Monthly Income Scheme: Best Options For Regular Passive Income In India

Creating a passive income source is one of the most common ideas people have when they start investing. However, most struggle in finding such investments that can give monthly returns. This is what monthly income schemes are for.

If you do not know much about them, read on till the end. In this blog, we will discuss what they are and some of the types of such schemes available in India.

What Is A Monthly Income Scheme?

A Monthly Income Scheme (MIS) is an investment option that helps you earn a fixed and regular income every month. Instead of waiting until maturity, you receive interest payouts monthly while your principal remains invested. These schemes are commonly offered by the Post Office, banks, and mutual funds, making them ideal if you want a predictable cash flow and financial stability.

How does it work?

A Monthly Income Scheme allows you to invest a lump sum amount and receive interest payouts every month at a pre-defined rate. Here is how it works:

- You invest a fixed amount in a scheme offered by a bank, Post Office, or mutual fund.

- The institution calculates interest based on the applicable rate and your invested amount.

- The earned interest is paid to you monthly, providing a steady income stream.

- Your principal amount remains locked for a specific tenure, depending on the scheme.

- At maturity, you receive your original investment amount back.

Who should invest?

A Monthly Income Scheme is suitable if you want a consistent income with relatively lower risk. You should consider investing if you are:

- A retiree looking for a regular income to cover monthly expenses

- Someone seeking stable returns without actively managing investments

- A conservative investor who prioritises capital safety over high returns

- An individual planning passive income to supplement salary or other earnings

- Anyone looking to diversify their portfolio with predictable income-generating investments

Types Of Monthly Income Schemes In India

You can choose from several monthly income plans in India based on your risk tolerance, income needs, and investment goals. These options range from government-backed schemes offering fixed income to market-linked instruments that may provide higher returns with some risk.

