Zero-Coupon Bonds Explained: How They Work And Who Should Invest

Most bonds are known for their regular interest payouts, but a zero coupon bond works differently. Unlike traditional bonds, these instruments do not provide periodic interest payments. Instead, they are issued at a deep discount to their face value, and the investor receives the full face value at maturity. The difference between the purchase price and redemption value becomes the investor’s return, making them a unique way to earn predictable, fixed income without recurring coupons.

In India, zero coupon bonds are often used by long-term investors who want to lock in returns with minimal reinvestment risk. Since they eliminate the uncertainty of fluctuating interest payments, they can be useful for goals like retirement planning, children’s education, or wealth creation over a fixed horizon. However, they also come with their own risks and tax implications, which every investor should understand before adding them to their portfolio.

Introduction To Zero Coupon Bonds

Definition And How They Differ From Regular Bonds

A zero coupon bond is a debt security that does not pay periodic interest (coupon) payments. Instead, investors purchase these bonds at a price lower than their face value and receive the full face value upon maturity. These fixed maturity bonds stand in stark contrast to regular bonds, which pay interest at fixed intervals throughout their lifetime.

For example, a regular 10-year government bond might pay 7% interest annually until maturity, when you receive your principal back. A zero coupon bond India offering the same returns would simply be priced at a discount that reflects the compound interest over that same period.

Why They Are Called “Deep Discount Bonds”

These instruments earn the name deep discount bonds because they’re sold at a significant discount to their face value. The deeper the discount, the longer the maturity period typically is.

In the Indian long-term fixed income market, these bonds first gained popularity when issued by the Industrial Development Bank of India (IDBI) in 19921. The bonds were offered at INR 2,700 and promised a face value of INR 1 lakh after 25 years, which is a deep discount of nearly 97%.

How Zero Coupon Bonds Work

No periodic interest, sold at a discount, redeemed at face value

When you purchase a zero coupon bond, you pay a price significantly below its face value. This discount is the interest you would have received if it were a regular coupon-bearing bond, but compressed into the initial price rather than distributed over time.

