Return On Equity Explained: How Investors Measure Profitability

When choosing which companies to invest in, assessing profitability is a key factor. However, the reported profit rarely indicates whether the company utilises its funds efficiently. This is where Return on Equity (ROE) comes in.

This financial metric cuts through the balance sheet complexities and delivers a concise indication of whether the company is genuinely creating value for its shareholders.

Ideally, every rupee invested by the shareholder in the business should generate returns that justify the risks borne. Profitability ratios like return on equity help benchmark this performance, such that it can be compared with other companies operating in the same sector.

Such a comparative analysis of the same sector companies through ROE helps identify not only the high performers but also the bottom performers that might have revenue growth, but the value generated might be insufficient.

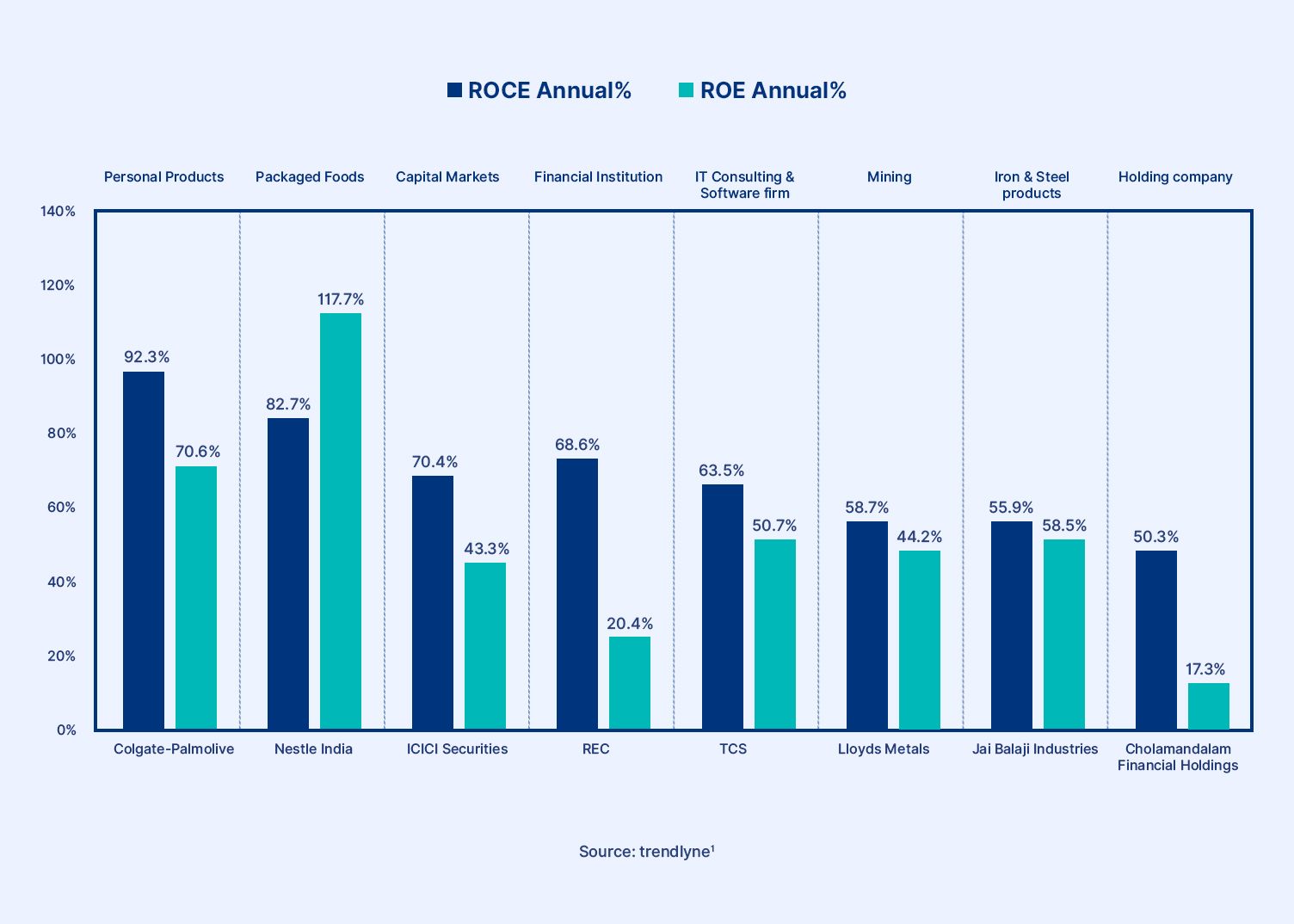

For example, the graph below illustrates how ROE varies across different sectors, along with companies that exceed the standard return on equity of their industry in FY24.

Roe Varies Across Different Sectors

Companies that consistently outperform their industry ROE offer better compounded wealth over the long term. Therefore, to understand the ROE meaning and use it to identify sectors and companies that can generate higher value for investors, this blog is a must-read.

What Is Return On Equity

Commonly abbreviated as ROE, return on equity refers to a fiscal performance metric that measures the net income reported by the company relative to the shareholder equity recorded in accounting statements. Simply put, ROE indicates the amount of profit a company earns for every rupee of equity capital invested by the shareholders.

Therefore, the measure of return on equity stems from two components, namely, net income and shareholders’ equity. Net income indicates the profit of the business after deducting all related costs, including depreciation, taxes, amortisation, interests, and so on.

On the other hand, shareholders’ equity represents the residual interest in the assets of the company after deducting all liabilities. Also known as net worth, the shareholders’ equity refers to the remainder of profit, left after all accrued debts of the company are met.

Return on equity can either be represented as a ratio or as a percentage. Multiplying the return on equity ratio by 100 gives the percentage form. Listed below are the ROE formulas.

Return on Equity Ratio = Net Income / Shareholders' Equity Return on Equity (ROE) = (Net Income / Shareholders' Equity) × 100 |

For example, if company A earns a net income of INR 16,00,000, while its shareholder equity is INR 8,00,000, its return on equity ratio will be 1:4, while return on equity in percentage terms would be 25%.

