Portfolio Turnover Ratio: Hidden Costs and Why Investors Should Care

The one thing investors are focused on is returns; they ignore the costs hidden in your Portfolio Turnover Ratio, also known as PTR. The reason for being attentive about these ratios is that they affect transaction costs, final investor return, and tax liability.

For example, let’s say two funds are delivering 12% gross returns. These could give very different net returns once we consider costs and taxes. Knowing PTR is as essential as knowing the differences between a credit score and a CIBIL score. They both seem similar, but have a lot of differences that affect financial returns.

In this blog, we will discuss the meaning of a portfolio and turnover. Moreover, we will talk about its effects on your wealth creation in mutual funds and why it is important

What Is Portfolio Turnover Ratio?

By definition, PTR is the percentage of fund holdings that have been replaced annually. It tells us how actively a fund manager buys or sells securities within the portfolio.

You can calculate your PTR with the following formula:

PTR = Lesser of Total Purchase (or Total Sales)/ Average Assets Under Management (or AUM) x 100

Let's take an example:

A mutual fund has an AUM of INR 100 crore in a year. The fund manager buys 30 crore securities and simultaneously sells securities worth 20 crores. This shows a lesser purchase of securities, and so the PTR calculated will come up to 20%. This means that 20% of the portfolio was churned during the year.

In other words, PTR checks a vehicle's engine activity. Higher revs will give you speed but will cost you more fuel, whereas low revs keep the ride smoother but will take you slower.

High vs Low Turnover Ratio

Now let's discuss in detail what the meaning of having a high vs a low turnover is:

1. High Turnover:

A high turnover signifies that a manager buys and sells securities very often, which can be multiple times within a year.

Pros

- Permits the manager to benefit from short-term market opportunities.

- High turnover reduces exposure to underperforming assets.

- In volatile markets, some turnovers might generate a larger gross return.

Cons

- High turnover suggests higher transaction costs.

- May lead to risk and volatility.

Example: A fund manager churns 100% of a portfolio worth 100 crore, in which trading with tax costs amounts to 2 crore(2%) from the investor's wealth, annually.

2. Low Turnover

A low turnover suggests that the fund manager has resorted to the buy-and-hold strategy. This is caused by fewer trades.

Pros

- It minimizes short-term taxes, which means it's more tax efficient..

- Fewer transactions offer stability and predictability in returns.

- Suitable for investors who want to create long-term wealth.

Cons

- Investors may lose out on short-term opportunities.

- It has a chance of not performing well in fast-moving, volatile markets.

Why Should Investors Care?

Most investors overlook the fact that costs and taxes directly impact their finances; they tend to focus more on the returns. This is where PTR helps; it influences both and is crucial to evaluate before making investments.

Effect on Expense Ratio and After-Tax Returns

With a higher turnover, there is an increase in higher trading costs, which are then added to the expense ratio. Short-term capital gains can be obtained with frequent buying and selling, with an equity of 15% compared to 10% in the case of long-term gains.

The US mutual funds show frequent trading worldwide, resulting in a 63% turnover ratio1.

