Loan Against Fixed Deposit: How To Borrow Without Breaking Your FD

Borrowing against an existing fixed deposit is one of the simplest ways to raise cash without breaking your FD. A loan against fixed deposit lets you place a lien on the FD and access liquidity, typically up to 85–90% of the deposit, while the FD continues to earn interest.

Here in this blog, it explains how it works, when to use it, the loan against FD process, documents, and eligibility, plus a mandatory chart and table comparing rates versus personal loans1. (All rates/data below are referenced to Indian bank pages and market aggregators listed after the text.)

What Is A Loan Against Fixed Deposit, And How It Works

A loan against fixed deposit is a secured credit facility where the bank places a lien on your FD and lends you a percentage of its value (commonly up to 90%). You keep earning FD interest; you pay interest only on the borrowed amount.

For example, if you have an INR 1,00,000 FD and the bank offers 90% LTV, you can borrow INR 90,000 without prematurely breaking the FD. Many banks offer the facility as an overdraft (OD) or a demand loan. Typical bank terms show rates charged over the FD rate (e.g., loan against FD interest rate + 1% or +2%).

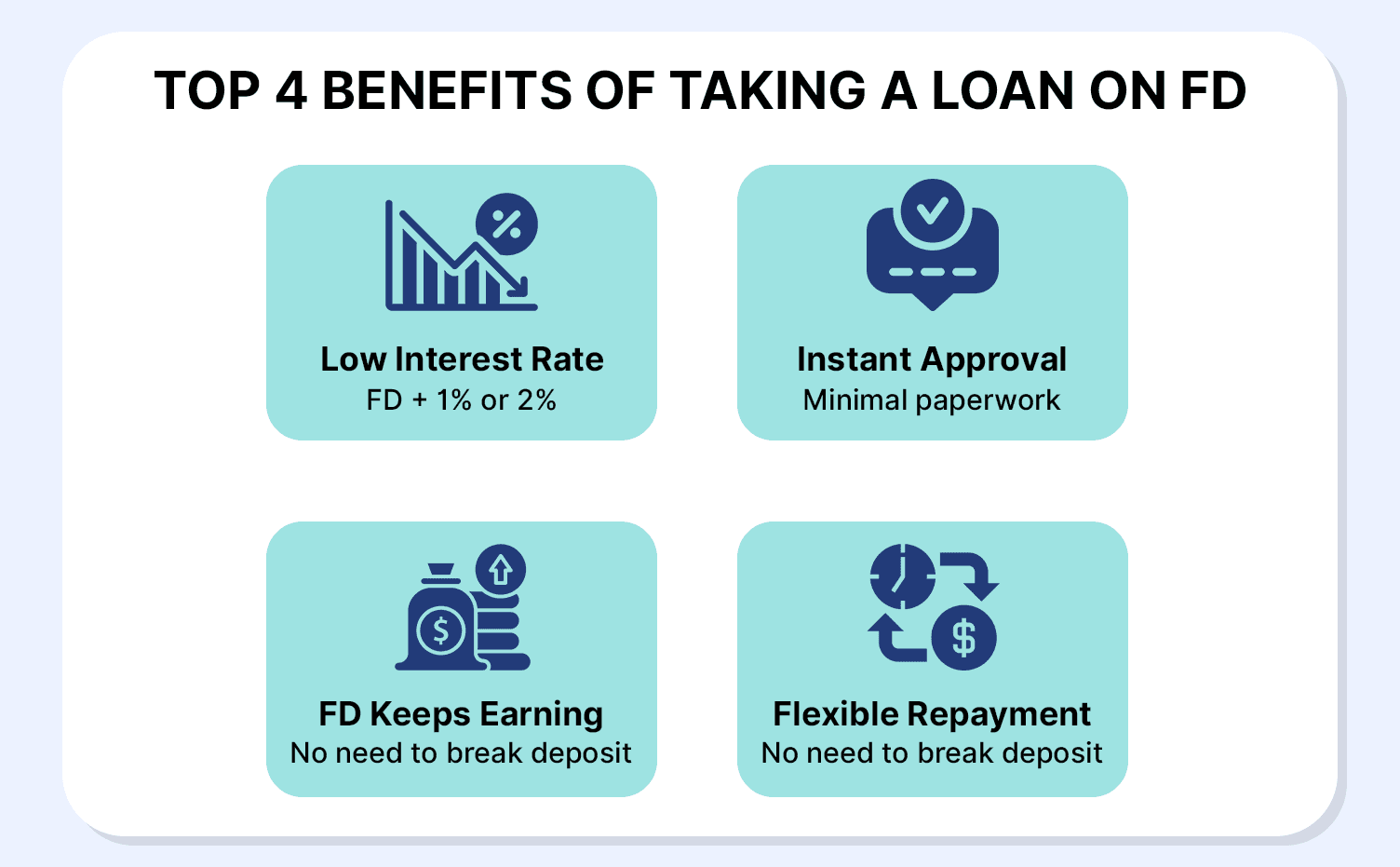

Benefits Of Taking A Loan On FD

Here are some loan against fixed deposit benefits:

