Sequence Of Returns Risk: The Hidden Danger In Retirement Planning

The process of retirement planning involves systematic savings over a considerable period so that an individual has an adequate corpus to withdraw from after retirement. The earlier you start, the higher the ROI (Return on Investment), the greater your retirement fund, and accordingly, your monthly withdrawal.

However, investors often ignore a critical aspect in retirement planning: the sequence of returns risk.

This can be illustrated with a simple example: suppose two individuals retire with the same corpus and earn the same average annual return; there is a chance that one might run out of money, whereas the other’s portfolio lasts throughout the retirement period. This is when they withdraw the same amount per month to cover their lifestyle expenses.

As an investor, you should have clarity about the sequence of returns and risk and consider it during your retirement planning. During retirement, the timing of market gains and losses can influence how long your savings last, even if long-term returns appear similar.

What Is The Sequence Of Returns Risk?

Consider a situation where the average returns on a portfolio is 15% per annum consistently for twenty years. On the other hand, a second case where the average return is 15% per annum for the given period, but there are periods with very high, very low, zero, and negative returns.

Sequence of returns risk refers to the danger that the order in which investment returns occur can affect the sustainability of a retirement portfolio. This risk is most relevant during the withdrawal phase, when investors depend on their accumulated savings rather than adding new contributions.