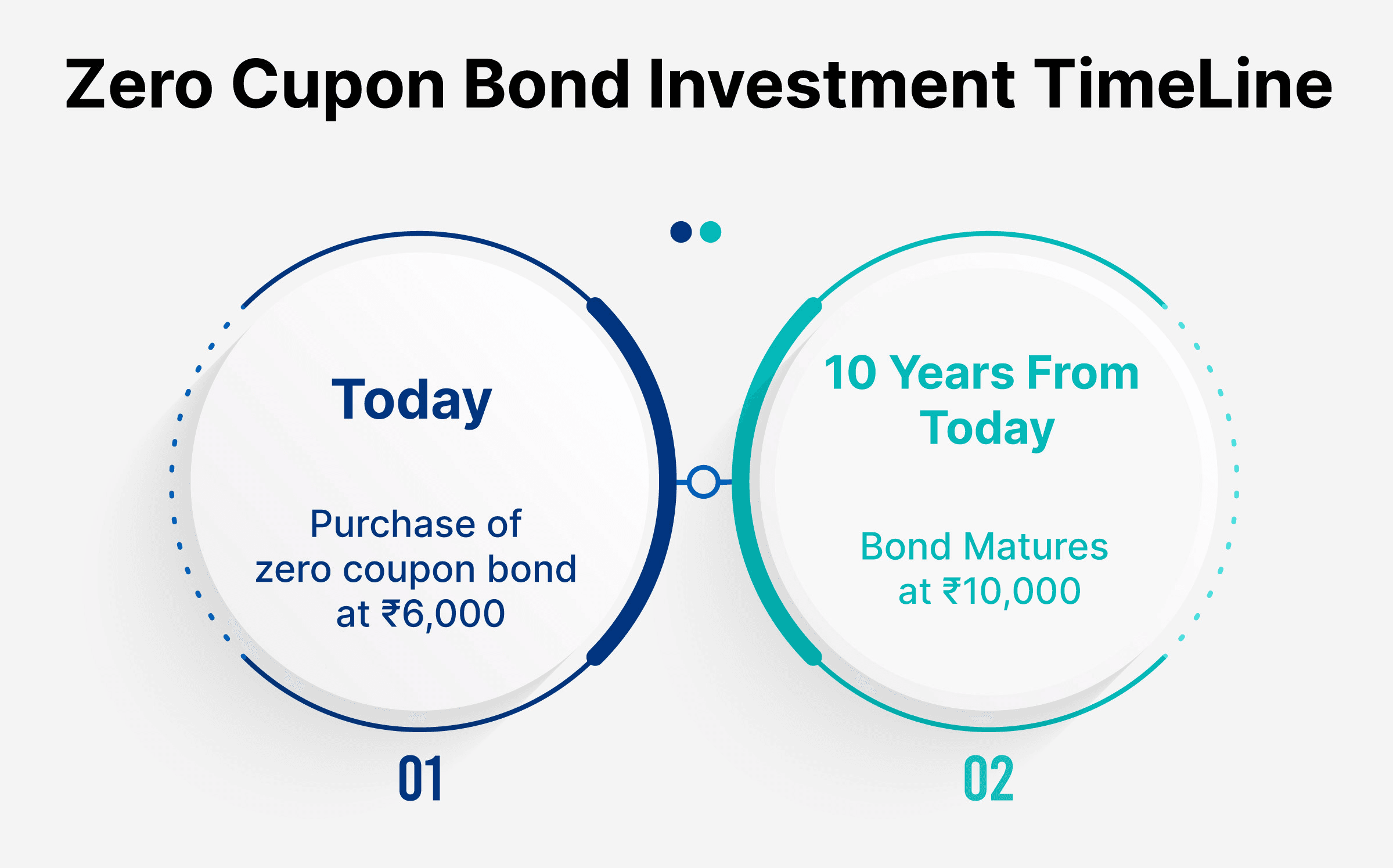

A 10-year zero coupon bond with a face value of INR 10,000 might be sold at INR 6,000 today. The INR 4,000 difference represents your total interest earnings, which you receive all at once when the bond matures, rather than in incremental payments.

The implied yield in this example comes around 5.2% compounded annually, the rate at which INR 6,000 grows to INR 10,000 over a decade. This yield-to-maturity becomes fixed at the time of purchase, providing investors with certainty about their returns regardless of market fluctuations.

Read: What Are Corporate Bonds: Meaning, Benefits, And How To Invest?

Advantages Of Zero Coupon Bonds

1. Fixed Maturity Value

The most compelling advantage of zero coupon bonds is their predictable outcome. At the time of purchase, an investor knows with certainty what amount they will receive at maturity. This fixed terminal value makes these bonds particularly suitable for financial planning where a specific sum is needed at a future date.

2. Good For Long-Term Goals

The structure of long-term bonds India of the zero-coupon variety makes them particularly well-suited for long-term goals. For retirement planning, these bonds offer a way to lock in returns decades in advance. A 30-year-old investor might purchase zero coupon bonds maturing in 30 years, creating a guaranteed retirement nest egg component without needing to monitor or manage ongoing interest payments.

Similarly, for children’s education funding, parents can match bond maturities to anticipated education expenses. This forced discipline helps investors stay committed to their long-term objectives.

For investors seeking greater stability and risk-adjusted returns, diversifying across different types of fixed-income products, including zero coupon bonds, regular coupon bonds, and securitised debt instruments (SDIs)—is essential. Platforms like Grip Invest curate diverse fixed-income portfolios, allowing individuals to balance liquidity, yield, and risk across bond types and issuer categories

Disadvantages Of Zero Coupon Bonds

No Regular Income Stream

Zero coupon bonds provide no cash flow until maturity, making them unsuitable for retirees or others dependent on investment income for living expenses.

The lack of interim payments also means investors miss opportunities to benefit from potential interest rate increases over the bond’s lifetime. Unlike floating-rate securities that adjust payments as rates rise, zero coupon bonds lock in the implied yield at purchase.

Sensitive To Interest Rate Changes

Zero coupon bonds have heightened price sensitivity to interest rate fluctuations. Because all the return is concentrated at maturity rather than distributed through interim payments, these bonds typically have higher duration than coupon-bearing equivalents.

This sensitivity means that when market interest rates rise, zero coupon bond prices fall more dramatically than traditional bonds. The price volatility is particularly significant for investors who may need to sell before maturity.

Read: Behavioural Finance In India: Why Your Mindset Matters More Than The Market

How Zero-Coupon Bonds Are Priced?

A zero bond does not pay any yearly interest. So instead of getting the interest every year, the person can buy zero bonds at a lower price and receive the full amount at maturity. The price will be decided by Face Value, i.e how much money one will get at the end, with how many years are left until the maturity, and the rate of return investors expect. The longer the time and the higher the expected return, the lower the price of the bond today.

Simple Formula

Price = Face Value ÷ (1 + Interest Rate)^Number of Years

- Price: The current market price.

- Face Value: The total amount paid at maturity.

- Yield: The annual interest rate or required rate of return.

- Years: Time remaining to maturity.

Taxation Treatment: Accrual vs Maturity Tax Impact

The difference between the purchase price and the maturity value is the profit earned from any zero-coupon bond, and since these bonds are issued at a discount and redeemed at the full value, that difference becomes the taxable gain for the person investing in zero-coupon bonds.