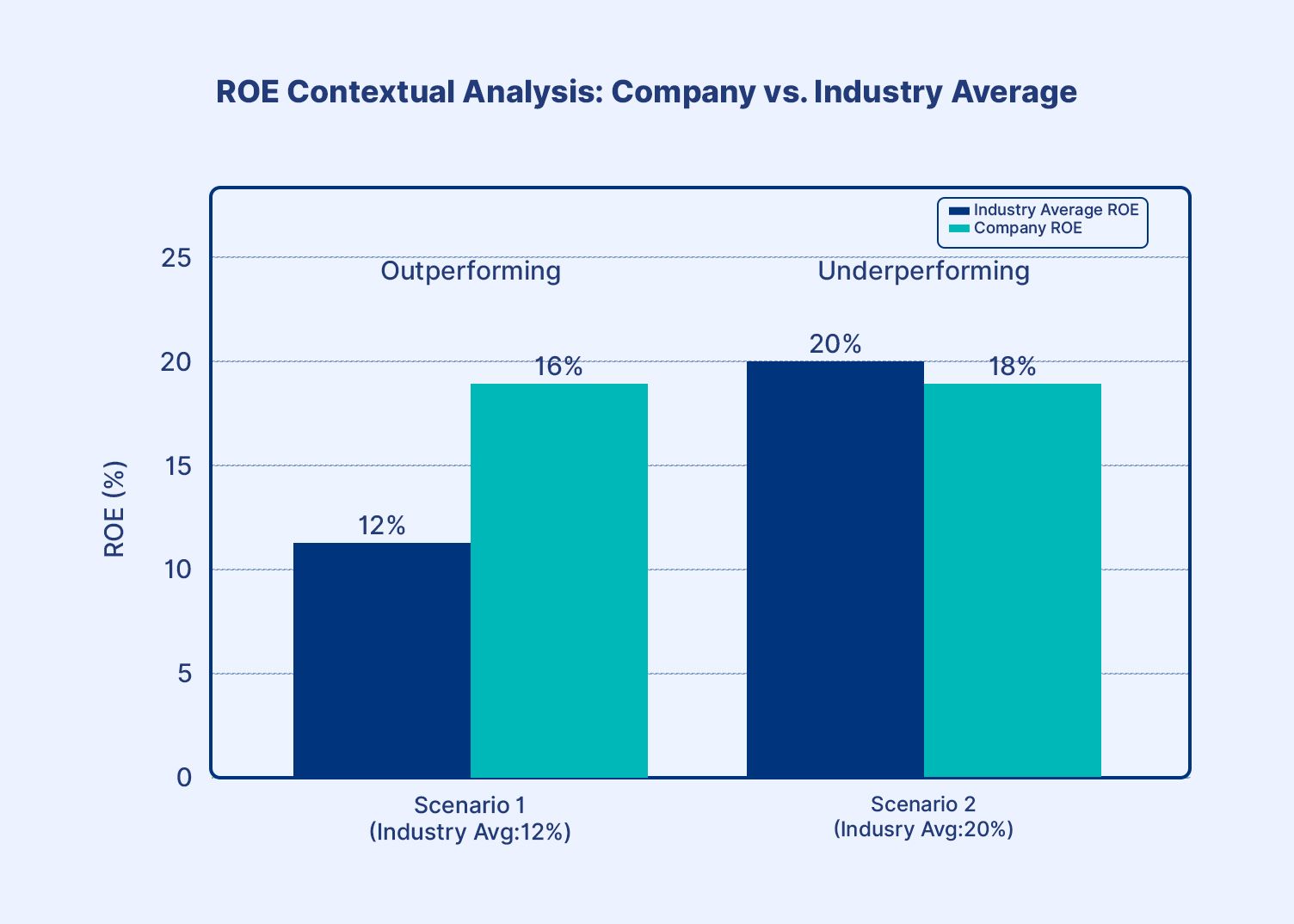

The ROE meaning becomes more nuanced when viewed in context. For instance, if a particular industry has an average ROE of 12%, and a company operating in that industry reports an 18% ROE, it might be considered a good sign, as the company has fared better than its peers or the industry.

However, had the ROE of the industry been 20%, the company's ROE would have indicated underperformance.

Therefore, the purpose of ROE is not served fully until an investor can interpret its meaning optimally.

How Investors Interpret ROE

Implementing the use of metrics like ROE to judge the investability of a company's stocks requires the investor to have optimal knowledge of how to interpret this ratio. Unlike many metrics, ROE has a contextual meaning, as elaborated before. This means ROE is low or high relative to a benchmark. This section explains what a high and a low return on equity imply.

| Particulars | High Return on Equity | Low Return on Equity |

| Meaning | The return on equity recorded by the company in question is higher than the industry average or its peers. | The return on equity recorded by the company in question is lower than the industry average or its peers. |

| Efficient Profitability | A high ROE not only implies that the company is profitable, but it also indicates that the shareholders can expect greater value than the average peers of the industry on their capital investment. | Even if a company records a profit, a low ROE implies that the company is inefficient in generating sufficient profit, which aligns with the capital shareholder’s invest, given a particular risk. |

| Management | The management team of the high ROE company might be able to identify profitable projects and optimally allocate the capital raised. | A low ROE company might have inefficient management that is unable to optimally allocate resources. The capital of the shareholders is inefficiently utilised. |

| Asset Model | Industries like technology often require less physical capital to generate revenue, resulting in a greater ROE. | Capital-intensive industries like manufacturing often require high physical capital to generate revenue, resulting in lower ROE. |

| Business Phase | Established businesses with efficient management often have a greater ROE. | Start-ups investing heavily in growth may have low ROE in early years. |

| Dilution | Well-planned equity issuance results in capital intake, which is required by the company. This avoids inefficient or underutilisation of capital. As the denomination (Shareholders’ Equity) is controlled, the ROE is high. | Raising more capital than what is required by the company creates the opportunity for underutilisation. With a higher-than-required denominator, the ROE falls. This dilutes the equity base and can artificially suppress profitability. |

However, despite these nuanced perspectives that the ROE provides on a company and its profitability, there are certain limitations to its use.

