Why Investing Early Is Important: Power Of Compounding In Action

Is it possible to have fun now, while staying financially secure for the future?

The world today wants to live in the moment. From fancy gadgets to Insta-worthy vacations, it is all about having the best now. This automatically makes our investments for the future take a backseat. The typical dialogue of every 23-year-old:

“If I cannot afford a Starbucks coffee most days, how can I start investing in 20s?”

But does it have to be this way? Is a secured future and a happening life impossible to co-exist?

Meet Sara. She started investing INR 3,000 per month when she was 25 years old. This means she saved ONLY INR 100 every day, much less than a cup of coffee. Sara continues this for 10 years and stops investing fresh funds, but lets her investments grow. By the time she is 65, she would have an INR 1.2 crores, assuming a modest 10% annual return.

Compare this to Daisy, who started investing at 35. She invests the same INR 3,000 and continues till retirement, meaning for 30 years. Despite continuous fresh investments for a longer tenure, Daisy ends up with INR 67.8 lakh only.

This is the power of compounding. It assures that with small but early and disciplined investments, investors can build a hefty corpus. Therefore, in this blog, we will decode why investing early is important, rather more crucial than investing heavily.

Small Steps, Big Results: Why Starting Early Matters

Many people believe you need a hefty sum to start investing. Not true! You can start with small, regular investments and gradually increase them as your income grows. The game-changer that makes this possible is the power of compounding, one of the key early investing benefits.

When this power of compounding is paired with early, disciplined investing, investors can expect long-term wealth creation without compromising on a fulfilled life. Let us take a closer look.

- The Compounding Effect: Adding interest to interest is compounding, meaning the interest rate is applied not only to your principal, but also to the accrued interest. Assume you make a monthly investment of INR 1,000 with a 12% yearly return. You receive INR 120 in interest for the first year. However, in the second year, you receive interest on both your principal and the INR 120 of interest you previously earned.

- Time is Your Ally: Your money has more time to grow through the process of compounding if you invest early. Your portfolio will witness the power of compounding over extended periods of time.

- Building a Habit: Starting small and investing regularly helps you develop a healthy financial habit. Rather than waiting for a long time for your income to grow, investors can start with a small contribution that fits their budget now, say INR 500 in mutual funds and INR 1000 in a high-yield FD.

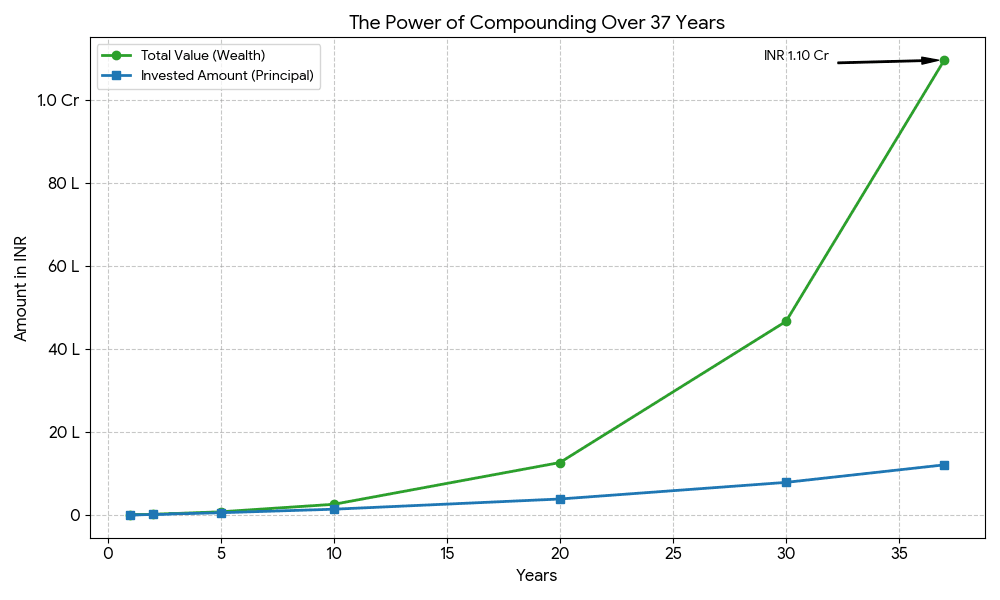

Let us take the compounding returns example of Ayusha. She wanted to start investing in 20s, at the age of 23. She began with INR 1,000 and increased it by just 5% every year.

Assuming a standard return of 12%, by the time she reached 60, her corpus stood at approximately INR 1.10 crore.

One of the major early investing benefits is that it makes long-term wealth creation possible even without a hefty investment. The key is disciplined and consistent investing. However, to understand why investing early is important, analysing the benefits of doing it is not enough; investors must also explore the cost of not doing it.