1. Lower interest costs: Interest on a loan on FD is typically FD rate + a small margin (often 1–2%), so overall interest is much lower than an unsecured personal loan. For example, SBI charges ~FD rate + 1% while many banks charge FD rate + 2%2.

2. Quick approval and minimal paperwork: Since the FD is collateral, approvals are fast.

3. You keep earning FD interest: The deposit continues to accrue interest while the loan remains linked to it.

4. Flexible repayment: In some cases, banks will give overdraft facilities under which a certain amount of money will be paid interest only on the amount taken.

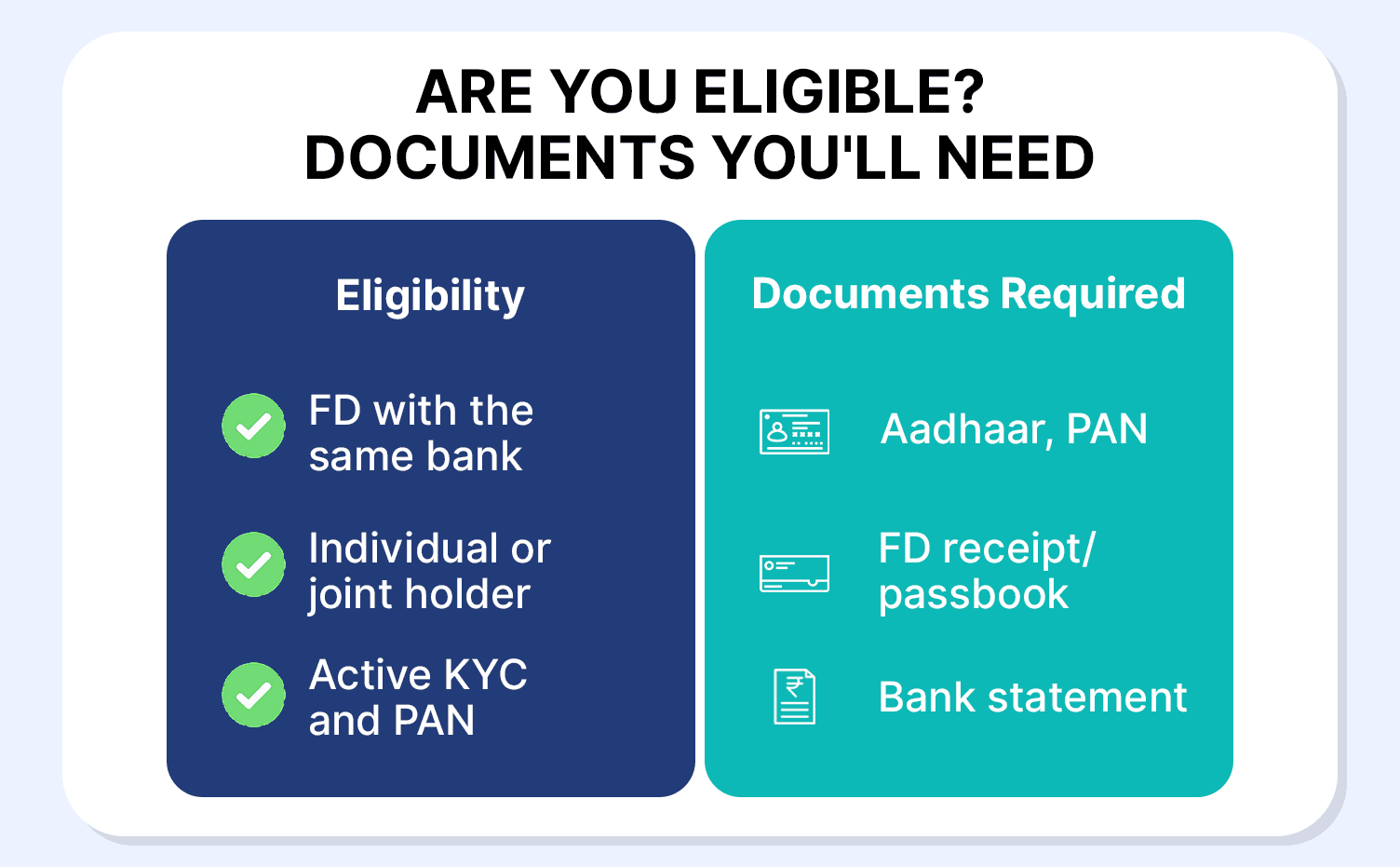

Eligibility And Documentation For Loan Against FD

Who can apply: Holders of eligible FDs (resident individuals, joint holders depending on bank policy). Many banks allow salaried and non-salaried customers as long as the FD is in the same bank.

Loan against fixed deposit documents required are mentioned below:

- Original FD receipt or passbook.

- KYC (PAN, Aadhaar).

- Account statement/proof of identity and residence (as per bank policy).

Loan against fixed deposit eligibility: FD should be through the bank in which the loan is taken, with a certain minimum period or minimum FD deposit (in many cases, the banks make an overly small minimum of just INR 5000). Digital platforms tend to have a maximum loan amount, which is usually up to 90% of the FD value3.

Repayment / Tenure: The loan against fd tenure is usually tied to the FD maturity. Overdrafts can remain until FD maturity; demand loans may require periodic payments. If you prepay or the FD matures before the loan is repaid, the bank will recover outstanding dues from the deposit.