Limitations Of ROE

Although return on equity is an efficient tool to judge a company's profit optimally, it still has certain limitations. These hurdles are explained below in detail.

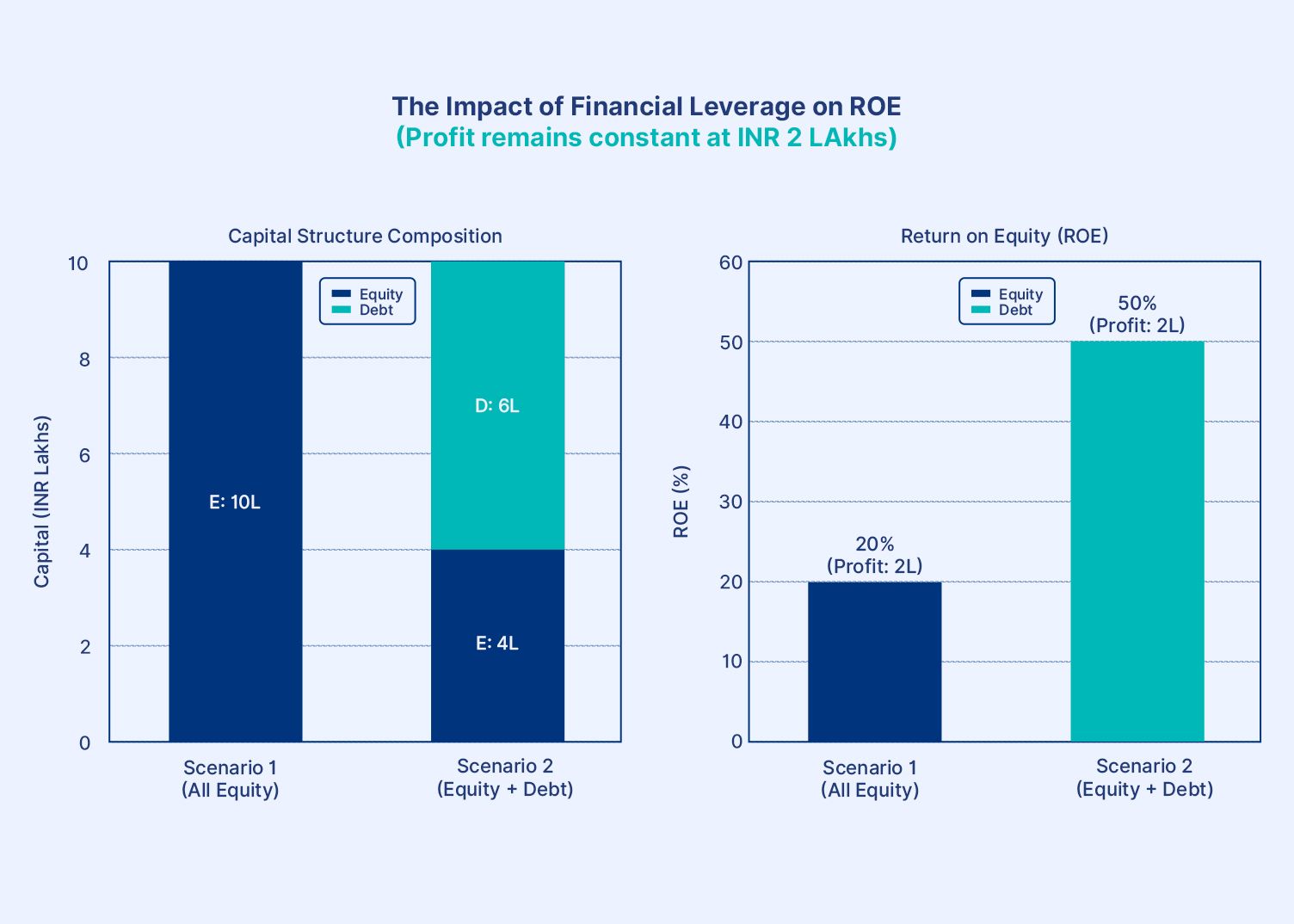

1. Impact of high debt: Imagine a company that does not utilise the capital it raised efficiently, resulting in a lower profit than expected, but rather than raising capital through equity, it primarily raises funds through debt. Since ROE uses shareholders’ equity and not the total capital in its denominator, a company that replaces equity with debt for capital effectively shrinks its equity base, resulting in a lower ROE, despite having no change in profit efficiency.