The Cost Of Delay: Why Starting Early Saves You

Time in the market is not just a cliche; it is among the most powerful variables in building wealth. The compounding returns an example of Priya and Sushil explores it the best.

Priya started investing at 25, while her friend Sushil started at 30, just 5 years later. Both invested INR 5,000 per month, and assuming a standard 12% return, let’s see what 5 years cost.

| Parameter | Priya (Early Starter) | Sushil (Late Starter) | Difference |

| Starting Age | 25 Years | 30 Years | 5 Years |

| Monthly Investment | INR 5000 | INR 5000 | - |

| Investment Duration | 30 Years | 25 Years | 5 Years |

| Total Amount Invested | INR 18,00,000 | INR 15,00,000 | INR 3,00,000 |

| Total Value with Returns | INR 1,76,49,569 | INR 94,88,175 | INR 81,61,394 |

So, just by investing 5 years late, Sushil lost about INR 81.61 Lakhs. Not just that, but late investors also face a greater inflationary impact.

Inflation Impact on Late Investors

Inflation erodes the real value of returns over time. Late investors lack the time horizon required for the power of compounding to overtake the effect of inflation. Moreover, late investors have to increase their investment corpus, compared to early investors, to get comparable long-term wealth creation. Besides compounding, a key reason for this is the lowered value of money.

For example, Roshan did not start investing in 20s.

He invested INR 5,000 per month from 30 years of age for 20 years. Assuming a return of 12%, the table below explains how inflation impacts investments of a late investor through a compounding returns example.

| Particulars | Details |

| Starting Age | 30 Years |

| Monthly Investment | INR 5,000 |

| Investment Duration | 20 Years |

| Total Amount Invested | INR 12,00,000 |

| Return of 12% without accounting for inflation | |

| Total Value with Returns | INR 49,95,740 |

| Return of 12% after accounting for 4% inflation | |

| Effective return (12% - 4%) | 8% |

| Total Value with Returns | INR 29,64,736 |

| Return if Roshan invested 5 years early from 30 years of age, while everything else remains constant | |

| Total value with returns, without accounting for inflation | INR 1,76,49,569 |

| Total value with returns, after accounting for inflation | INR 75,01,476 |

Therefore, just by investing 5 years early, Roshan could have earned INR 45.36 Lakhs more, lowering the impact of inflation. Let us now discuss why investing early is important by analysing the early investing benefits.

Risk And Advantages Of Starting Early

A key reason why investing early is important is closely linked to the heightened risk appetite of early investors. If you decide to start investing in 20s, not only will you get greater compounding, but you will also enjoy several risk benefits. Discussed below are some of them.

- Longer Time Horizon: Starting investments early allows investors a greater time horizon. This, in turn, helps ride out market volatility, accumulate greater compounding returns, and have a higher risk appetite in early years. A longer time horizon also instils greater flexibility to alter portfolio allocations for optimal investing.

- Riding the Market Volatility: While volatility is the characteristic trait of the market, it eases over time. History demonstrates that the stock market often trends upward over the long run, despite volatile periods in between. For instance, if you look at the chart of NIFTY 50 of the last 6 months, it exhibits volatility; however, when you zoom out and take a 5-Year perspective, the volatility smoothens out.

Investors might benefit from this general long-term growth trajectory if they start investing early and stick with it over time. You still have time for the market to rebound and your investments to perhaps realise their full potential, even if you incur temporary losses, during short-term volatility.

Therefore, young, early investors can invest in growth-oriented assets, like stocks. While these assets offer the potential for higher returns, they also experience short-term price fluctuations or volatility. However, a long-term perspective reduces this concern.

- Leveraging Your Risk Tolerance: Theoretically, investors at a younger age have higher risk tolerance because they have greater tenure at their disposal for long-term wealth creation. Through optimal portfolio allocation and diversification, early investors can prioritise higher growth assets compared to investors who are closer to retirement.

- Flexibility in Asset Allocation: Investors who are closer to retirement often have to prioritise capital preservation over growth. This does not apply to early investors. Therefore, such investors can prioritise growth assets, which have a higher risk profile, like equity or equity-oriented instruments.

- Human Capital as a Risk Cushion: Human capital indicates your future earning potential. For young professionals, career growth, rising skills and qualifications create an opportunity for rising income. This expanding source of income serves as a hedge against investment losses.

Early investors have a range of investment opportunities and assets fitting their objectives. These assets might not have been a viable option for late investments.

Investment Options For Early Investors

As a new investor, you have a variety of options to choose from. Here are some popular choices:

1. Stocks: Represent ownership in a company and offer potentially high returns but come with higher risk.

2. Mutual Funds: Pool money from many investors to buy a diversified portfolio of stocks, bonds, and other assets. This reduces risk compared to individual stocks.

