in corporate India. The segment contributes approximately 78% of the company's PBIT (Profit Before Interest and Tax) while generating asset-light margins. This cash surplus is what allows ITC to fund its FMCG expansion, agribusiness investments, and substantial dividend payouts — all simultaneously

The company is essentially debt-free and has consistently generated strong operating cash flows. ITC's operating revenue for the trailing twelve months stands at approximately INR 79,800 crore, with a pre-tax margin of ~36% — exceptional by any industry standard.

3 ITC's Business Segments: A Diversified Empire

One of the most underappreciated aspects of ITC's investment case is the sheer breadth of its business.

Here is a snapshot of ITC's current segment structure:

| Business Segment | Key Brands / Operations | Revenue Share (H1 FY25) |

| FMCG – Cigarettes | Gold Flake, Classic, India Kings, Wills Navy Cut | ~42% |

| FMCG – Others | Aashirvaad, Sunfeast, Bingo!, Yippee!, Fiama, Savlon, Classmate | ~28% |

| Paperboards & Packaging | Bhadrachalam mills; specialty paper, packaging | ~13% |

| Agribusiness | Soya, wheat, spices, coffee, leaf tobacco exports | ~14% |

| Hotels (demerged) | ITC Grand Chola, ITC Maurya, Welcomhotel chain | Demerged Jan 2025 |

Source:Screener4

Such FMCGs as Aashirvaad (atta), Sunfeast (biscuits), Bingo! (snacks), and Yippee! (noodles) are now real category leaders. Aashirvaad is a brand with a market share of more than 30 percent in the branded packaged flour. Savlon is developed into one of the leading hand sanitisers and hygiene brands in India.

Risks And Future Outlook For ITC Share Price

1. Regulatory Risk in the Tobacco Sector

Regulation has been the elephant in the room of ITC investors. One of the most taxed items in the GST (28% + cess) is tobacco, and occasionally it is reported that it could be increased further. In early 2025, it was reported that ITC might have to increase the prices of cigarettes by 20-40 percent to cover higher levies a move that, although margin-accretive, would strain volumes.

Any large reduction in the volume of cigarettes would have a direct effect on the dividend-paying ability of ITC6.

There are also international ESG (Environment, Social, and Governance) stressors such that the large institutional investors and mutual funds are limited or deterred to owning tobacco stocks. This corporate headwind has damped off the PE multiple of ITC compared to the pure-play FMCG.

2. Growth in FMCG: The Long-Term Catalyst

The tobacco-free (FMCG) segment has the promising future growth potential of ITC. As revenue has increased by a CAGR of 12%+, and EBITDA margins widen (10 years ago the company recorded sub-2% margins, now it is 12-14%), the FMCG business of ITC is starting to resemble a real threat to Hindustan Unilever and Nestle India.

Analysts point out that this segment by itself may be worth INR 1-1.5 lakh crore in market cap in due course when it keeps expanding.

The paperboards and packaging market segment also shows an advantage of the booming e-commerce and consumer goods packaging demand in India and the agribusiness market is an unobtrusive but stable contributor to the package, which exploits the unparalleled rural last-mile penetration of ITC.

3. The Hotels Demerger: A New Chapter

ITC has been successful in demerging its hotels business to form a separate entity, ITC Hotels Limited, with effect of January 1, 2025. ITC shareholders received 1 share of ITC Hotels for every 10 ITC shares held BUT ITC retained 40% ownership of ITC Hotels, with the remaining ~60% going directly to ITC shareholders.

This de-values the hospitality business by the drag on valuation of the cigarette company and this may enable both parties to be assessed at their merit. There is a booming domestic travel and hospitality market in India which is favorable to ITC Hotels.

The basis of the earnings by ITC Ltd. after the merger with Demerger has been slightly recalibrated, and therefore this is one of the reasons the price has corrected so recently.

With the new structure digesting in the market within the next 2-4 quarters, a few of the brokerages have pegged a target of 380-440 on the parent stock.