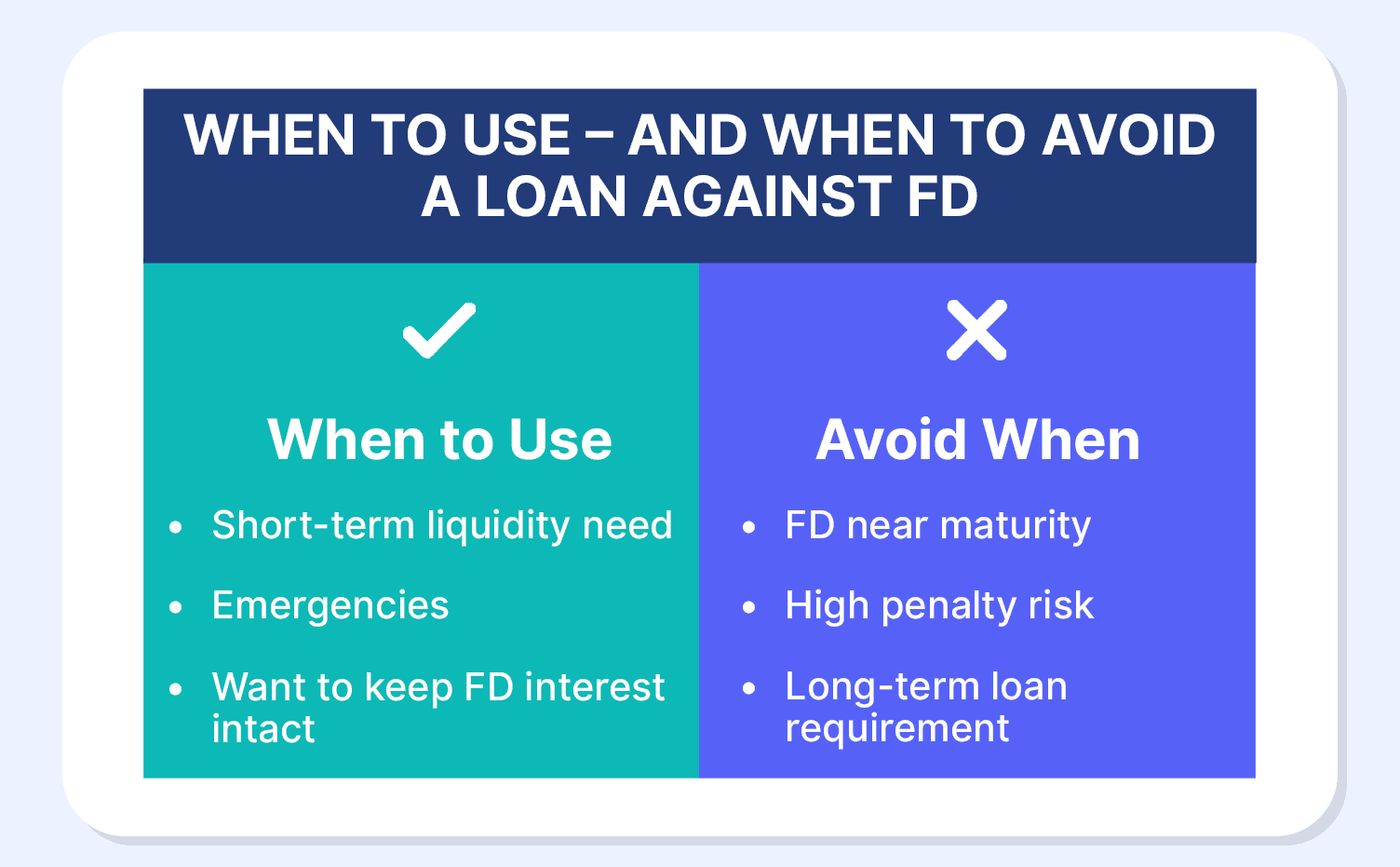

When To Use A Secured Loan Using FD, And When To Avoid

Good use cases:

- Short-term urgent cash requirements (medical, needed repairs).

- Debt consolidation occurs when the cost of borrowing through an FD is lower than the current loans.

- When you want to avoid breaking long-tenure FDs that have attractive rates.

Avoid if:

- FD maturity is near, and the penalty/interest difference is negligible.

- You plan to use the loan for long-term expenses, so consider structured loans with scheduled repayment rather than OD.

- If you have cheap alternatives (e.g., liquid funds with negligible exit load and you can sell them quickly).

Alternatives Worth Considering Before Taking a Loan Against FD

1. Liquid Mutual Funds or Short-Term Debt Funds

These funds can be a practical alternative when you need quick access to cash without breaking an FD.

- Liquidity: Many liquid funds now offer instant redemption (up to a limit) and settle the rest within 24 hours.

- Costs: No lock-in period and usually no exit load after seven days.

- Returns: While not guaranteed, they often deliver slightly higher post-tax returns compared to savings accounts.

- When it helps: Useful if you want to avoid pledging your FD or breaking it prematurely.

2. Personal Loans (For Strong Credit Profiles)

If you have a high credit score and stable income, a personal loan can sometimes be competitive.

- Interest rates: For top borrowers, personal loan rates can go as low as 10 percent to 12 percent, though this varies widely.

- Speed: Instant digital approval from many lenders.

- No collateral needed: You don’t have to compromise your FD or reduce its compounding timeline.

- When it helps: If your FD is locked into an attractive rate and you don’t want to disturb it.

3. Fixed-Income Marketplaces (If You Want Flexibility)

Platforms that curate fixed-income instruments can be useful—not as a direct replacement for an FD loan, but as a way to restructure your fixed-income portfolio for better liquidity and yields.

- Options: Corporate FDs, listed bonds, short-duration bonds, and high-quality debt products.