Ideal Turnover Ratios For Different Categories

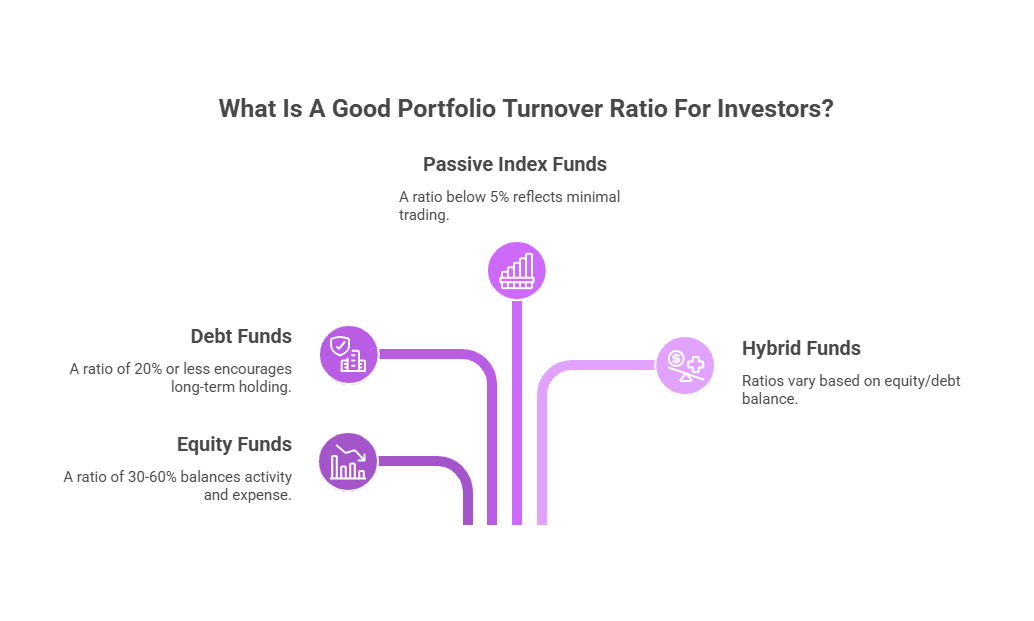

There are four different categories with their turnover ratios based on the portfolio nature and investment benefits-

- Equity Funds: Portfolios that are heavy on company stocks must have a healthy ratio of 30-60%. Having a higher ratio incurs more expense, whereas a lower ratio means passive behavior in the active funds

- Debt Funds: .Fixed- securities like government bonds, treasury bills, debentures, or a mix of those should ideally have a turnover ratio of 20% or less. The yield rate does not fluctuate a lot like shares, so holding onto it for a longer period is the ideal option.

- Passive Index Funds: Portfolios based on established indices like Nifty or Sensex50 are usually not bought or sold actively. A healthy ratio will be lower than 5%

- Hybrid Funds: Hybrid portfolios are tricky. Based on the investor's attitude, i.e., equity-heavy or debt-heavy, a balance is necessary. An aggressive hybrid (equity) would call for 30-50% turnover. A conservative hybrid (debt) would have <20% turnover.

Role Of Passive And Fixed Income Investments

Investors who prefer stability, lower risks, and long-term wealth building create their portfolio around fixed-income investments. This means they have considerably lower hidden costs and a more predictable growth projection over the years.

Passive Funds And Bonds With Low Turnover = Stability

Passive funds and fixed-income investments are attractive to conservative investors who prefer capital protection with modest returns and do not have to worry about active management risk. This buy-and-hold strategy makes trading a smooth experience compared to high-risk share trading. In addition, maintaining the turnover rate (<20%) is equally important for such portfolios, which would otherwise drive away the low-cost benefits.

Conclusion

High-turnover portfolios may offer quick gains but come with higher costs and taxes, while low-turnover ones focus on long-term efficiency and compounding. The right choice depends on your goals and risk appetite. To make that decision simpler, platforms like Grip Invest give you access to diversified options—from corporate bonds to SDIs, starting at just INR 1,000, helping you build a portfolio that matches your wealth journey.

FAQs On Portfolio Turnover Ratio

1. What is considered a good turnover ratio?

For short holding periods like equity, the ratio is higher (around 30-60%). For debt securities like bonds, which generally have longer hold periods, the turnover ratio is much lower (<20%).

2. Is high portfolio turnover always bad?

No. Having a high portfolio is not considered ‘bad’ in the traditional sense. It depends on the investor's attitude. Such portfolios are considered more volatile and are best avoided by investors who prefer stability.

3. How does turnover affect taxation?

Tax is levied whenever the fund manager sells your assets. Having a higher portfolio turnover translates to frequent transactions in the same time period compared to low portfolio turnover. Each time revenue is gained from these transactions, it gets taxed.

4. Which types of funds have low turnover?

Debt-based turnover has a long hold period and low turnover. Such assets are not sold frequently because of their lock-in periods, which results in a healthy ratio of 20% or less.

References:

1. Morning Star, accessed from: https://www.morningstar.com/articles/1136410/what-is-portfolio-turnover

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks, including delay and/ or default in payment. Read all the offer-related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for the consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001