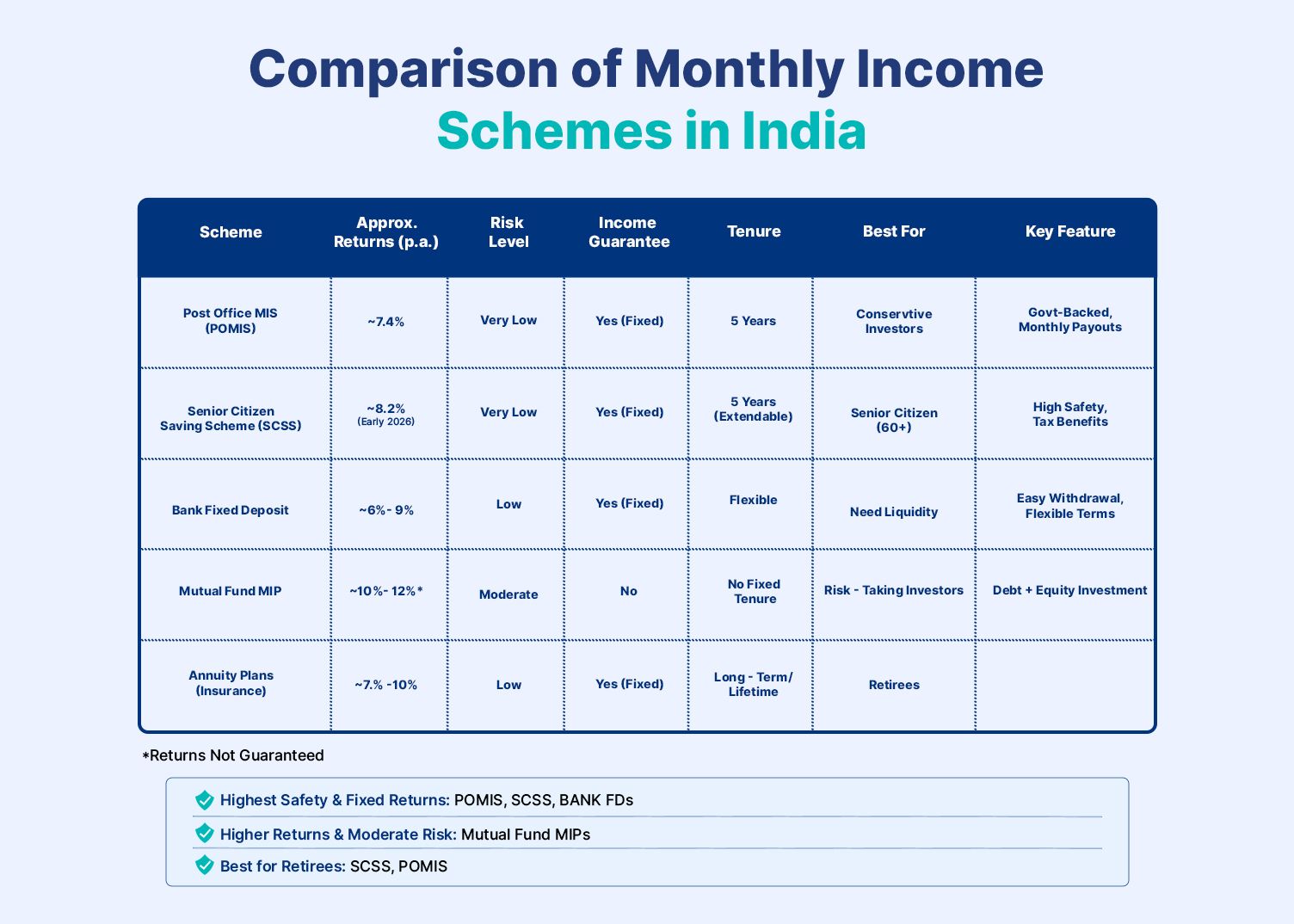

1. Post Office MIS (POMIS)

Post Office MIS is a government-backed scheme that provides a fixed monthly income with high safety. You invest a lump sum and earn 7.4% annual interest, paid monthly, for a 5-year tenure. Your principal is returned at maturity, making it suitable if you want a stable and predictable income.

2. Monthly income mutual funds

Monthly income mutual funds invest mainly in debt securities like bonds and money market instruments to generate regular income. Returns are not guaranteed and depend on market performance. These funds offer higher return potential than fixed schemes and are suitable if you can accept moderate risk for better income.

3. Senior citizen schemes

SCSS is a government-backed scheme designed to provide a regular income after retirement. It offers 8.2% annual interest, paid quarterly, with strong capital protection. The scheme has a 5-year tenure and is suitable if you are a senior citizen seeking a secure and reliable income.

4. Corporate bond monthly payout options

Corporate bonds provide regular income by paying interest to investors, sometimes monthly, depending on the bond structure. Platforms like Grip Invest and Navi Finserv offer such opportunities. These investments can offer higher returns than traditional schemes but involve moderate risk based on issuer credibility.

Returns And Risk Comparison

To make a well-calculated decision for which MIS to choose, go through the table shared below.

Tax Implications

Most monthly income plans in India are taxable. The monthly income or the interest that you earn is added to your total income and taxed according to the Income Tax slab under ‘Income from other Sources.’

Post Office MIS (POMIS)

- Interest earned is fully taxable as per your income tax slab.

- There is no TDS deduction, but you must report the income in your ITR.

- The investment amount does not qualify for the Section 80C deduction.

Monthly Income Mutual Funds

- Income received through IDCW payouts is taxed as per your slab rate.

- Capital gains from redemption are also taxed as per applicable debt or equity taxation rules.

- TDS may apply depending on the payout amount and investor category.

Senior Citizen Savings Scheme (SCSS)

- Interest income is taxable as per your slab rate.

- TDS applies if the annual interest exceeds INR 50,000.

- Your investment qualifies for a tax deduction under Section 80C up to INR 1.5 lakh.