- Cost comparison: Always compare the total cost of borrowing vs the opportunity cost of breaking an FD vs reallocating into more liquid fixed-income options.

- When it helps: If you frequently face short-term liquidity crunches, shifting a portion of your fixed-income allocation to more liquid products can reduce your reliance on FD loans.

Conclusion

A loan against a fixed deposit can be a smart, cost-efficient way to access short-term liquidity without disrupting your returns. It keeps your FD intact, offers faster approval than most credit products, and typically comes with lower interest charges than unsecured loans. Just make sure to compare the effective rate (FD interest plus lender margin), evaluate the LTV offered, and account for any processing or foreclosure fees before making a choice.

For flexible, transparent, and easy-to-access fixed-income options, explore Grip Invest.

FAQs On Loan Against Fixed Deposit

1. How much loan can I get against my FD?

Typically up to 85–90% of the FD value, check bank-specific LTV (SBI/YONO lists up to 90%).

2. Is the loan against FD taxable?

Borrowing money isn't considered income for tax purposes. If you take out a loan for personal reasons, you can't deduct the interest you pay on it. The tax rules can be different if funds are being borrowed for business purposes or when the loan is used for generating investment revenue. Indeed, it is generally recommended to seek advice from a tax consultant.

3. Do I lose interest if I take a loan on an FD?

No, in case of an OD loan or a demand loan secured by an FD, the FD continues to earn the interest; the bank holds a lien and places interest on the loan itself. Always make sure that there are no administrative charges.

Reference:

1. SBI, accessed from: https://sbi.co.in/web/yono/loan-against-fixed-deposit

2. SBI, accessed from: https://sbi.co.in/web/personal-banking/loans/loans-against-securities/loan-against-time-deposit

3. SBI, accessed from: https://sbi.co.in/web/yono/loan-against-fixed-deposit

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001