Premature FD Withdrawal Penalty: How Much Do You Really Lose?

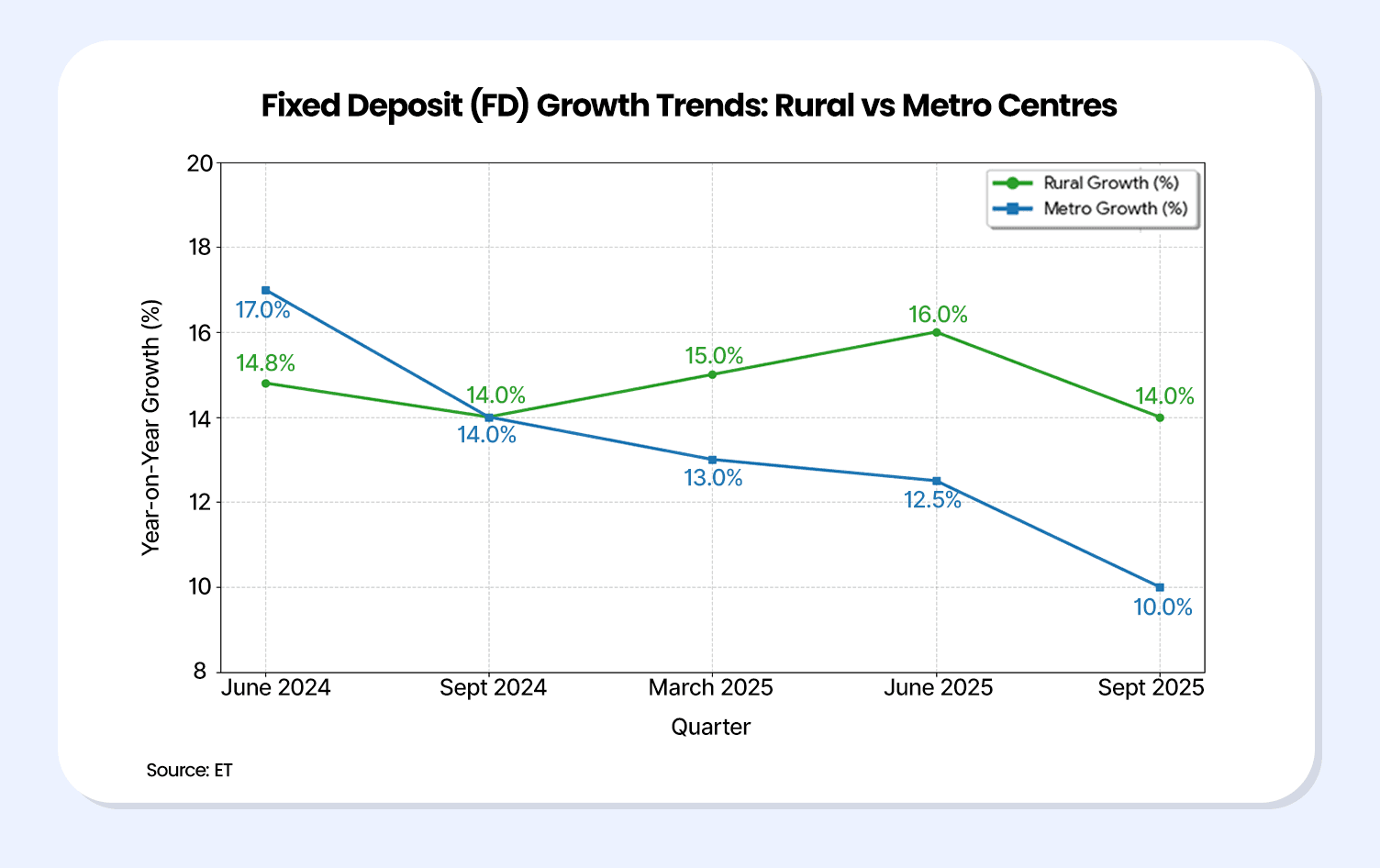

Fixed deposits have always been a popular choice among Indians, specifically among conservative investors. Even in the September quarter of 2025, the fixed deposit balance in rural areas jumped 14% year-on-year to hit INR 9.7 lakh crore, while in urban areas, the rise was 10% to reach INR 86 lakh crore. The graph below shows the growth of FDs in India, especially in rural areas, despite periodic fluctuations1.

