Clay Craft India IPO Review: Key Details And Risks

Clay Craft India IPO brings a ceramic tableware manufacturer to the NSE Emerge platform. The issue is a fully fresh issue.

The IPO closed recently, which makes the update relevant for readers tracking SME listings. The issue has also received strong subscription interest, but investors still need to read the numbers, Clay Craft India's business model and risks together.

The offer opened on 17 June 2026 and closed on 19 June 2026. The shares are expected to list on NSE Emerge on 24 June 2026. Since this is a fresh issue, the next important question is how the company plans to use the funds.

Object of the issue | Amount |

Capital expenditure for additional manufacturing facility at Manda, Rajasthan | INR 9,700.00 lakh |

Estimated total project cost for the Manda facility | INR 12,641.68 lakh |

Internal accruals or borrowings proposed for the project | INR 2,941.68 lakh |

General corporate purposes | Not to exceed 15% of gross proceeds or INR 10 crore, whichever is lower |

Source: Claycraft,1

This makes the IPO mainly a capacity expansion story. The company is not using the largest share of proceeds for debt repayment. That distinction matters because future returns will depend on how well the new facility is executed and utilised.

Clay Craft India: Company Overview

Clay Craft India was incorporated as a private limited entity on 31 October 1988 and converted into a public limited company in 2025. Its portfolio spans dinner sets, tea and coffee serving sets, mugs, tumblers, platters, bowls and tabletop accessories. As of 31 March 2026, it offered about 5,770 SKUs across its range.

The firm markets products under the Clay Craft and JCPL brands. It also provides design, development and production support for other buyers. This gives its operating model a mix of own-brand revenue and B2B supply.

Its main categories include dinner sets, tea and coffee serving sets, mugs, tumblers, vacuum bottles, platters, bowls, tabletop accessories and gift items.

The product mix shows where the business is most dependent:

Mugs and dinnerware together contributed 75.89% of FY26 sales. This gives the company scale in two core categories, but it also means product-level demand shifts can affect performance.

The sales channel mix is also important when talking about Clay Craft India company details:

Distributor-led sales form the backbone of the business. Modern retail, corporate and HoReCa add demand diversity, but exports remain small. This means the company is still largely linked to Indian consumption and domestic retail demand.

Industry Analysis: Clay Craft India’s Market Opportunity

The company operates in a market where demand is shaped by home consumption, gifting, hotels, restaurants and design-led retail.

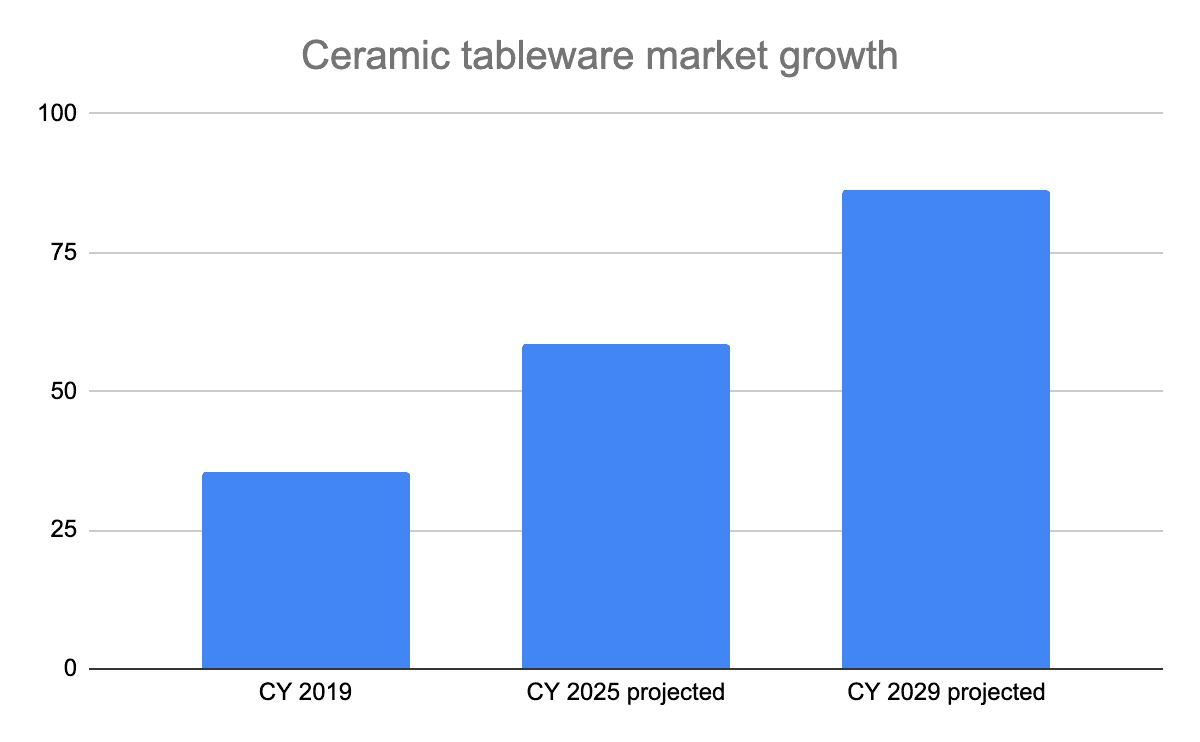

The Indian ceramic tableware market has been growing steadily. Research estimates show the market rising from INR 35.6 billion in CY 2019 to a projected INR 58.5 billion in CY 2025. It is expected to reach INR 86.2 billion by CY 2029.4

The projected CAGR from CY 2025 to CY 2029 is around 10%. The key drivers include:

- Urban housing growth,

- Higher spending on home products,

- Gifting occasions,

- Hospitality demand

- And a shift from plastic tableware towards ceramic and other durable materials.

