Tax-Free Government Bonds: Definition, Advantages, And Who Should Invest

Introduction: Why Tax-Free Bonds Are Attractive To High-Income Individuals

In the case of investors belonging to higher tax brackets, the task is not only about making money but also about retaining it after paying taxes. This is where tax free gov bonds come into the picture because fixed income options like fixed deposits or corporates have tax implications that lower their return on investment.

The attractiveness of tax-free government securities lies in the fact that the income derived therefrom is tax-exempt under the Income Tax Act and therefore provides an added advantage to high-net-worth individuals seeking secure, tax-efficient long-term income. In a situation where equity markets are prone to volatility and taxes on debt securities are rising, such securities are among the few that are predictable and tax-efficient.

What Are Tax-Free Government Bonds?

1. Issuers and Structure

Government tax free bonds are offered by government-supported PSI undertakings. Historically, it has been noticed that tax free government bonds are issued by organisations such as NHAI, REC, PFC, IRFC, HUDCO, etc. These bonds are also known as tax free infrastructure bonds because they are used for funding infrastructure projects.

Although these are not directly issued by the Government of India, having the support of government-owned institutions helps to mitigate the risk of default.

2. Interest Income Exemption

The distinctive feature of tax free bonds India is that the interest income is fully tax-exempt under Section 10(15)(iv)(h) of the Income Tax Act1. This is so, irrespective of the income tax slab under which the taxpayer falls.

For example, an investor who falls under the 30% tax bracket and earns an annual return of INR 70,000 from the tax-free bond gets the entire return. In order to earn the same after-tax return from the taxable fixed deposit, the return has to be nearly INR 1,00,000.

Benefits Of Tax Free Government Bonds

1. Stable and Predictable Returns

The coupon rates in tax free government bonds are fixed on long maturities of, for instance, 10 years, 15 years, and 20 years. This makes them ideal for people with income that they want to stabilize, such as retirees with long-term financial plans.

Historically, the tax free bond interest rates in India vary from 5.5% to 8.5%2. The rates are based on the time of issue.