The primary cause of this popularity is the notion of predictable returns, low risk, etc., that investors have with FDs. However, when investors break a fixed deposit early, most of these notions crumble. In such a scenario, the importance of flexibility and liquidity becomes acute, as investors realise that FD returns can be fixed but might not be predictable.

Therefore, in this blog, we will decode the premature FD withdrawal penalty and understand what happens if we try liquidating before maturity, so that investments can be planned effectively.

What Is Premature FD Withdrawal?

Before getting into the FD penalty charges for premature withdrawal, let us understand the nuances of it.

If a fixed deposit investor withdraws his FD funds, partially or fully, before the maturity date, it is called a premature withdrawal of a fixed deposit.

For instance, if Mr K invested INR 10 lakhs at 6.5% for 10 years in an FD but withdrew it after 5 years, it is considered a premature withdrawal. Let us discuss some FD withdrawal rules and features in India to understand the concept better.

FD Withdrawal Rules India

Listed below are the features of a fixed deposit withdrawal that investors must know.

1. Bank FD Penalty: When investors withdraw FDs before maturity, they have to pay a fine and lose a portion of the interest accrued. The interest deduction is calculated based on the tenure for which the FD was made and the tenure it was actually held.

2. Minimum Period: Most fixed deposits have a particular tenure during which withdrawal is not allowed. For instance, XYZ bank might not allow withdrawals for 7 days from the date of creation on FDs less than INR 1,00,000.

3. Partial Withdrawal: Banks often allow partial withdrawals, that is, withdrawal of a set amount and not the entire FD. For instance, if Mr K withdraws INR 10,000 out of his INR 2 lakh FD, the remaining INR 1.90 lakh will continue as a FD, post withdrawal. This helps reduce the penalty and limit capital erosion.

Now, with this understanding of FD withdrawals, let us explore the premature FD withdrawal penalty.

How Banks Calculate Premature FD Withdrawal Penalty

As previously discussed, two types of premature FD closure charges are levied when an investor decides to break an FD before its maturity. Each of them is discussed below.

- Penalty or Fine: Banks charge a basic penalty or fine at a flat rate. Although the penalty rate can vary, typically it ranges from 0.5% to 1%, based on the unique policy of the bank or non-banking finance company (NBFC) in question.

- FD Interest Loss: Banks have varying interest rates, which differ based on the FD tenure and amount. When FD is broken prematurely, the interest accrued is either recalculated based on a lower interest rate (if the rate on tenure for which the FD is actually held is lower than the booked rate) or maintained at the same rate (if the rate on tenure for which the FD is actually held is equal to or greater than the booked rate).

Now, let us look at two cases of premature FD withdrawals to understand the premature FD withdrawal penalty in detail.

| Case 1: Mr K invested INR 1,00,000 at 7.5% interest for 3 years, but he withdrew the entire FD prematurely after 2 years. The rate of return on a 2-year FD is 7%, while a penalty is charged at 1%. | |

| A. Principal | INR 1,00,000 |

| B. Booked interest rate (3-year FD) | 7.5% |

| Maturity amount if not withdrawn | INR 1,24,972 |

| C. Interest rate on 2-year FD | 7% |

| D. Penalty | 1% |

| E. Effective interest (C-D) | 6% |

| Maturity amount post withdrawal | INR 1,12,649 |

| Case 2: Other factors remaining constant, if 2-year and 3-year interest rates were 6.5% and 6%, respectively. | |

| A. Principal | INR 1,00,000 |

| B. Booked interest rate (3-year FD) | 6% |

| Maturity amount if not withdrawn | INR 1,19,562 |

| C. Interest rate on 2-year FD | 6.5% |

| D. Penalty | 1% |

| E. Effective interest (B-D) | 5% |

| Maturity amount post withdrawal | INR 1,10,449 |

While interest loss is a key concern with premature FD withdrawal, the penalty interest might seem minimal, but it requires attention because it differs from bank to bank.

Penalty Differences Across Banks

When choosing a bank to make a fixed deposit, investors should take the Bank FD Penalty for premature withdrawal into consideration as well. This can aid in choosing one with an optimal penalty structure and reduce loss in case of withdrawal before maturity. The table here highlights the penalty rates at some banks as of 21 January 2026.

| Bank | Penalty | Exceptions |

| SBI2 | For deposits up to INR 5 lakh penalty is 0.50%. For deposits above INR 5 lakhs penalty is 1%. | No interest paid for less than 7 days deposit |

| HDFC3 | 1% | Penalty is not applicable for single deposits that are:

|

| ICICI Bank4 | Penalty is 0.50% for less than 1-year deposits and 1% for 1-year to less than 5-year deposits. If the deposit is 5 years or above, the penalty can vary from 1.00% to 1.5% for deposits below INR 5 crore, and remains constant at 1.5% for deposits of INR 5 crores and above. | |

| PNB5 | 1% |

However, not just penalty and interest loss, investors should also consider the taxation impact of premature withdrawals.