ITC vs FMCG Peers: Share Price Performance And Valuation Metrics

| Name | EPS 12M | P/E | DIV YIELD % | 1YR RETURN % | MAR CAP RS CR |

| Hind Unilever | 64.01 | 47.29 | 1.85 | -3.01 | 516487.19 |

| ITC | 16.51 | 17.6 | 4.98 | -30.48 | 368115.77 |

| Hindustan Foods | 12.47 | 42.72 | 0.0 | -0.4 | 6514.93 |

| Godavari Bioref. | 0.69 | 43.2 | 0.0 | 8.24 | 1453.38 |

| Davangere Sugar | 0.06 | 69.24 | 0.0 | -42.43 | 587.73 |

Source: Screener

The company also offers the highest dividend yield making it attractive for income-focused investors. However, despite stable profitability, ITC delivered a weak 1-year return indicating negative market sentiment after the demerger and concerns about slower growth compared to premium FMCG peers.

Balancing Your Portfolio: Fixed Income Alongside Dividend Stocks

ITC is a very attractive dividend company, but there should not be a single investment bearing the entire burden of an investment strategy of the investor. The income-based investors especially those who are in or nearing retirement; will tend to value investing in high-dividend equities but with predictable fixed-income securities.

This forms a two- stream of income; one that takes part in the equity growth, and one that brings about some assurance irrespective of the market movement.

Here's why fixed income complements a dividend stock like ITC:

- Dividend payouts can be reduced or deferred in bad years, fixed-income returns are contractually defined

- While ITC's ~6–7% dividend yield is attractive, it comes with equity-level volatility; bonds and corporate FDs offer similar or higher yields with significantly lower risk

- Fixed-income instruments like corporate bonds and high-yield corporate FDs lock in returns, so even if ITC corrects 10–15% in a bad quarter, your fixed-income leg keeps generating income undisturbed

Platforms like Grip Invest offer curated access to SEBI-regulated corporate bonds and corporate fixed deposits from vetted issuers, allowing investors to build this fixed-income layer without needing to navigate complex bond markets on their own. For an ITC investor already earning ~6–7% in dividends, adding a 9–12% corporate bond alongside it creates a blended portfolio yield that is both higher and more stable.

Conclusion

ITC remains a unique mix of steady income and gradual growth, backed by strong cash flows and a diversified business model. While short-term movements in the ITC share price may continue due to regulatory risks and market cycles, its long-term story is anchored in FMCG expansion and consistent dividend payouts.

For investors, the key is balance. Relying only on dividend stocks may expose portfolios to sector-specific risks. This is where platforms like Grip Invest can play a role by offering access to curated fixed-income opportunities, helping investors create a more stable and well-diversified portfolio alongside equity investments like ITC.

FAQs On ITC Share Price Analysis

1. Is ITC a good dividend stock?

A: Yes, ITC is widely regarded as one of India's best dividend-paying stocks among large-caps. It has consistently grown its dividend over the past decade, and at current ITC share price levels (~INR 306), the trailing dividend yield is approximately 6–7%. The company's strong free cash flows from its cigarettes business provide a reliable funding base for dividends. However, investors should factor in the regulatory uncertainty around tobacco and the potential for stock price stagnation in the near term.

2. Why did ITC share price remain stagnant for years?

A: ITC's share price was stuck in a broad INR 200–INR 300 range from roughly 2015 to 2022 — a period of nearly seven years. The primary reasons were: (1) successive GST and excise duty hikes on cigarettes, which clouded earnings visibility; (2) a slow pace of FMCG margin improvement, making it hard to justify a re-rating; (3) ESG-related selling pressure from foreign institutional investors; and (4) the Hotels and Agri segments being viewed as capital-heavy drag businesses. The re-rating only began when FMCG margins improved and the Hotels demerger announcement offered value unlocking.

3. What businesses does ITC operate?

A: As of 2025–26, ITC Limited operates primarily in four segments: (1) FMCG – Cigarettes (largest profit contributor, ~78% of PBIT); (2) FMCG – Others (consumer brands like Aashirvaad, Sunfeast, Bingo!, Yippee!, Fiama, Savlon, Classmate); (3) Paperboards, Paper & Packaging (one of India's largest paperboard manufacturers); and (4) Agribusiness (agricultural commodity exports and sourcing). The Hotels business was demerged into a separate listed entity — ITC Hotels Limited — effective January 2025.

References:

1. Yahoo finance, accessed from: https://finance.yahoo.com/quote/ITC.NS/history/

2. Money control, accessed from: https://www.moneycontrol.com/india/stockpricequote/diversified/itc/ITC

3. IND money, accessed from: http://indmoney.com/stocks/dividend/itc-ltd-dividend

4. Screener, accessed from: https://www.screener.in/company/ITC/consolidated/

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001