SBI Bond Interest Rate: Latest Rates And How They Work

When people think about investing with the State Bank of India, fixed deposits (FDs) are usually the first option that comes into everyone’s mind.

However, there’s another option that often gets overlooked such as SBI bonds. If your deposit is currently in an SBI FD earning around 6.05% to 6.40% annually, it’s worth considering whether you could be earning more elsewhere.

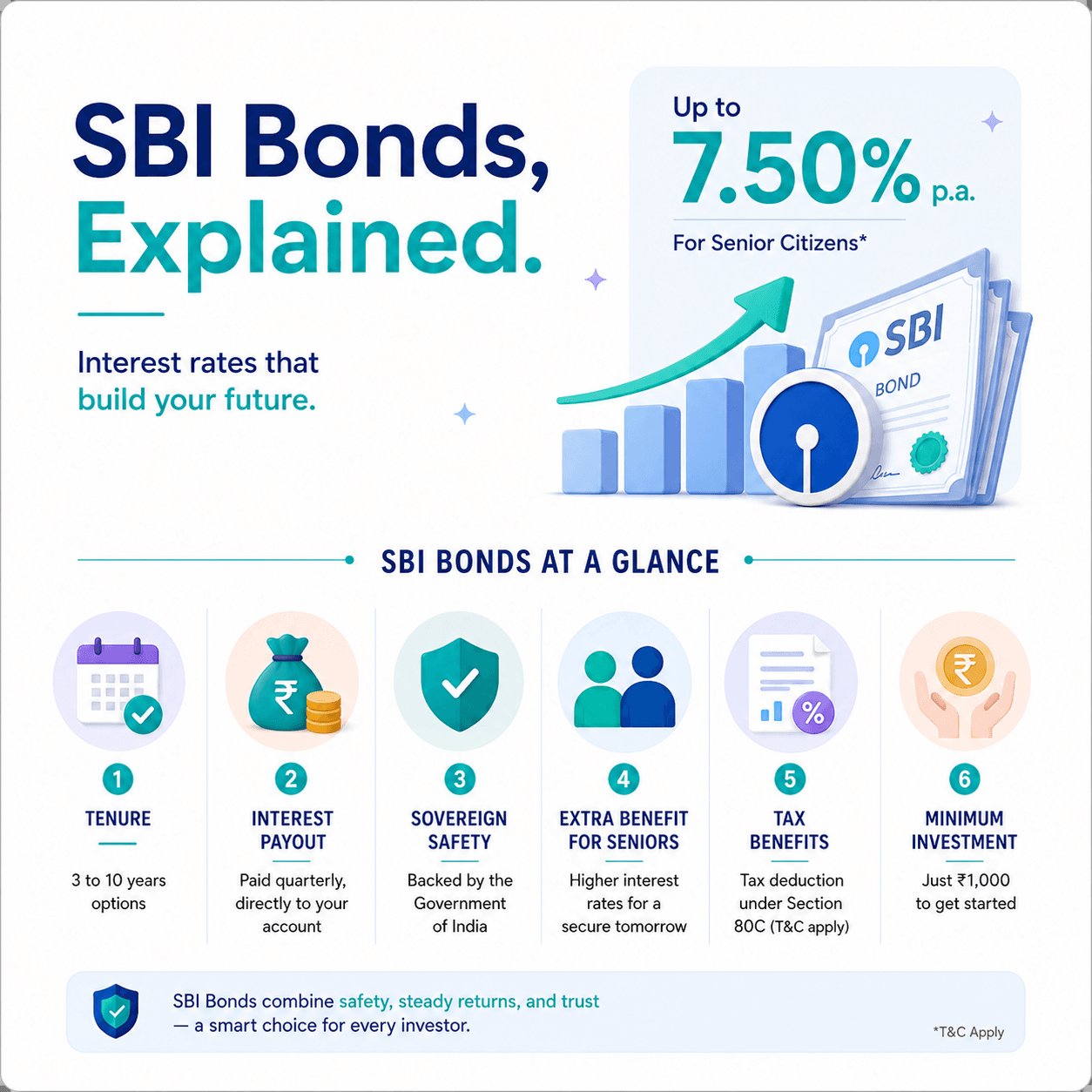

SBI bonds, relying on their type and duration, have recently offered interest rates ranging from 6.93% to 8.05% per year. This makes them an attractive choice for investors which are looking for higher, stable returns from a reliable, government-backed institution.

