Section 54F Of Income Tax Act: Exemption Rules, Conditions And Calculation

If you sell long-term capital assets, such as shares or land, you typically have to report the sale to the tax authorities. If they were sold at a higher price than the invested value, long-term capital gains tax applies to that profit.

As long-term capital gains taxes can take an unexpected amount of your sale proceeds, careful tax planning ahead of time may help you save money on your income taxes. Using the provisions of section 54F is a great way to defer taxes from the sale of a long-term asset. It will help you to build your wealth as an investor without giving away a substantial amount of it in income taxes.

This provision has been established to encourage individuals to make investments in residential real estate and protect their capital gains.

Understanding this provision can have a positive impact on your financial health.

What Is Section 54F, And What Problem Does It Solve?

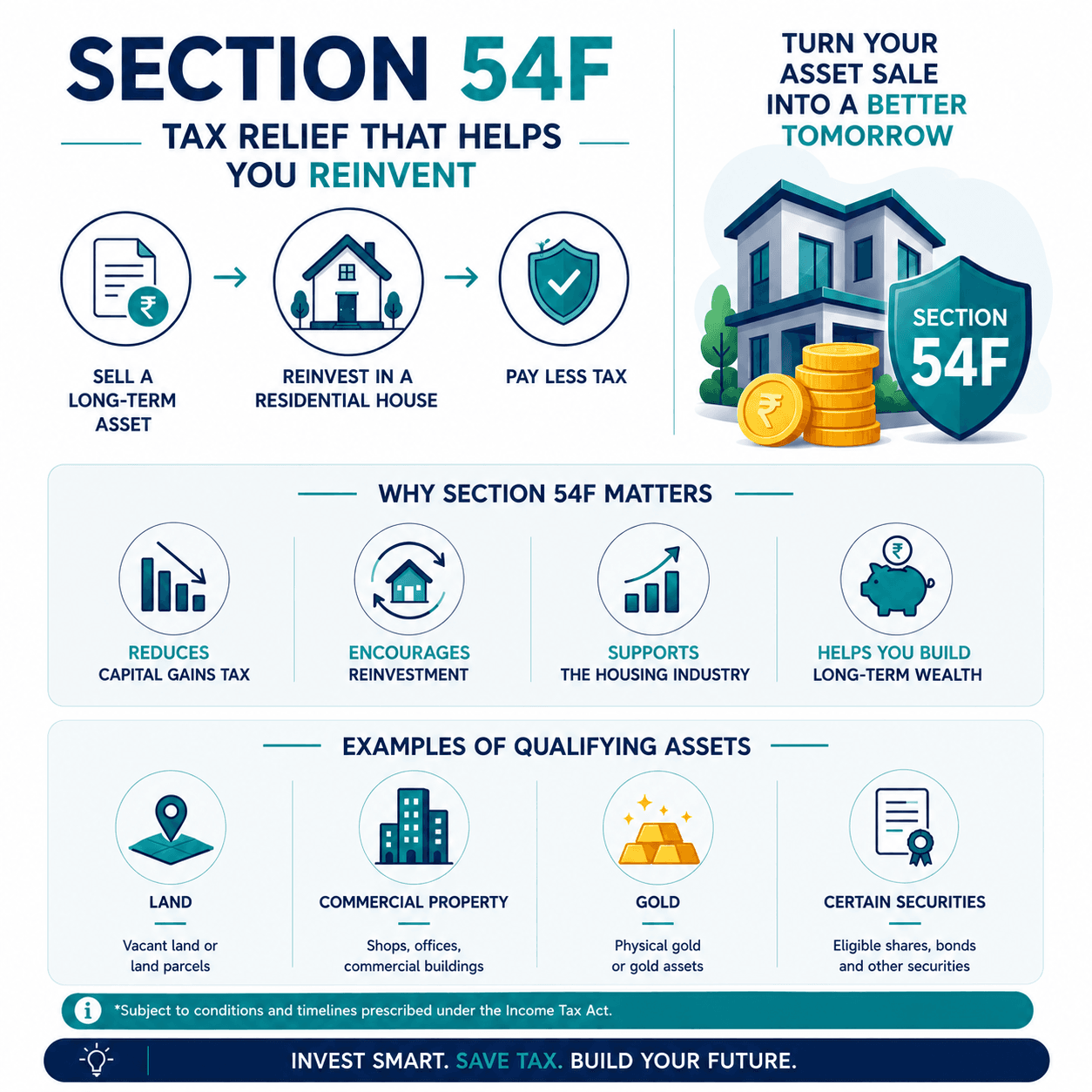

Section 54F is a provision that provides tax relief from capital gains taxes for individuals (including HUFs) who are caused by the sale of a long-term capital asset that has been owned long enough to qualify as a long-term capital asset, as per the rules for that asset category.

When an individual sells a long-term capital asset, they will normally pay long-term capital gains tax under the Indian Income Tax Act. Since the intent of section 54F conditions is that the proceeds of the sale of a long-term capital asset are to be reinvested in a new property or home.

So, the amount of capital gains tax payable upon the sale of a long-term capital asset can be reduced based on the value of the new residence.

The issue of high taxation during asset sales can deter investors from selling due to the amount of taxes they will owe. However, through the Section 54F exemption, investors are able to more easily invest their money back into productive investments, using the value of an asset they just sold.

The Section 54F exemption can also aid in the housing industry and provide tax benefits to the seller and subsequent buyer.

Many taxpayers have successfully utilised Section 54F to help lessen the impact of taxes on the sale of an asset or investment.

Which Assets Qualify For 54F Exemption?

Section 54F helps you save tax when you sell a long-term asset like land, commercial property, gold, or certain securities and use the money to buy a residential house in India.

A few things you should know:

- The asset you sell must be held for the long term. For most properties, this means more than 24 months. For listed securities, it is more than 12 months.