For Clay Craft India, the opportunity is not only market growth. The sharper point is capacity. The IPO proceeds are meant to fund a new manufacturing facility at Manda, Rajasthan. If completed on schedule, the facility can help the company address demand across distributor, modern retail and institutional channels.

However, market growth alone does not guarantee operating success. Ceramic tableware remains competitive. The company also competes with organised brands, imports and smaller manufacturers. Design relevance, pricing and channel execution will matter as much as capacity.

Clay Craft India Financial Analysis

Clay Craft India's financials show rising revenue and improving profitability. Here is the three-year financial trend from the restated statements:

| Particulars (INR lakh) | FY24 | FY25 | FY26 |

| Revenue from operations | 14,542.55 | 15,194.22 | 17,988.67 |

| Total income | 14,698.82 | 15,443.70 | 18,456.86 |

| EBITDA | 2,864.95 | 3,539.06 | 4,195.94 |

| PAT | 1,350.20 | 2,075.74 | 2,701.49 |

| Total assets | 18,867.35 | 21,739.48 | 25,195.35 |

| Total debt | 4,679.54 | 4,774.55 | 4,997.74 |

Clay Craft India's revenue from operations grew 4.48% in FY25 and 18.39% in FY26. PAT moved faster, rising from INR 1,350.20 lakh in FY24 to INR 2,701.49 lakh in FY26.5

The trend shows a business with better scale in FY26. The next question in IPO analysis in India is whether margins can remain stable when the company expands capacity.

Profitability Metrics

The KPI table gives a clearer picture of operating quality:

| KPI | FY24 | FY25 | FY26 |

| EBITDA margin | 19.70% | 23.29% | 23.33% |

| PAT margin | 9.28% | 13.66% | 15.02% |

| RoE | 12.24% | 16.21% | 17.71% |

| RoCE | 14.42% | 16.69% | 18.26% |

Margins improved across the period. EBITDA margin moved from 19.70% in FY24 to 23.33% in FY26, while PAT margin rose to 15.02%. This indicates better operating leverage and cost absorption.

Balance Sheet Strength

The balance sheet shows rising assets and manageable leverage. Total assets increased to INR 25,195.35 lakh in FY26, while shareholders’ funds stood at INR 16,606.41 lakh.

The debt-equity ratio was 0.30 in FY26 compared with 0.34 in FY25. The current ratio stood at 2.21. These numbers suggest the company is not highly leveraged before the IPO.

However, inventories were INR 5,192.99 lakh and trade receivables were INR 1,730.77 lakh in FY26. For a manufacturing business with many SKUs and distributor-led sales, inventory planning and receivable collection will remain important.6

Key Risks To Consider Before Investing

The business has growth levers, but risks need careful review because this is an SME IPO with expansion-led fund utilisation.

1. Company-Specific Risks

Here are the main company-level risks investors should track:

The new facility is a key growth lever, but it also raises execution risk. Civil work is scheduled from April 2026 to January 2027, while plant and machinery installation is planned from November 2026 to February 2027.

2. Industry-Level Risks

The wider ceramic tableware market carries several external risks. These factors may influence Clay Craft India’s sales momentum, pricing power and operating efficiency.

3. Demand slowdown

Ceramic products are partly linked to discretionary consumption. Household buying may soften during weaker income cycles, while hotels, restaurants and catering businesses may delay fresh procurement.

4. Sector competition

The company operates in a crowded market with organised brands, imports and regional manufacturers. Cheaper alternatives may restrict pricing flexibility and make customer retention more difficult.

5. Regulatory changes

The production process depends on fuel, power, water and specialised inputs. Stricter pollution norms, factory approvals or operating conditions may raise compliance expenses.

6. Economic sensitivity

Sales are connected to retail demand, gifting occasions, hospitality activity and consumer confidence. A slower economic environment may reduce order flow across important channels.

7. Input cost movement

Important materials include ceramic colours, bentonite, kaolin, transfer paper and feldspar. Profitability may narrow if procurement prices rise faster than the company can revise selling prices

Building A Balanced Portfolio Beyond IPOs

Clay Craft India IPO offers exposure to India’s ceramic tableware market, backed by a fresh issue aimed at capacity expansion. The company has grown revenue, improved margins and reported better return ratios over FY24 to FY26.

Still, the investment view should remain balanced. Investors need to track facility execution, customer concentration, supplier dependence, working capital and post-listing liquidity. Subscription interest can support near-term attention, but fundamentals will decide the longer-term story.

IPO investing can form part of an equity portfolio, but it should not be the only route for wealth creation. Corporate bonds and fixed-income investments can provide stability, predictable cash flows and diversification alongside equity investments.

| Feature | IPOs (e.g., Clay Craft) | Corporate Bonds (9%–12.5%) | Bank FDs |

| Goal | Growth/price gains | Fixed income/higher yield | Capital preservation/steady income |

| Risk | High (execution, market) | Moderate (credit risk) | Low (bank credit risk) |

| Return predictability | Low | High (fixed coupons) | High (fixed interest) |

| Liquidity | Variable (post-listing) | Moderate | High (premature withdrawal w/ penalty) |

| Time horizon | Medium–long | Medium | Short–medium |

| Key checks | Execution, customer/supplier concentration, working capital | Issuer credit, covenants, tenor | Bank type, rate, premature rules |

To diversify beyond IPOs, investors can explore regulated fixed-income opportunities such as corporate bonds, government bonds on Grip Invest and access 9% to 12.5% fixed returns.

FAQs On Clay Craft India IPO

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001