That said, there are various new bond investors who get confused by one key concept: the difference between a bond’s coupon rate and its yield. The coupon rate is the fixed interest mentioned on the bond, while the yield reflects the actual return based on the price you pay for it in the market. Understanding this difference is essential for making better investment decisions.

What SBI Bonds Include?

SBI issues have various categories of bonds to raise capital for its operations and regulatory requirements. Here's a breakdown of the main types available to investors:

1. RBI Floating Rate Savings Bonds (Distributed by SBI)

These are government-backed bonds that are issued by the Reserve Bank of India and distributed through SBI branches. The interest rate is not fixed and it's linked to the National Savings Certificate (NSC) rate plus a spread of 0.35%.1

1. Current Rate (Jan–Jun 2025): 8.05% per annum, paid semi-annually on 1st January and 1st July each year.

Tenure: 7 years | Minimum Investment: ?1,000 | No maximum limit

2. SBI Tier II Bonds

Tier II bonds are subordinated debt instruments that SBI issues to meet regulatory capital requirements under Basel III norms. They're rated AAA by domestic agencies like CRISIL and CARE, the highest safety rating.

3. Latest Issuance (October 2025): SBI raised ?7,500 crore through 10-year Tier II bonds at a coupon rate of 6.93% per annum the largest bank bond issuance of FY2025-26.2

3. SBI Additional Tier 1 (AT1) Bonds

AT1 bonds are perpetual in nature they have no fixed maturity date. These are rated AA by domestic agencies and offer higher coupons (~7.7% as seen in recent issuances) to compensate for the added risk.

However, they come with a significant caveat: in times of financial stress, the principal can be written down. These are strictly for institutional or sophisticated investors and are NOT recommended for retail investors.

4. SBI Infrastructure Bonds (Indicative)

Issued to fund infrastructure projects, these bonds have historically offered yields in the range of 7.5% to 8.6% per annum depending on the tenor and market conditions. Being AAA rated and linked to India's infrastructure growth story, they appeal to long-term investors.3

Table 1: SBI Bond Types at a Glance (2025 Data)

Bond Type | Coupon / Rate | Tenure | Key Feature |

| RBI Floating Rate Savings Bond (via SBI) | 8.05% p.a.* | 7 years | Linked to NSC rate + 0.35% spread; semi-annual payouts |

| SBI Tier II Bond (Oct 2025 issuance) | 6.93% p.a. | 10 years (call at 5) | AAA rated; largest bank bond issuance in FY26 |

| SBI AT1 (Additional Tier 1) Bond | ~7.7% p.a. | Perpetual | AA rated; higher risk; not for retail investors |

| SBI Infrastructure Bond (indicative) | 7.5%–8.6% p.a. | Varies | Issued to fund infra projects; AAA rated |

Source: SBI Bond Type In India.4

To understand how much your bond investment can grow over time, use a bonds calculator to calculate estimated returns and compare different investment scenarios

How SBI Bond Interest Rates Are Decided?

SBI bond coupon rates don't emerge in a vacuum. Three primary forces shape them:

1. RBI Monetary Policy

The Reserve Bank of India's repo rate directly influences borrowing costs across the banking system. When the RBI raises rates, bond yields typically rise to remain competitive.

Conversely, when the RBI cuts rates, new bond issuances tend to carry lower coupons. In April 2025, the RBI cut the repo rate by 25 basis points to 6.0%, signaling an easing cycle that has already begun to soften new bond coupon rates.

2. Credit Rating

SBI's consistently high credit ratings AAA for most long-term bonds and AA+ for AT1 bonds from CRISIL, CARE, and ICRA mean the bank can raise funds at relatively low rates.

A higher credit rating = lower risk = lower coupon needed to attract investors. This is why SBI bonds offer lower rates than similarly tenured corporate bonds from mid-rated companies, but they also carry significantly less credit risk.

3. Tenure And Market Demand

Longer tenures generally command higher interest rates. The October 2025 SBI Tier II bond (10-year) priced at 6.93% is a case in point; it attracted bids three times the base issue size, reflecting strong institutional demand. Market participants had expected the bond to price between 6.95%-7.00%, but the overwhelming demand allowed SBI to price it 7 basis points tighter.

