The Power Of Rupee Cost Averaging In Mutual Fund Investments

Introduction

Investing in mutual funds is a popular way to build wealth over time. For many people, dealing with the ups and downs of the market can be difficult, especially when trying to figure out the best time to invest. Rupee Cost Averaging (RCA) offers an easy and effective way to handle these challenges by investing a fixed amount regularly, regardless of market ups and downs.

This approach allows investors to buy more units when prices are low and fewer when prices are high, lowering the average cost of their investment and minimizing the risks of trying to time the market. RCA is often implemented through Systematic Investment Plans (SIPs), making systematic investing accessible to all.

Demystifying Rupee Cost Averaging: The Core Concept

Rupee Cost Averaging is the practice of investing a fixed sum of money regularly into a mutual fund. This strategy leverages the "Buy Low, Buy More" principle. Investors buy more units when the Net Asset Value (NAV) of the fund is low and fewer units when prices rise, thus averaging out the purchase cost over time.

By sticking to a regular investment schedule and ignoring market noise, investors avoid the stress and pitfalls of trying to time the market, allowing for steadier progress toward financial goals.

Illustrative Examples Of Rupee Cost Averaging

Scenario 1: Rising Market

Imagine an investor who puts INR 10,000 monthly into a mutual fund. In a rising market, where the NAV moves from INR 20 to INR 28 over six months, the investor buys fewer units as prices rise. Despite this, the total value of their investment increases steadily, reflecting the market’s upward trajectory.

Scenario 2: Falling Market

In a falling market, where the NAV decreases from INR 28 to INR 20, investing the same INR 10,000 each month allows you to buy more units at lower prices. This lowers your average cost per unit and sets you up to gain more when the market bounces back.