If these bonds are held for More Than 12 Months

The profit is treated as Long-Term Capital Gains (LTCG) and is generally taxed at 12.5% without indexation (for listed bonds, as per current tax rules).

If these bonds were Sold Within 12 Months

The profit is treated as Short-Term Capital Gains (STCG) and is taxed according to the investor’s applicable income tax slab.

Accrual vs Maturity Taxation

Tax at Maturity (Common Case)

Tax is paid when the bond matures or when investors sell it in the secondary market. The entire gain is taxed in that financial year.

Accrual Taxation (In Some Cases)

In certain situations, the “implied interest” may be taxed annually, even though no actual cash is received during the holding period. This spreads the tax burden over the years but creates yearly tax liability.

Zero-Coupon Bonds Vs Fixed Deposits

| Feature | Zero-Coupon Bonds | Fixed Deposits |

| Interest Payout | No Periodic Payout | Monthly/Quarterly |

| Returns | Locked in at Purchase | Fixed Rate Declared |

| Taxation | Accrual or capital gains-based | Interest taxed annually |

| Liquidity | Tradable | Premature withdrawal penalty |

| Risk Level | Depends on the issuer | Low (especially PSU/private banks) |

| Reinvestment Risk | None | Present |

| Category | Fixed-income investments in India | Fixed-income investments in India |

Liquidity Risks In The Secondary Market

Liquidity risk simply means how easy or difficult it is for a person to sell their bond before maturity. Zero-coupon bonds are harder to sell in the secondary market because not many people trade them. Some Liquidity Risks in the Secondary Market.

- Low Trading Volume & Depth: These bonds usually have fewer buyers and sellers in the market, which makes selling difficult.

- Price Fluctuation Risk: Bond prices can drop sharply when interest rates rise in the market.

- Higher Risk in Corporate Bonds: Corporate zero-coupon bonds may have more liquidity and credit risk than government-issued ones.

- High Price Volatility: The difference between the buying price and selling price can be large, and one can face a loss.

- Risk of Selling at a Loss: If the investor needs money urgently, they may have to sell at a lower price.

Should You Invest In Zero Coupon Bonds?

Best-Suited Investor Profiles

They suit investors with:

- Defined future financial obligations with specific timing

- Long investment horizons matching bond maturities

- Sufficient alternative income sources during the bond’s term

- Conservative risk tolerance seeking predictable outcomes

How Grip Invest Makes Access Easier

Traditionally, accessing quality bond investment India opportunities has been challenging for individual investors, with high minimum investments and limited secondary market liquidity. Platforms like Grip Invest have democratised access to fixed income securities by:

- Lowering minimum investment thresholds

- Providing curated selections of quality issuers

- Offering simplified digital purchase processes

- Creating more efficient secondary market opportunities

- Providing transparent information about risks and returns

Additionally, Grip Invest offers innovative fixed income options such as baskets blending zero-coupon, high-yield, and SDIs, further enhancing diversification benefits and income stability for investors

Read: Trump’s 200% Pharma Tariff: Impact On Indian Pharma Exports And Investors

Conclusion

Zero coupon bonds offer a simple approach to fixed-income investing that reduces reinvestment risk. Their structure makes them particularly valuable for matching specific long-term goals.To build a resilient and goal-oriented investment strategy, consider a mix of zero coupon bonds along with other fixed-income products like secured bonds and SDIs available on modern platforms such as Grip Invest. This approach can reduce the risk from any single security type and optimize for both growth and predictability

FAQs On Zero Coupon Bonds

1. Are zero coupon bonds safe in India?

Yes, zero coupon bonds can be considered safe in India. However, they still carry risks such as lack of regular income and high sensitivity to interest rate.

2. How is income from zero coupon bonds taxed?

Zero coupon bond taxation depends on the holding period and whether they are notified or not. In case of notified bonds if held for more than 12 months, the interest income attracts long term capital gains tax of 12.50%. Interest income from Non-notified zero coupon bonds are treated as Income From Other Sources.

3. Who should invest in zero coupon bonds?

Long-term investors who don't need regular income and have specific future financial goals can invest in these bonds. .

4. What is the maturity value calculation?

Maturity value equals the face value of the bond. Total return = Face value minus purchase price.

5. Are zero-coupon bonds better than FDs?

If the investor is looking for long-term growth and higher tax brackets (20%+), then they can opt for zero-coupon bonds, but for liquidity and more security, they should choose an FD.

6. Can retail investors buy zero-coupon bonds?

Yes, retail investors can buy listed zero-coupon bonds or government-issued deep-discount bonds through exchanges or investment platforms.

References:

1. Deccan Herald, accessed from: https://www.deccanherald.com/business/idbi-pay-interest-bonds-fm-2551545

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001