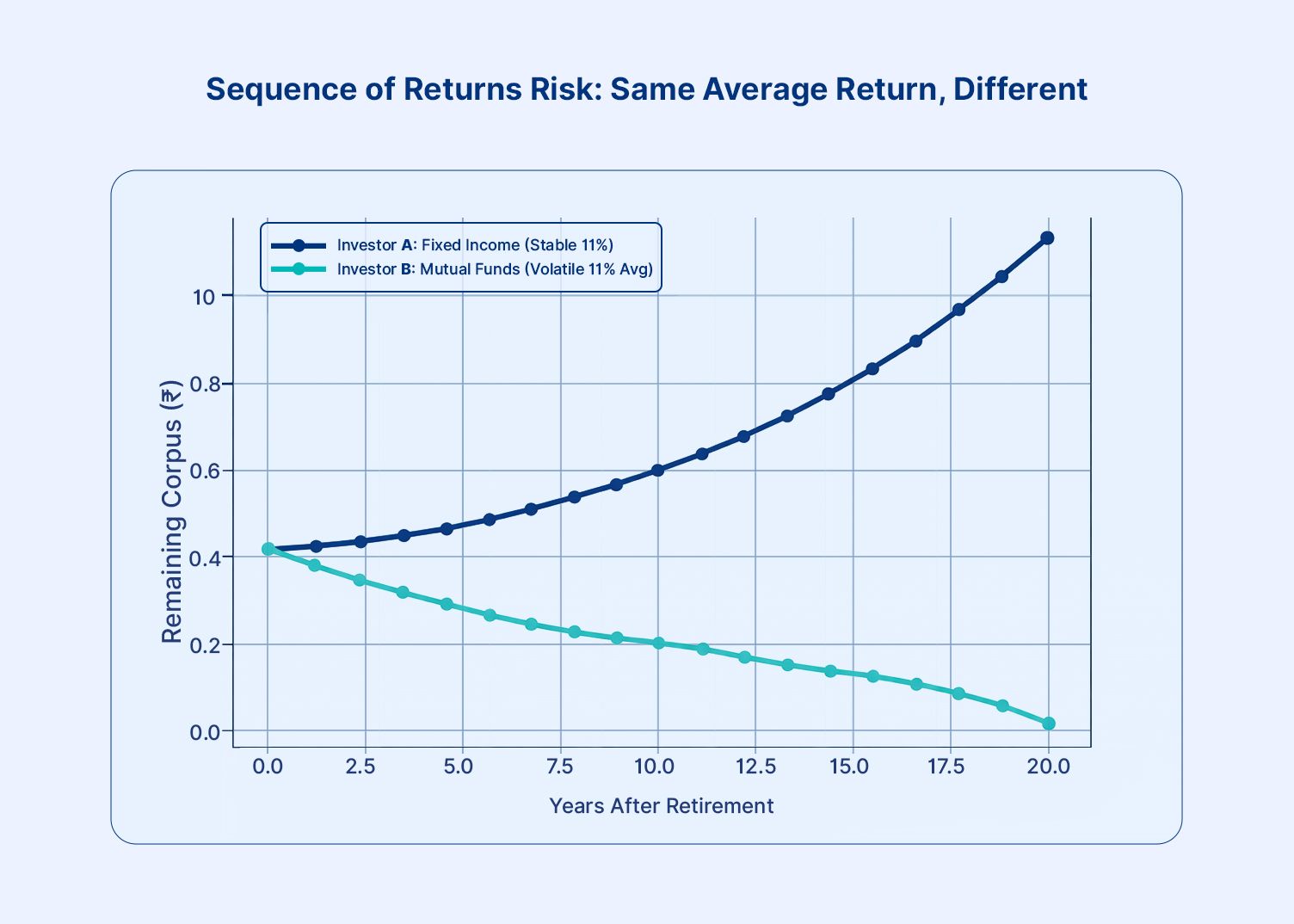

Let us consider the following graph:

Figure 1.0: Sequence of Returns Risk (Investor A vs. Investor B)

In the above example, Investor A and Investor B started the retirement with a INR 25 lakh corpus and withdrew INR 1.5 lakhs per annum. Investor A’s funds were deposited in a fixed income investment at 11% per annum. Investor B had invested in different assets with volatile returns, but the average return for 11 years was 11% (per annum). As it is clear, Investor B’s corpus turned negative in the sixteenth yea,r whereas, despite the withdrawals, Investor A’s corpus continued to rise.

The order of returns impact becomes critical because withdrawals during market downturns reduce the invested capital base. When markets recover later, gains apply to a smaller amount, limiting the portfolio’s ability to grow. As a result, two investors with identical average returns may experience very different outcomes depending on when market losses occur.