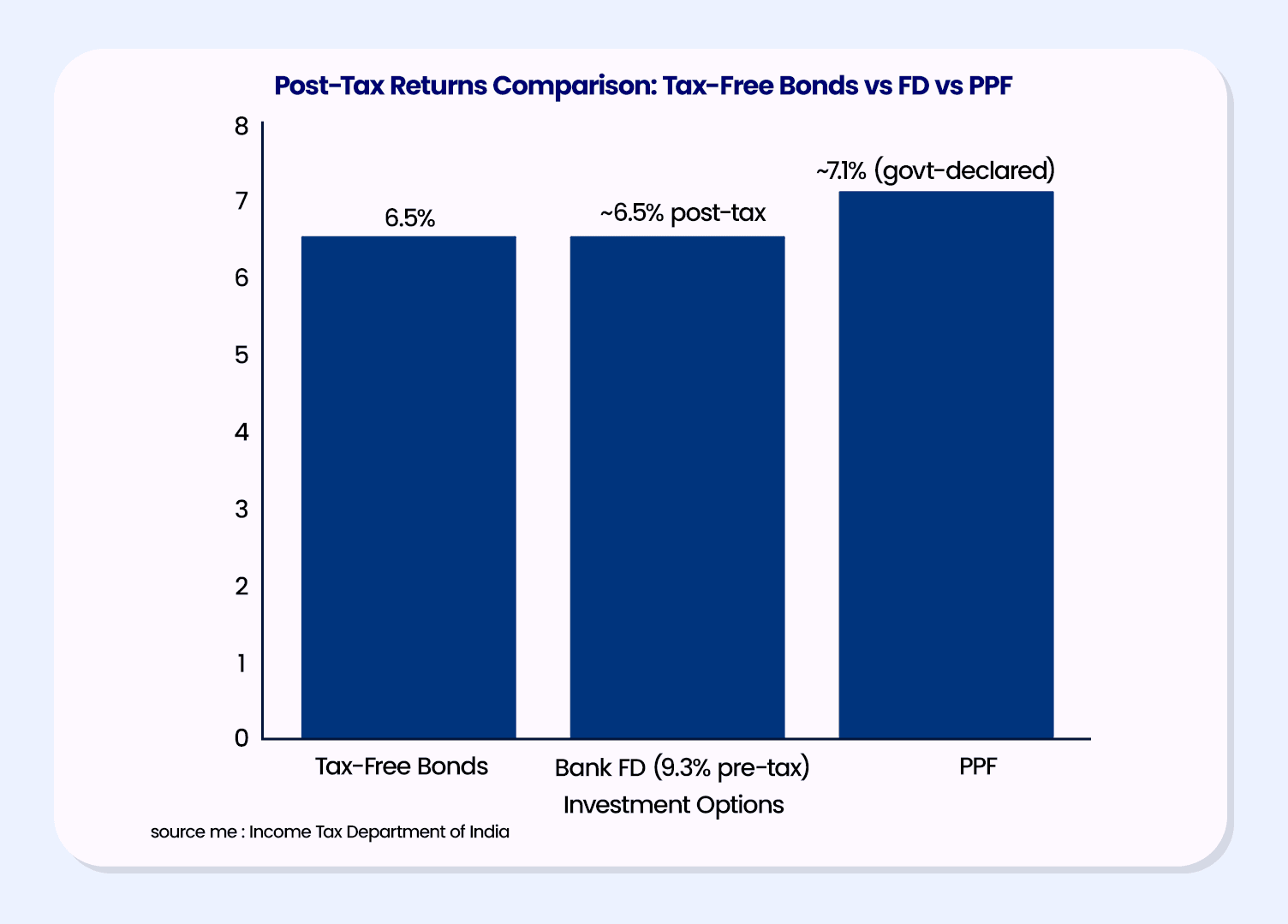

2. Higher Post-Tax Yield

The real value of tax free government bonds lies in their post-tax returns.

Hypothetical example:

- Tax-free bond yield: 6.5%

- Investor tax slab: 30%

Taxable equivalent return = 6.5% ÷ (1 - 0.30) = 9.28%

This makes the tax exempt bond returns much more competitive compared to the bank FDs or debt funds.

Note: Returns shown are illustrative. FD post-tax returns assume a 30% income tax slab. PPF returns are based on the latest government-declared rates. Tax-free bond yields vary based on issue year and issuer.

FD pre-tax return assumed at ~9.3% to arrive at a 6.5% post-tax return for a 30% tax slab investor.

3. Low Credit Risk

Being mostly issued by PSU-backed organizations, tax-free bonds offered by the government usually possess high credit ratings (AAA and equivalent). This results in less default risk for these instruments compared to bonds and unsecured debt offered by the private corporate sector.

4. Visibility of Income

Given the long maturity period, the tax-free bonds seem to be the best for the investor with long-term financial goals, like preparing for the retirement period.

Risks And Limitations To Know

More often these tax free government bonds come with a few drawbacks some of them include:

1. Liquidity Constraints

Although publicly traded, tax-free bonds can find themselves with limited liquidity when sold after issuance and before maturity at a discount, particularly when the overall cycle of interest rates is increasing.

2. Limited Availability

Currently, there has been no new issuance of tax-free bonds of large amounts in the recent past. This has led to access being provided through secondary market platforms or carefully designed platforms.

3. Interest Rate Sensitivity

As with other long-term bonds, prices of tax-free bonds will fall when interest rates go up. Even though it won’t have any bearing for the investors holding until the end of the term, it becomes important for early withdrawers.