Tax Impact Of Breaking An FD Early

Although the tax rates applicable to an FD remain the same during premature closures, different aspects of taxability must be analysed before choosing premature withdrawal.

- Tax Planning: In case of premature withdrawal, tax remains payable on the investment. Therefore, the tax payable can become due earlier than anticipated and hinder the tax plan.

- Readjustment of TDS: The bank or NBFC reevaluates the TDS to match the lower interest earned post the premature FD withdrawal penalty.

- Tax-Saving FDs: In case of tax-saving FDs, premature withdrawals are restricted due to a 5-year lock-in6.

Therefore, investors should optimise their portfolio and FD investments with better FD liquidity options and alternatives.

Smarter Alternatives To Avoid FD Penalties

Investors can aim to balance their portfolio with liquid and short-term emergency fund investments to avoid premature FD withdrawals and penalties. Discussed below are some options.

- Short-Term FDs: Rather than investing the entire prospective FD allocation in one long-term FD, investors can diversify the fund across FDs of different tenures, including short-term FDs (3-12 months or less). This can help balance liquidity while optimising yield.

- Liquid Funds: Different types of liquid funds, including short-duration and ultra-short-duration funds, mature fast because of the investment in short-term assets like T-bills. As of 20 January 2026, the category average performance of short-duration fixed-income funds were 7.08%7.

- Debt Assets: Short-term debt assets, like bonds in secondary market with early maturity, can offer a blend of liquidity, low risk, and predictable returns. Grip offers corporate bonds with up to 12.5% YTM.

Conclusion

While fixed deposits are widely perceived as safe and predictable, premature withdrawal can materially reduce returns through interest recalculation, penalties, and tax timing mismatches. Understanding how premature FD withdrawal penalties are calculated, how interest rates are reset, and how different banks apply charges is essential before committing funds for long tenures.

For investors who may need liquidity, breaking an FD early can disrupt cash flow planning and erode the very stability FDs are meant to provide.

A more balanced approach involves planning FD investments across staggered tenures, maintaining adequate liquid assets, and complementing traditional FDs with instruments that offer better liquidity and predictable cash flows. Evaluating alternatives before locking funds can help avoid unnecessary penalties while keeping financial goals on track.

Platforms like Grip Invest allow investors to explore corporate FDs and corporate bonds with defined maturities, helping improve liquidity management and reduce the risk of premature withdrawals while planning fixed-income investments more effectively.

FAQs On Premature FD Withdrawal Penalty

1. How much penalty is charged for premature FD withdrawal in India?

Most banks charge a penalty between 0.5% and 1% on the applicable interest rate, but the exact charge depends on the bank, FD amount, and remaining tenure.

2. Do I lose all interest if I break an FD early?

No, but the interest is usually recalculated at a lower rate applicable to the actual holding period, and then the penalty is deducted, which reduces overall returns.

3. Is premature withdrawal allowed in tax-saving fixed deposits?

No. Tax-saving FDs come with a mandatory 5-year lock-in period, and premature withdrawal is not permitted under income tax rules.

References:

1. Economic times, accessed from: https://economictimes.indiatimes.com/industry/banking/finance/banking/fixed-deposit-growth-finds-its-key-driver-in-rural-incomes/articleshow/125897315.cms?from=mdr

2. SBI, accessed from: https://sbi.bank.in/web/business/sme/sme-fixed-deposits/term-deposits

3. HDFC, accessed from: https://v.hdfcbank.com/htdocs/common/Netbanking_Note/Liquidate_Fixed_Deposit.html

4. ICICI, accessed from: https://www.icicidirect.com/ilearn/personal-finance/articles/premature-fd-withdrawal-charges

5. PnB, accessed from: https://pnb.bank.in/pre-mature-cancel.html

6. Income tax, accessed from: https://tinyurl.com/mrhjxj2b

7. Morning star, accessed from: https://www.morningstar.in/tools/mutual-fund-category-performance.aspx

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001