How It Impacts Retirement Portfolios

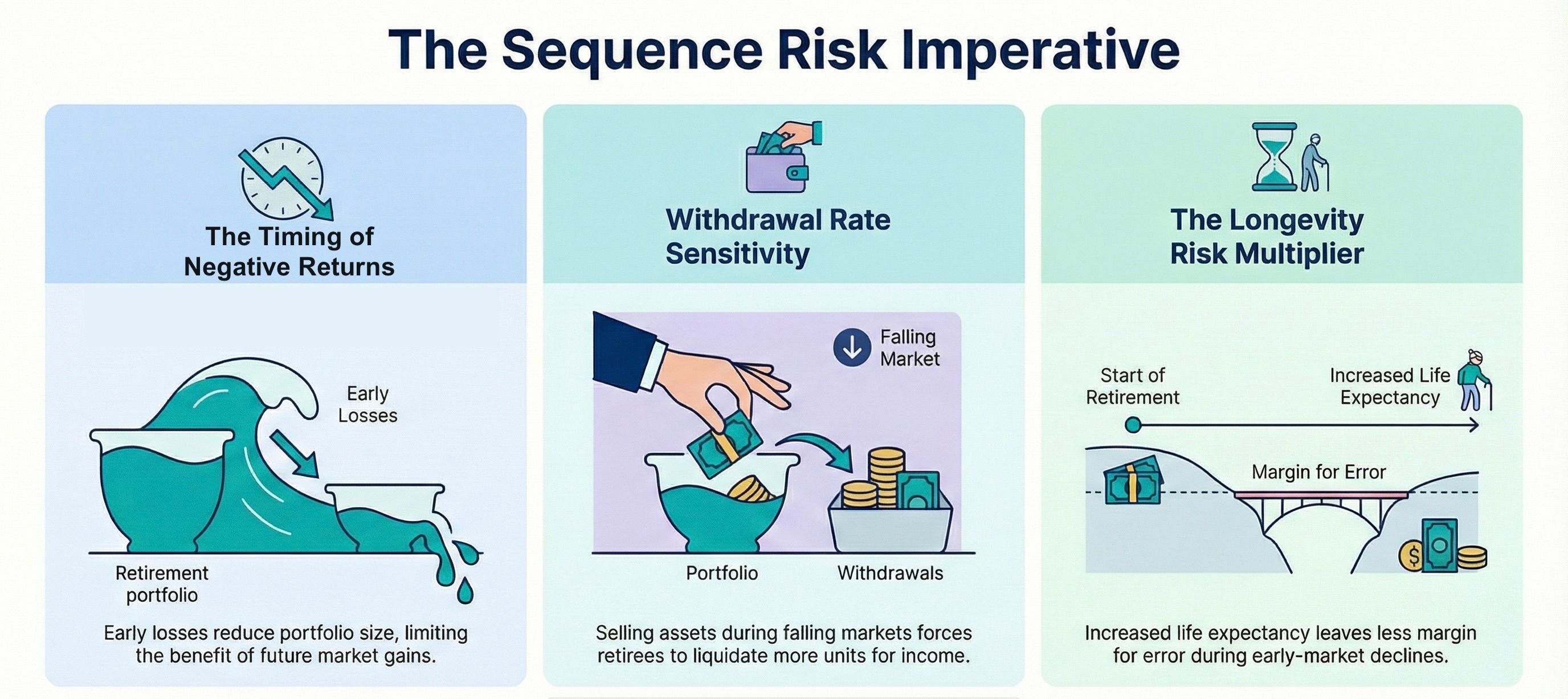

1. Early Negative Returns Impact

As illustrated in the example above, if the investor suffers negative returns in the early years, the risk of retirement portfolio depletion or even negative territory increases significantly. Unlike investors in the accumulation phase, retirees cannot wait indefinitely for markets to recover without consequences.

The reduced portfolio size limits the benefit of future market gains. Even if the market performs well later, the portfolio's average return might increase, but the corpus value might not recover due to planned withdrawals and fund depletion during the early years.

2. Withdrawal Rate Sensitivity

Portfolio withdrawal timing plays a crucial role in determining sustainability. When withdrawals continue during falling markets, investors are forced to sell more units to generate the same income. This accelerates capital erosion and reduces the portfolio’s ability to recover.

3. Longevity Risk Interaction

Sequence risk retirement becomes even more significant when combined with longevity risk. As life expectancy increases, retirees must ensure their savings last longer. Early market declines increase the probability of exhausting funds prematurely. Hence, there is a massive uncertainty in retirement planning. Even the portfolios designed with reasonable return assumptions can face critical challenges if the first few years witness poor or negative returns.

Real World Example (India Context)

The timing of market entry and exit, and the sequence of returns, can be two critical game-changers in retirement planning. One can understand it through a sequence of returns example, comparing two different retirees.

One investor retired in early 2008, just before the global financial crisis. During that period, the Nifty 50 declined by more than 50% from its peak. This investor began withdrawing funds while the market was falling sharply. As a result, their portfolio shrank rapidly, and even though markets eventually recovered, the damage had already been done.

Another investor retired in 2014, as markets entered a sustained bull phase. This investor benefited from positive returns in the early years of retirement. The portfolio of such an individual grew despite regular withdrawals, and the investor even had the option to increase annual withdrawals to meet lifestyle requirements.

As already mentioned, an investor can rebuild during the accumulation phase, but it becomes quite difficult during the withdrawal phase.

Mistakes Investors Make

Many investors consider ‘average returns’ from a fund or portfolio and fail to study the sequence of returns. It is quite critical to take into consideration the sequence of returns for proper retirement planning. Early market declines combined with withdrawals can permanently weaken a portfolio, even if long-term returns remain favourable. Maintaining excessive equity exposure near retirement and failing to diversify across asset classes increases vulnerability. A balanced allocation, including fixed income instruments, can provide stability during downturns.

Investors should also ensure that withdrawal planning is carefully carried out and that risk management is an integral part of retirement planning. It is interesting to note that the sequence of return risk, as illustrated by our example, can be reduced considerably if the returns from an investment are consistent throughout the retirement period. You may consider fixed-income securities and bonds as part of your retirement corpus on the Grip Invest platform, which offers you massive flexibility and also mitigates sequence risk.

FAQs

1. What is the sequence of returns risk in simple terms?

It is the risk that poor returns in the early years of retirement can accelerate the decline of your portfolio. Even with good long-term average returns, early losses combined with withdrawals can permanently weaken your retirement savings.

2. How do retirees protect against it?

Retirees can reduce this risk by maintaining a balanced portfolio, keeping some funds in fixed income, lowering withdrawals during downturns, and gradually shifting to safer assets before retirement.

3. Does SIP investing remove sequence risk?

No. SIP reduces timing risk when investing, but sequence risk persists in retirement because withdrawals during market declines can erode portfolio sustainability.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001