Short-Term Vs Long-Term Bonds: Which One Should You Pick In 2026?

India’s bond market is at a pivotal stage, shaped by volatile interest rate movements, global geopolitical shifts, and growing investor demand for stable, fixed-income options. With both government and corporate bonds offering distinct benefits, the challenge for investors in 2026 lies in choosing between short-term and long-term bonds.

Short-term bonds provide greater liquidity and lower interest rate risk, while long-term bonds offer the potential for higher returns but come with greater exposure to market fluctuations. Understanding the differences between these options and aligning them with your risk tolerance, return expectations, and financial goals is crucial for effective fixed-income planning.

This blog explores their features, benefits, and risks to help you make an informed choice between short-term and long-term bonds.

Difference Between Short-Term And Long-Term Bonds

Bonds are fixed-income investments in India in which you invest to generate consistent earnings. You can receive a fixed interest income and principal amount on maturity by investing in the best bond in 2026. However, you need to consider the financial goals and liquidity needs before you start investing. Therefore, let us understand the difference between short-term and long-term bonds.

1. Tenure And Maturity Period Explained

Most short-term bonds have a maturity ranging from 1 to 3 years (e.g., T-Bills, short-duration debt funds). Long-term bonds have maturities of 10-30 years and are typically government securities or corporate bonds.

However, if you are planning to invest in short-term corporate bonds, you can find these short-term corporate bonds (3–6 months) on Online Bond Platform Providers (OBPPs) like Grip Invest. Specifically, the Marketplace on Grip Invest always has such short-term bond options. To invest in short term bonds, click the link below and register now:

2. How Interest Rates And Risks Vary By Bond Duration

Bond investment strategy in India is often based on your financial goals and risk tolerance. The shorter the maturity of a bond, the less sensitive it is to interest rate changes and therefore the less the price volatility1.

Long maturity bonds typically yield higher interest rates, but in a rising rate environment, the longer the maturity, the greater the price interest rate risk. It is advised that investors should check the credit rating of the bond before investing in it. Both short-term and long-term bonds are rated by independent credit rating agencies, providing insights about the issuer’s strength. For example, a ‘AAA’ or ‘AA’ rated short-term bond is more secure and stable than a “BBB-” rated bond.

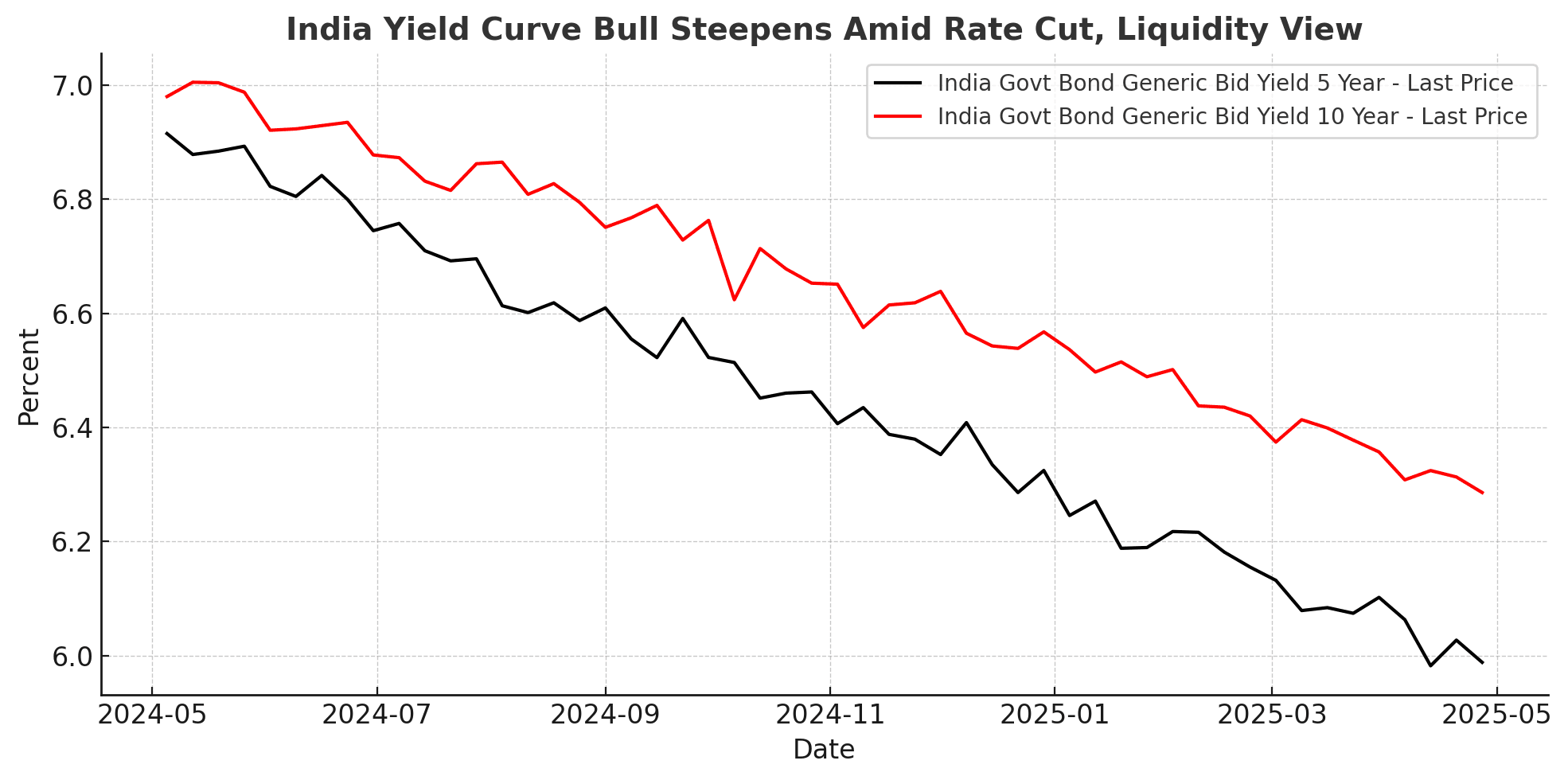

3. Understanding The Yield Curve

The yield curve is a graphical representation of bond yields across different maturities, indicating market expectations for interest rates and economic conditions.