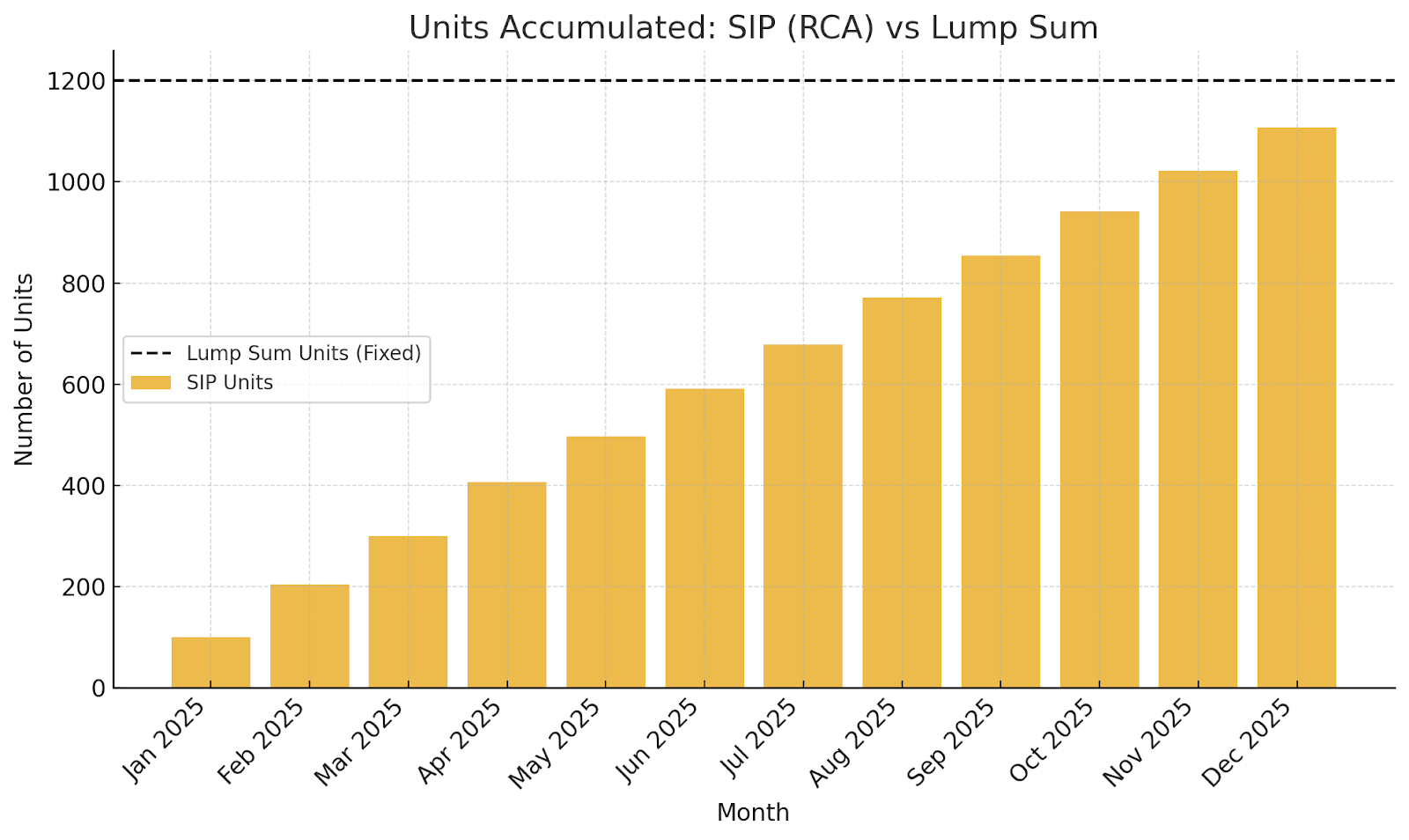

Let us understand this with this table:

| Month | Investment (INR ) | NAV (INR) | Units Purchased | Cumulative Units | Total Invested (INR) |

| 1 | 10,000 | 20 | 500.00 | 500.00 | 10,000 |

| 2 | 10,000 | 22 | 454.55 | 954.55 | 20,000 |

| 3 | 10,000 | 24 | 416.67 | 1,371.21 | 30,000 |

| 4 | 10,000 | 26 | 384.62 | 1,755.83 | 40,000 |

| 5 | 10,000 | 28 | 357.14 | 2,112.97 | 50,000 |

| 6 | 10,000 | 27 | 370.37 | 2,483.34 | 60,000 |

Benefits Of Rupee Cost Averaging With Real Facts

1. Mitigating Market Volatility

RCA dilutes the risk of investing a lump sum at an inopportune moment. SIP inflows in India touched a massive INR 28,464 crore in July 2025, showcasing investor preference for this market volatility-mitigating approach. By spreading investments, RCA reduces the impact of market fluctuations and protects the investor from large losses¹.

2. Fostering Investment Discipline

Regular investments via SIP cultivate a disciplined saving habit. Broad participation through SIPs—with assets crossing INR 1,09,000 crore in 2025-highlights how investors leverage RCA for steady wealth creation.

3. Taming Emotional Biases

Investors often face emotional challenges: panic during downturns or greed during upswings. RCA’s automated, fixed investment routine helps eliminate emotional decision-making, promoting steadiness and long-term thinking.

4. Achieving A Lower Average Cost (Data-backed)

Rupee Cost Averaging allows the investors to reduce their average cost per unit by purchasing more units when prices are low and fewer units when prices are high. In an example of clear tax paper, Priya invested INR 5,000 monthly in a volatile market over a year and accumulated 1,259 units at an average cost of INR 47.65 per unit, compared to 1,200 units at INR 50 per unit from a lump sum. This illustrates the real savings RCA can offer2.

5. Harnessing The Power of Compounding

Consistent investing over 15 years at an assumed 18% return can transform INR 9 lakh invested into nearly INR 46 lakh3. RCA allows investors to benefit from compounding by continually increasing their corpus and reinvesting returns without trying to time the market.

6. Accessibility And Affordability

SIPs, the common vehicle for RCA, allow investments from as little as INR 500 per month, making wealth-building accessible across income levels and encouraging participation from diverse investor profiles.

7. Peace Of Mind

With automatic monthly investments, investors freed from constant market watching reduce stress and maintain focus on longer-term goals, enhancing their financial journey4.

Rupee At An All-Time Low: Why RCA Matters More Than Ever Right Now

Here is a live example of why rupee cost averaging is such a powerful concept. In 2026, the Indian rupee fell to its all-time low of INR 95.23 against the US dollar, the worst fiscal year performance for the currency in over a decade.

For most investors, headlines like these trigger panic- should I stop my SIPs? Should I wait for the market to stabilise? This is exactly the kind of moment where rupee cost averaging does its best work.

When the rupee weakens, the prices of import-dependent sectors and certain asset classes fluctuate. Markets tend to get nervous. But if you are investing a fixed amount every month through a SIP, you are automatically buying more units when prices dip and fewer when they rise. The currency noise in the background does not change your investment discipline; it actually works in your favour.

Think of it this way: investors who paused their SIPs during the rupee's slide missed the opportunity to accumulate units at lower NAVs. Those who stayed consistent benefited from the eventual recovery. The rupee's all-time low of 2026 is not a reason to stop investing; it is a reason to trust the process of rupee cost averaging even more.