For example, suppose Company A made a net profit of INR 2 lakhs with INR 10 lakhs of equity capital. Its ROE would be 20%. Now, imagine the net profit remains the same, and the company still raised INR 10 lakhs. However, this time it raises INR 4 lakhs from equity and INR 6 lakhs from debt. In this scenario, its return on equity ratio would be 50%. Notice how ROE increased from 20% to 50%, without an improvement in profit, but due to replacing equity with debt.

2. Accounting adjustments: Return on equity might be impacted by accounting choices that are completely legal, like share buyback, depreciation policy, revenue recognition, etc. For example, when a company buybacks its shares, the shareholders’ equity reduces, resulting in a rise in equity, without any actual change in profit. Therefore, the ROE meaning must be interpreted after reading the notes to accounts as well, which explains how the ROE is calculated.

3. Sporadic Gains and Losses: A company can record sudden profit hikes or slumps for factors that are unique, unusual to its operations, and out of its control. For example, in this ongoing Iran-US and Israel War, certain companies might have an impact on profit, resulting in lower ROE. However, this is not a common occurrence. Therefore, while interpreting ROE data, investors must not rely on data of a single year; optimal analysis of consecutive financial years helps understand the ROE trend and ignore occasional spikes or dips.

There are several other aspects of how ROE is implemented by experienced investors to judge profitability efficiently.

How Investors Use ROE In Stock Analysis

Return on equity is a highly efficient financial metric that investors often use to judge the profitability of a company. However, it must be used efficiently, keeping certain aspects in mind, for a holistic analysis.

1. Notes to Accounts: While referring to an ROE, an investor must refer to the notes to accounts to avoid limitations caused by accounting adjustments and debt-intensive capital structure.

2. Track ROE over Multiple Years: Analysing only one year’s ROE can result in a distorted analysis due to the impact of sporadic or unusual events. Analysing recurring ROE records of consecutive years helps gauge profit patterns and weed out exceptions.

3. Same Industry Comparison: Different industries have different ROE, as explained before. Therefore, when comparing the ROE of companies, investors must ensure that they belong in the same industry.

4. Combining ROE with Other Ratios: Different ratios analyse different aspects of the business, while some judge profitability, others might judge liquidity or capital structure, and so on. As no single ratio shows the complete picture, investors must use different ratios and metrics together for a holistic analysis.

For example, a high ROE, paired with a consistently growing Earnings Per Share (EPS), indicates compounding shareholder wealth.

However, successful investing requires optimal portfolio planning as well. Despite strong equity allocation with optimal analysis of financial ratios, over-reliance on equity can increase risk beyond investor appetite. Therefore, diversification across fixed-income securities, along with debt, is necessary for stable growth.

Grip houses a range of financial assets, like high-yield FDs and corporate bonds, that can offer up to 12.5% YTM. Visit Grip Invest Today!

FAQs On Return On Equity

1. What is return on equity?

Return on equity (ROE) is a financial ratio that measures the net profit a company generates relative to its shareholders' equity. When net income is divided by shareholders’ equity, we get the return on equity ratio.

2. What is a good ROE ratio?

There is no single universally 'good' ROE, as the benchmark varies by sector. If the ROE of a company is better than the industry average, it is considered good. On the other hand, a company's ROE, which is lower than the industry and peers, indicates a poor ROE.

3 Why do investors track ROE?

Investors track return on equity because it directly measures whether a company is creating value for shareholders. It indicates whether the company can utilise its resources, specifically funds raised with equity capital, efficiently to generate sufficient profit.

Reference:

1. trendlyne, accessed from: https://trendlyne.com/posts/4588927/chart-of-the-week-companies-that-outperformed-their-industry-this-year-in-roce-and-roe

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001