- If you sell a short-term asset, you cannot claim this exemption.

- Both Indian residents and NRIs can use Section 54F to save tax.

- You must buy or build the new house within the time limits set by the Income Tax Act.

- On the date of sale, you should not own more than one residential house apart from the new one you are buying.

It is a good idea to check how long you have held the asset before planning your sale. Speaking to a tax expert can help you make the most of this exemption.

The Core Condition: Buying Or Building A Residential House

To qualify, you will need to reinvest in one property located in India. Timelines are very strict as this is a requirement.

- Purchase option: You may purchase a new property within the time frame of one year before or two years after your previous property's sale date. This allows you flexibility in your plans.

- Construction option: You will have three years from the date of your sale to finish building your new property. There is enough time for you to complete your building project and allow for you to make any necessary changes if needed.

After the building has been completed, it must also be ready for you to move in. If you start building but do not finish within the time frame, you will not qualify under these regulations.

If you are unable to reinvest immediately, you may place the unused funds into the Capital Gains Account Scheme (CGAS) prior to filing your tax returns. This will keep your application active.

Proportional Exemption: How It's Calculated When You Don't Reinvest Full Proceeds?

The policy will also apply to an overall benefit proportioned against what you invested into your new property, so you do not need to reinvest your entire cash proceeds when you sell.

The exemption will be calculated based on how much net cash proceeds you actually put into your new property.

Simple formula:

Exemption = Long-term Capital Gain × (Amount invested in new house / Net sale consideration)

Net sale consideration is the full sale value minus expenses like brokerage or legal fees.

For Example:

Ramesh sells equity shares for INR 50 lakhs. He held them for over 24 months, so long-term capital gain is \INR 20 lakhs after indexation. He reinvests INR 35 lakhs in buying a new flat within the allowed time and does not own more than one house on the sale date.

Exemption = INR 20 lakhs × (INR 35 lakhs / INR 50 lakhs) = INR 14 lakhs.

Taxable gain = INR 6 lakhs. This way, even partial reinvestment saves a good portion of tax. Full reinvestment would exempt the entire INR 20 lakh gain.