Let us understand the bond yield curve in India below.

Source: Bloomberg

This chart shows India’s 5-year (black) and 10-year (red) government bond yields from May 2024 to April 2025. From mid-2024 to early 2025, yields on both 5-year and 10-year G-Secs generally softened, reflecting rate cut expectations. The drop in shorter maturities signals a bull steepening, where long-term yields fall less than short-term ones, suggesting optimism for growth recovery.

Returns: Long-Term Vs Short-Term Bond Investments

The returns received from long-term and short-term bonds depend on different parameters, such as bond ratings, issuer, current market conditions and interest rates. If you compare the returns from bonds based on maturity period, always ensure that you compare similarly rated bonds from the same category so that a clear picture of comparison is available.

1. Historical Returns Of Short-Term Vs Long-Term Bonds

In the Indian market, short-term bonds have historically delivered modest but stable returns, typically ranging between 5–6%, with lower sensitivity to interest rate changes. Long-term bonds, while offering higher average yields of 6–7%, have shown greater volatility due to rate fluctuations. Over the past decade, long-term bonds outperformed during rate-cut cycles, whereas short-term bonds excelled in rising rate environments2.

Note: The above comparison of the returns is presented for government bonds only. Please note that for corporate bonds of different ratings, the historical returns will change. For example, if you look at the historical return of ‘A’ rated corporate bonds, it ranges between 6.5% - 7.2% for a 5-year period. For a short term of 1 year, this return is around 7.5% - 8%. These figures are based on trends observed from Nifty’s Corporate Bond Indices3.

2. How Inflation Impacts Bond Returns

Interest rates typically increase due to inflation, which in turn decreases bond prices and increases bond yields. As inflation rises, new bonds issued with higher interest rates are more attractive to investors, lowering the market price of older bonds with lower yields.

Also Read: How Inflation Affects Investments And Smart Strategies to Stay Ahead

3. Tax Efficiency Of Long-Term Vs Short-Term Bonds

The investor's income slab determines the tax rate on interest earned on taxable bonds. As per the July 2024 amendment, the long-term bonds held for more than 12 months are subject to LTCG tax at 12.5% without indexation, whereas short-term bonds are subject to STCG tax at the slab rate.

Which Bonds Suit Your Investment Goals?

If you want a stable fixed income, consider short-term fixed income bonds. There are favourable rates, low risks in bond investing, and high liquidity that make it an attractive option for short-term financial planning.

However, given their growth potential and tax advantages, long-term bonds present an attractive choice. With yields on a declining trend, these bonds offer scope for capital gains if interest rates fall further. Many institutional investors, particularly insurance companies and mutual funds, are increasing their exposure to long-term bonds to capitalise on the yield spread advantage.

Hence, there is no one answer to the question of short-term bonds or long-term bonds. It depends on the investor's financial goals, their liquidity needs, and risk appetite.

Risks To Know Before Investing

Bonds generally carry lower risk sensitivity as they are debt instruments, often backed by collateral. However, long-term bonds tend to be more vulnerable to interest rate fluctuations. If the RBI maintains its recent neutral stance, market volatility could persist. Since interest rates and bond prices move inversely, rising rates push prices down, while falling rates lift them. Investors must be mindful of timing.

Liquidity and credit risks also play a role, as short-term corporate bonds may offer attractive yields but carry credit risk. A balanced perspective can be achieved by assessing current interest rate dynamics and comparing returns through platforms like the Grip Invest.

Conclusion

Bonds are fixed-income instruments that bring stability to your portfolio. There is a risk in bond investing, but they are less risky than shares as they are non-market-linked and offer predictable returns. The decision on whether to invest in short-term or long-term bonds is to be made according to the needs of your income, your tolerance for risk investing, and your opinion on the market prospects in 2026.

A flattened yield curve in India suggests a conservative approach, offering short-term stability, long-term growth potential, and tax benefits. You should focus on maximising your returns and effectively managing your investments. By balancing duration and diversifying between government and corporate bonds, investors can achieve stability and higher returns. To explore such opportunities, sign up on Grip Invest today and start earning fixed returns of up to 14%.

References:

- Reuters, accessed from: https://www.reuters.com/world/india/indian-companies-rush-sell-short-term-debt-rbi-monetary-boost-lowers-rates-2025-05-28/?utm_source=chatgpt.com

- Economic Times, accessed from: https://economictimes.indiatimes.com/markets/bonds/rbis-50-bps-rate-cut-sparks-short-term-bond-rally-long-term-yields-stay-subdued-whats-ahead/articleshow/121672419.cms?utm_source=chatgpt.com

- Nifty Indices, accessed from: https://niftyindices.com/indices/fixed-income/corporate-bond-indices

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001