Current SBI Bond Interest Rate Trends

Recent Coupon Rates at a Glance

- RBI Floating Rate Savings Bond (via SBI): 8.05% p.a. (Jan-Jun 2025)

- SBI Tier II Bond (Oct 2025): 6.93% p.a.

- SBI AT1 Bonds (2021 issuance reference): ~7.7% p.a.

- SBI Tier II Bond Coupon (INE062A08249): 7.74% p.a. (ISIN listed on BondsIndia).5

Comparison with SBI Fixed Deposits

As of December 15, 2025 (latest revised rates), SBI FD rates for the general public range from 3.05% (7-day deposits) to 6.40% (2-3 year tenure) per annum, with the special Amrit Vrishti 444-day FD offering 6.60%.

Table 2: SBI FD Rates vs SBI Bond Yields, Tenure-Wise Comparison (2025)

Tenure | SBI FD Rate (General) | SBI Bond Yield (approx.) | Advantage |

| 1–3 years | 6.25%–6.40% | 7.5%–7.74% | Bonds ~130–150 bps higher |

| 5 years | 6.05% | ~7.8%–8.0% | Bonds ~175–195 bps higher |

| 7 years (FRSB) | N/A (max 10 yr) | 8.05% (floating) | Gov-backed; floating rate protection |

| 10 years (Tier II) | ~6.05% | 6.93% | Bonds ~88 bps higher |

Source: SBI FD Rates vs SBI Bond Yields.6

How Rates Have Changed In Recent Years

Between 2020 and 2022, when the RBI maintained accommodative monetary policy, SBI bond coupons were lower for instance, a 2020 issuance saw rates around 6.8%.

As inflation pressures built and the RBI began hiking rates from May 2022, SBI bond rates firmed up, with AT1 bonds touching ~7.7% in 2021 and Tier II bonds reaching ~8.29% in some earlier issuances (2015 Series I). With the RBI now back in an easing cycle in 2025, new issuances like the October 2025 Tier II bond at 6.93% reflect this declining rate environment.

Risks Investors Should Know Before Buying SBI Bonds

SBI bonds are among the safest fixed-income instruments in India. But 'safe' is not the same as 'risk-free.' Here are the three primary risks every bond investor must understand:

1. Interest Rate Risk

If you buy a 10-year SBI Tier II bond at 6.93% and market rates rise to 8% a year later, your bond's market price will fall, because new investors can get 8% elsewhere. This risk is relevant only if you need to sell before maturity. If you hold to maturity, you receive your full principal back.

2. Liquidity Risk

Not all SBI bonds trade actively on exchanges. While Tier II and listed bonds have some secondary market presence, the bid-ask spreads can be wide for smaller investors. This means you may not be able to exit at a fair price in an emergency.

Important: The RBI Floating Rate Savings Bond (distributed via SBI) cannot be used as collateral for loans. Premature redemption is only allowed for senior citizens above 60 years, subject to conditions.

3. Reinvestment Risk

When you receive semi-annual coupon payments, you'll need to reinvest that money somewhere. If interest rates have fallen by then, your reinvested income earns less than expected, eroding your effective overall return.

Conclusion

SBI bonds offer a compelling proposition: the trust and creditworthiness of India's largest public sector bank, combined with returns that meaningfully beat SBI fixed deposits across comparable tenures.

Whether it's the government-backed RBI Floating Rate Savings Bond at 8.05% or a listed SBI Tier II bond with a yield of 6.93%-7.74%, investors who are comfortable with bond mechanics can earn materially more than what a standard FD offers.

That said, the bond market is not one-size-fits-all. SBI bonds are just one piece of the fixed-income universe. Comparing across issuers, including AAA-rated PSU bonds, infrastructure bonds, and high-rated NBFC bonds can help you optimise your yield without compromising on safety.

This is where platforms like Grip Invest come in.

Grip Invest allows you to compare listed bonds across multiple issuers on a single platform, so instead of manually hunting for the best coupon across SBI, NABARD, REC, or PFC bonds, you can view yields, ratings, tenures, and prices side-by-side.

For investors who want AAA-rated security but also want to explore whether another top-rated issuer might offer 20–50 basis points more in yield for the same tenure, Grip Invest's bond comparison tools help you make that call with clarity and confidence.

The SBI bond interest rate story in 2025 is ultimately one of opportunity for higher yields, strong safety, and the flexibility to participate in India's growing bond market.

FAQs On SBI Bond Yields, Returns & Key Questions

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001