Tax-Free Bonds Vs Other Tax-Saving Options

Tax Free Bonds vs PPF

Feature | Tax-Free Bonds | PPF |

Lock-in | None (market-linked exit) | 15 years |

Risk | Low | Sovereign |

Liquidity | Moderate | Restricted |

Returns | Fixed, higher for HNIs | Govt-declared |

Tax | Interest tax-free | Fully tax-free |

In the matter of tax free bonds vs PPF, flexibility as well as better yields can be achieved through bonds, whereas PPF is ideal for conservative and long-term investors.

Tax-Free Bonds In 2026: What Investors Should Know

The market for tax free bonds 2026 remains largely active through the secondary market. HNIs have shown robust demand based on the following factors:

- Increased taxes on debt funds (as per the new tax regulations)

- Loss of attractiveness of conventional tax-efficient tools

- Desire for predictable, tax-efficient income Desire for predictable

As a consequence, platforms that showcase high-quality bond opportunities have started to gain prominence.

Who Should Consider Investing in Tax-Free Government Bonds?

- Investors in the 30% or higher tax bracket

- Persons retiring expecting fixed, tax-free income

- Conservative Investor Diversification Out of Equity Risk

HNIs giving priority to post-tax returns Long-term investors who can hold bonds to maturity

How Investors Can Buy Bonds Today

Today, investors can access tax-free government bonds through platforms like Grip Invest, which simplify participation in the fixed-income market by offering curated and thoroughly screened bond opportunities. Instead of navigating fragmented or low-liquidity exchanges, investors can review key details such as issuer profile, tenure, yield, credit quality, and cash flow visibility in one place before making an informed decision.

These platforms also enable side-by-side comparisons of tax-free bonds, government securities, and other fixed-income instruments, helping investors evaluate options based on post-tax returns, risk profile, and investment horizon. By improving transparency and accessibility, such platforms make it easier for investors to incorporate fixed-income products into a well-balanced portfolio without unnecessary complexity.

Before investing in bonds, you can use a bonds calculator to estimate potential returns, interest payouts, and maturity value based on your investment amount and tenure.

Conclusion

For investors in higher tax brackets, tax-free government bonds continue to stand out as a rare combination of predictable income, tax efficiency, and relatively low credit risk. At a time when taxation on traditional debt instruments has increased and equity markets remain volatile, these bonds offer clarity on post-tax returns, something many income-focused investors value.

While limited fresh issuance and liquidity considerations mean they are not suitable for short-term goals, tax-free bonds can play a meaningful role in long-term income planning, especially for retirees and conservative investors who prioritise stability over aggressive growth. As with any fixed-income investment, understanding interest rate sensitivity and holding period expectations remains crucial before investing.

For investors looking to explore available tax-free bond opportunities in today’s market, platforms like Grip Invest help simplify access to vetted fixed-income instruments while enabling informed comparisons across bonds and other income options.

FAQs

1. Are tax-free government bonds completely risk-free?

Tax-free government bonds are considered low risk because they are issued by PSU-backed institutions with high credit ratings. While they are not technically sovereign bonds, the government backing significantly reduces default risk compared to corporate bonds.

2. Can tax-free bonds be sold before maturity?

Yes, tax-free bonds are listed and can be sold in the secondary market. However, liquidity may be limited, and prices can fluctuate based on interest rate movements, so returns may differ from the original yield if sold early.

3. Are tax-free bonds better than debt mutual funds after recent tax changes?

After the removal of indexation benefits on many debt funds, tax-free bonds have become more attractive for investors in higher tax brackets. Their fully tax-exempt interest often results in superior post-tax returns for long-term, income-focused investors.

References:

1. Tax man, accessed from: https://tinyurl.com/4nn736hr

2. NSDL, accessed from: https://nsdl.co.in/downloadables/The%20Financial%20Kaleidoscope%20-%20Oct%2015%20issue.pdf

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities are subject to risks. Read all the offer-related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading. This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip Invest”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip Invest or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip Invest does not guarantee or assure any return on investments and accepts no liability for the consequences of any actions taken based on the information provided. For more details, please visit https://www.gripinvest.in/.

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001.