Key Restrictions That Can Disqualify Your Claim

There are several significant conditions governing the Section 54-F provision that will protect the integrity of this provision. Violating any of these conditions can result in losing some or all of the benefits of this provision.

- You cannot own more than one residential dwelling as of the date of closing on your original property (with the exception of the new property being purchased).

- You cannot dispose (sell) of your new property prior to the expiration of 3 years from the date of purchase or completion of construction of your new property. If you do, the original exemption from the sale of your original property will be reversed, and the original benefit will become taxable.

- You cannot purchase another residential building within two years or construct a residential building within three years of the date of sale of your original property.

The conditions set forth in section 54-F limit the number of times that you may sell, flip, and purchase another primary residence.

If you fail to meet the requirements of subsection 54-F at any time after the sale of your original property, the amount of the previously exempted sale will be added to your taxable income for that tax year. You should plan well to avoid any unexpected tax implications relating to any of the above issues.

Lastly, one of the requirements of subsection 54-F states that new properties must be located in India. You should always maintain accurate and complete records for all transactions and dates when you engage in these transactions.

Also Read: Section 80CCD Deductions In Income Tax

Section 54F vs Section 54: Quick Comparison

| Particulars | Section 54 | Section 54F |

| Applicable On Sale Of | Residential house property | Any long-term capital asset other than a residential house |

| Eligible Taxpayers | Individuals and HUFs | Individuals and HUFs |

| Reinvestment Requirement | Invest capital gains amount | Invest net sale consideration |

| Type of New Asset | One residential house in India | One residential house in India |

| Exemption Calculation | Based on amount of capital gains invested | Based on proportion of sale proceeds reinvested |

| Ownership Restriction | Relatively flexible in certain cases | Cannot own more than one residential house (excluding new house) on sale date |

| Purchase Timeline | 1 year before or 2 years after sale | 1 year before or 2 years after sale |

| Construction Timeline | Within 3 years from sale | Within 3 years from sale |

| Applicable To NRIs | Yes | Yes |

| CGAS Benefit Available | Yes | Yes |

| Lock-in Period For New House | 3 years | 3 years |

Which Applies When?

Many people can mix up these two similar-sounding provisions. Knowing the difference allows for proper choice. 54F vs 54 Income Tax Comparison is an important issue. Section 54 applies to the sale of a residential home and reinvestment of the proceeds into another residential home. Section 54F applies to any other long-term asset sold, i.e., either shares or gold.

In Section 54, the exemption amount will be based on the gain that is reinvested. In Section 54F, the exemption amount will be determined by taking the proportion of the total amount realised from the sale of an asset that is reinvested. The ownership requirements in Sections 54 and 54F will have substantial differences. Under Section 54, an individual will have more flexibility in relation to his/her existing houses in certain situations.

Understanding the difference between Section 54 and 54F helps you choose the correct exemption. Always ensure that you sell the asset that is being compared against the appropriate section.

Conclusion

Section 54F can be a powerful tool for reducing long-term capital gains tax while simultaneously building long-term wealth through residential property ownership. By reinvesting eligible capital gains into a residential house within the prescribed timelines, taxpayers can significantly optimise their tax liability and strengthen their financial planning goals, including retirement security and family wealth creation.

The provision also encourages productive deployment of capital into real assets instead of leaving gains idle or exposed to unnecessary taxation.

However, to fully benefit from Section 54F, taxpayers must maintain proper documentation, comply with eligibility conditions, and make timely investments or deposits under the Capital Gains Account Scheme (CGAS), where applicable.

While real estate can play an important role in wealth preservation and tax planning, a well-balanced portfolio should also include diversified investment avenues that offer liquidity, stability, and regular income potential. Platforms like Grip Invest allow investors to explore fixed-income opportunities such as corporate bonds and other alternative investments that can complement long-term financial planning alongside real estate investments.

FAQs On Section 54F

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001