When RCA Shines Brightest: Market Conditions And Investment Horizons

1. Optimal Performance In Volatile And Bear Markets

RCA provides major benefits during market turbulence by allowing the accumulation of more units at depressed prices5. This was especially helpful during the time period of market downturn in the year of 2022, when investors using SIPs were able to buy at lower prices, while those who invested a lump sum faced big losses in the short term.

2. Consistent Growth In Bull Markets

Even when markets trend upward, RCA ensures steady investment, allowing investors to participate fully in growth while smoothing out entry costs. SIP investors have enjoyed 12–15% CAGR during recent bullish phases, illustrating RCA’s utility across market cycles.

3. The Long-Term Advantage

RCA’s true strength emerges over longer horizons. Over the 10+ years, disciplined investing reduces volatility impact, delivers robust returns, and supports compounding. Investors staying committed over decades typically build significantly larger wealth than those trying to time markets.

4. Effect Of Investment Horizon

Short-term investors (<3 years) may see less benefit due to market unpredictability. However, horizons of 7–10 years or more maximize averaging and compounding advantages, aligning well with common financial goals like retirement or children’s education6.

RCA Vs. Lump-Sum Investing: A Comparative Look

A lump sum invested at the ideal time can yield higher returns, but comes with increased risk if done at market peaks. RCA through SIP averages out costs and significantly reduces timing risk. For example, investing INR 18,000 via six-monthly SIPs generally results in a better average purchase price than investing it once at a market high.

Avoiding Pitfalls: Common Mistakes In RCA Implementation

1. Pausing SIPs During Market Dips - Stopping investments during market downturns forfeits the opportunity to buy at lower prices, undermining the core advantage of RCA. History shows that investors who pause often miss out on market rebounds7.

2. Chasing Short-Term Performance - Switching funds based on recent returns disrupts portfolio stability and caps compounding benefits. Prioritizing fund quality and consistency over quick gains is key to RCA success.

3. Neglecting Fund Quality And Diversification - Selecting poor-quality funds or neglecting asset diversification exposes investors to concentrated risks. RCA works best with diversified portfolios and reputed fund managers.

4. Focusing On Short-Term Gains - RCA requires patience. Expecting quick profits leads to premature withdrawals, cutting short compounding gains, and reducing final corpus size.

5. Underestimating Inflation And Reviewing Investments - Not increasing SIP amounts to keep up with inflation can reduce the growth of your wealth. By increasing your investment amounts gradually each year, you can make the most of Rupee Cost Averaging, growing your total investment and earning more from compounding returns.

Conclusion

Rupee Cost Averaging offers a simple, disciplined way to invest that lowers risk, controls emotions, and harnesses compounding advantages over the long term. By sticking to regular investments regardless of market noise, investors stand a better chance of meeting their financial goals steadily and confidently.

For investors looking to diversify beyond mutual funds while gaining access to fixed income products with stable, transparent returns, Grip Invest offers a user-friendly platform with curated debt fund options and innovative features like automated reinvestment. Combining the steady, systematic approach of Rupee Cost Averaging with the reliability and convenience of platforms like Grip Invest can help build a robust, balanced portfolio designed for sustained financial growth.

FAQs On Rupee Cost Averaging

1. What is Rupee Cost Averaging?

It is investing a fixed amount regularly to buy more units when prices are low and fewer when prices are high, thus reducing average cost and timing risk.

2. What are the disadvantages?

Requires long-term commitment, may underperform lump sum in consistently rising markets, and demands investment discipline.

3. Is RCA effective in all market conditions?

It excels in volatile and bear markets, while providing consistent growth support in bull markets, especially over the long term.

References:

1. AMFI India, accessed from: https://www.amfiindia.com/mutual-fund

2. Clear Tax, accessed from: https://cleartax.in/s/rupee-cost-averaging-works

3. Motilal Oswal MF, accessed from: https://www.motilaloswalmf.com/Pdf/Products/equity/2048794609SIP-PPT---july-2018.pdf

4. Aditya Birla Capital, accessed from: https://www.adityabirlacapital.com/abc-of-money/what-is-a-systematic-investment-plan

5. HDFC Fund, accessed from: https://www.hdfcfund.com/learners-corner/intermediate/making-rupee-cost-averaging-work-you

6. Bajaj MC, accessed from: https://www.bajajamc.com/knowledge-centre/how-rupee-cost-averaging-works-in-sip-investments

7. Angel One, accessed from: https://www.angelone.in/knowledge-center/mutual-funds/rupee-cost-averaging-in-sip

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks, including delay and/ or default in payment. Read all the offer-related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for the consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001