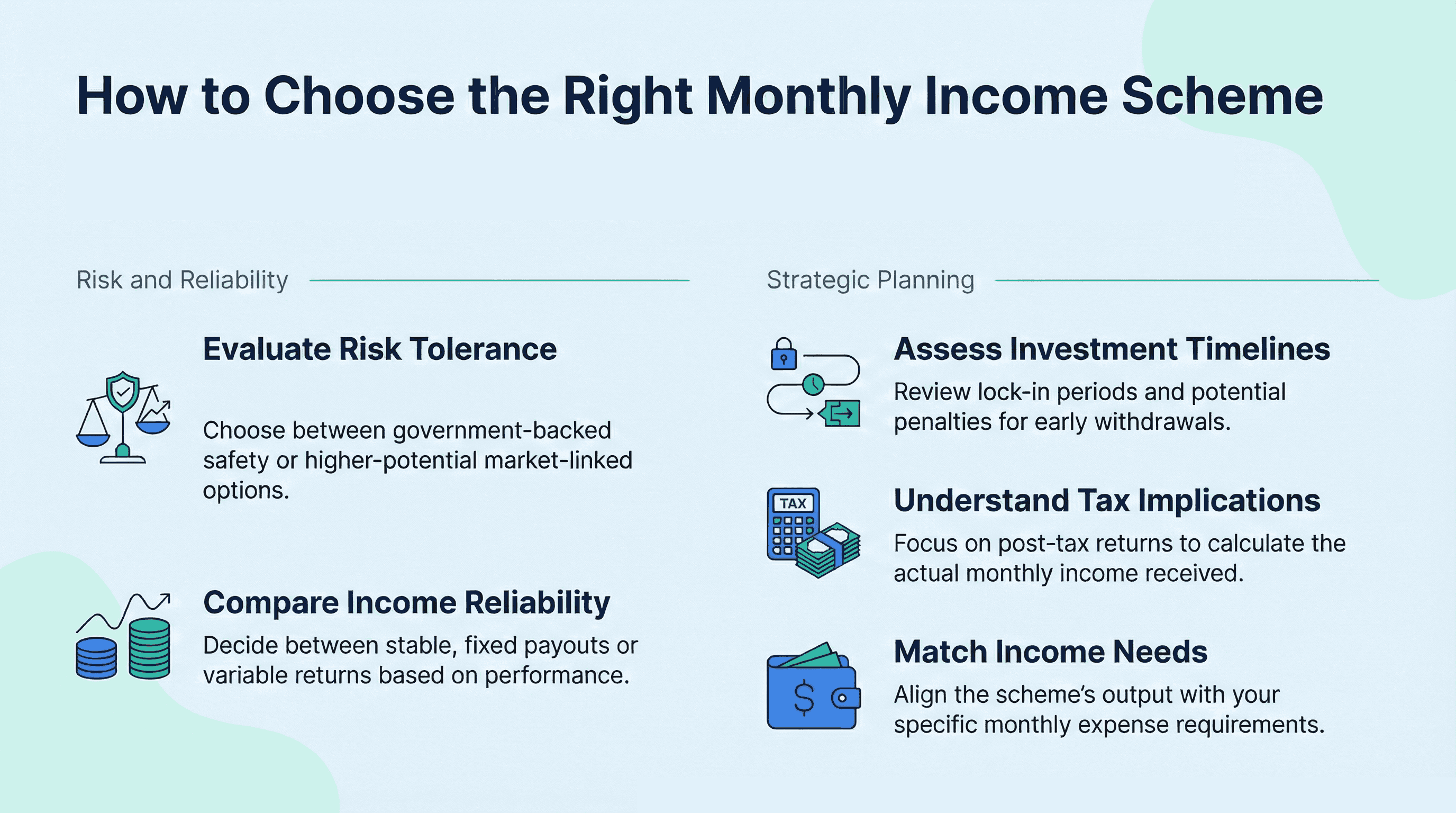

How To Choose The Right Scheme?

Selecting the right monthly income scheme depends on your income needs, financial goals, and risk tolerance. You should evaluate key factors carefully to ensure the scheme provides a stable income while protecting your capital.

1. Evaluate Your Risk Tolerance

You should start by deciding whether you want complete safety or are open to taking some risk for higher returns. If you want guaranteed income and capital protection, government-backed schemes are a better fit. If you are comfortable with some uncertainty, market-linked options like mutual funds or corporate bonds may offer better income potential.

2. Compare Income Reliability

Some schemes offer fixed monthly income, while others provide variable payouts depending on performance. You should choose between a stable and predictable income or a slightly higher income that may fluctuate. This decision depends on whether consistency or higher returns matter more to you.

3. Assess the Investment Timeline

Every scheme has a fixed tenure or lock-in period. You should make sure you are comfortable keeping your money invested for that duration. Also, check if early withdrawal is allowed and whether there are any penalties involved.

4. Understand Tax Implications

The income you receive is usually taxable, which reduces your actual earnings. You should always consider post-tax returns to understand how much income you will actually receive every month.

5. Match the Scheme to Your Income Needs

You should calculate how much you need every month and invest accordingly. This helps you select a scheme that can generate enough income to support your expenses without putting your financial security at risk.

Conclusion

Starting to invest in monthly income schemes can play a crucial role in moving towards financial independence. However, to ensure so, it is essential that you choose the best monthly income scheme per your risk appetite and investment goals.

To effortlessly start earning monthly payouts from your investments, consider signing up with Grip Invest. It is an intuitive alternative investment platform that facilitates you to invest in avenues like corporate bonds and SDIs. In fact, they have enabled investments worth over INR 3,000 crores.

FAQs

1. Is the Monthly Income Scheme safe?

Yes, monthly income schemes can be safe, depending on the type you choose. Government-backed options like Post Office MIS and SCSS offer high safety and stable income, while mutual funds and corporate bonds carry some risk but may provide higher returns.

2. Which Income Plan gives the highest return?

Corporate bond monthly payout options and market-linked income funds usually offer the highest returns, typically around 8% to 12% per annum, depending on risk and issuer quality. In comparison, government schemes like Post Office MIS offer around 7.4% annually, with lower risk but more stable income.

3. Is MIS taxable?

Yes, income from a Monthly Income Scheme (MIS) is fully taxable. The interest you receive is added to your total income and taxed as per your income tax slab. There is usually no TDS in Post Office MIS, but you must report it in your ITR.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001