3. Exchange-Traded Funds (ETFs): Similar to mutual funds but trade on stock exchanges like individual stocks. They offer low fees and a diversified way to invest in different sectors or markets.

4. Fixed Income Instruments: These provide steady returns with lower risk. Examples include:

- Bonds: Loans you make to governments or companies, earning interest payments over time. They offer predictable returns but may have lower growth potential than stocks.

- Fixed Deposits (FDs): Secure deposits with banks for a fixed term, offering guaranteed returns. Ideal for short-term goals or building an emergency fund.

5. Real Estate And Other Alternative Investments: While stocks, mutual funds, and ETFs are popular options, young investors can also consider alternative investments to diversify their portfolios further. Here are a few examples:

6. Real Estate: Investing in rental properties can generate passive income and potential long-term appreciation. However, real estate requires significant upfront capital and ongoing management responsibilities.

7. Commercial Real Estate via Co-ownership: For those interested in real estate but lacking a large sum for a whole property, consider co-owning a piece of commercial real estate. This approach allows you to collectively own Grade A commercial properties, like warehouses and offices in prime locations, alongside other investors.

8. Peer-to-Peer Lending: This involves lending money directly to individuals or businesses through online platforms. It can offer attractive returns but also carries the risk of borrower default.

9. Commodities: Investing in commodities like gold, oil, or agricultural products can provide a hedge against inflation. However, commodity prices can be volatile.

10. Securitised Debt Instruments (SDIs) : SEBI and RBI regulated fixed income opportunities offering better risk-adjusted returns than traditional investments. These investment options are rated by independent credit rating agencies and come with a security package.

Remember, the best investment choice depends on your individual goals and risk tolerance. Consider consulting a financial advisor for personalised guidance.

Strategies For Early Investing

Understanding why investing early is important is incomplete without exploring the strategies that can make early investing effective. Investors can follow the steps discussed below for optimal investing.

1. Define Your Goals: The first step is to finalise the goal an investor wants to achieve through a particular investment. The goal will determine the nature of suitable assets and the required time horizon.

2. Asset Allocation by Age Strategy Framework: The next important consideration is the age of the investor. As you get older, your asset allocation changes from high-growth stocks to conservative, income-focused assets like bonds, primarily due to the reduced risk tolerance. For instance, an investor in his 20s might allocate 80% of his portfolio to equity and equity-oriented assets, while at 60, the same investor can prioritise a 70% debt allocation.

3. Other Risk Factors: Besides age, investors must also consider other factors like the nature and amount of income, liabilities, liquidity requirements, etc., to gauge the risk level suitable for them.

4. Asset Allocation: Based on the determined risk level, investors can compare various assets and choose the allocation that fits them the most.

5. Automate Your Investments: To guarantee regular contributions to investment accounts, investors can set up automated transfers. In doing so, the desired funds will get automatically deducted on the instructed dates. It can help avoid missing instalments.

6. Review: Investors must periodically review their portfolio performance. This can reveal consistently underperforming assets and help ensure that the risk profile stays at a determined level. The investor can then take corrective actions, like liquidating high-risk or underperforming assets and directing the proceeds to other investments.

However, there are certain risks that investors must take into account.

Challenges And Considerations

Starting early does not eliminate all investment challenges. Here are some factors to be aware of:

1. Market Volatility: The stock market experiences ups and downs. Do not panic sell during downturns. Stay invested for the long term to benefit from market recovery.

2. Inflation: Inflation erodes the purchasing power of your money over time. Choose investments that have the potential to outpace inflation. You can consider investing in investment-grade corporate bonds to earn inflation-beating returns.

Strategies For Mitigating Challenges:

1. Diversification: Spread your investments across different asset classes to reduce risk from any single asset performing poorly.

2. Stay Invested for the Long Term: Do not make investment decisions based on short-term market fluctuations. Focus on your long-term goals and maintain a disciplined investment strategy.

Conclusion

Even with a limited corpus, investing early can help investors build a significant corpus. Rather than waiting to build long-term wealth, investing early can be a powerful financial move. The power of compounding, paired with access to a greater tenure, can boost returns and aid in long-term wealth creation. However, optimal diversification is key.

Platforms like Grip Invest, a leader in high-yield investment opportunities, can be a helpful starting point.

FAQs On Early Investing

1. What Type of Investment Has the Highest Long-Term Growth?

Stocks typically offer the highest long-term growth. They are volatile but tend to perform well over time. For instance, the average annual return of the S&P 500 over the last 90 years is around 10%.

2. What Does the Rule of 72 Tell You?

The rule of 72 is a simple way to estimate how long an investment will take to double at a fixed annual rate of interest. Divide 72 by the annual interest rate. For example, if your investment earns 6% per year, it will double in about 12 years (72/6 = 12).

References:

1. NSE India, accessed from: https://www.nseindia.com/index-tracker/NIFTY%2050

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001