1 Crore FD Interest Per Month: How Much Income Can You Earn?

Fixed Deposits have been a reliable financial tool for decades. People often think that risk-averse investors prefer it more than the other categories. While the assumption does hold some water, the reality is a bit deeper. Investors often choose FDs because they are safe and extremely simple to understand.

Investors turn to FD when they need a reliable, predictable tool, usually because they are about to make a significant investment, such as INR 1 crore. Once such a large amount is invested, an investor often seeks a fixed monthly income, as it is tied to long-term goals such as retirement.

In fact, what 1 crore FD interest per month would fetch is a common question that investors often ask.

How FD Interest Is Calculated

Before understanding the FD interest calculation India, let's quickly understand what a fixed deposit is. A fixed deposit is a financial instrument in which an investor deposits a lump sum with a bank or financial institution for a specific tenure at a fixed interest rate. The money remains deposited with the bank/financial institution, and the investors earn interest at the predetermined rate for the specified tenure.

Monthly payout vs cumulative FD

Based on when interest income is collected by investors, FDs can be divided into two types: monthly and cumulative.

- Under the Monthly Payout FD, interest is credited to the investor each month. This structure is great for individuals who are looking for a consistent fixed deposit monthly income.

- Cumulative is the opposite of monthly. Under it, the interest income is not paid to the investor monthly. Rather, it is added to the principal and paid at maturity. The benefit of doing so is that investors can earn higher total returns, but they have to give up regular monthly income.

Interest formula

Fixed Deposit Interest calculation is simple. It just multiplies the principal amount by the interest rate. Now, as the interest rate is usually "per anum", to calculate monthly income, the total annual interest is divided by 12. The calculation differs slightly for Cumulative FD because interest is not paid out every month. Instead, the interest is added back to the principal, and future interest is calculated on the increased amount. This process is called compounding.

Let's understand it with the help of a simple example:

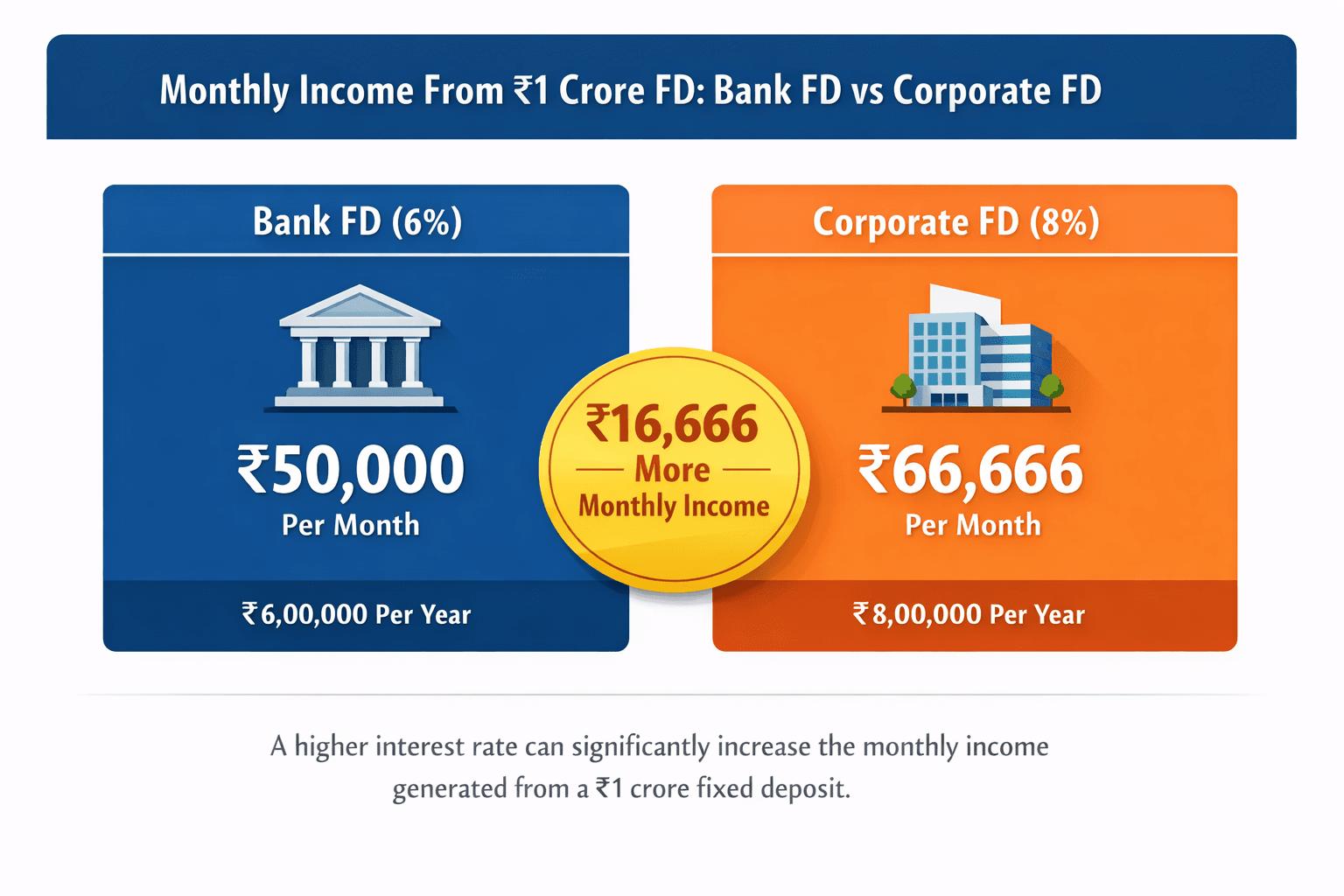

If you invest a principal amount of INR 1,00,00,000 at an interest rate of 6%

Your interest income under the Monthly Payout FD will be:

Annual Interest = INR 1,00,00,000 × 6% = INR 6,00,000

Monthly Interest = INR 6,00,000 ÷ 12 = INR 50,000

So, you receive INR 50,000 every month for the entire tenure, while the principal amount remains INR 1 crore.

Your interest income under the Cumulative Payout FD will be:

Year 1 Interest = INR 1,00,00,000 × 6% = INR 6,00,000

New amount after Year 1 = INR 1,06,00,000

Year 2 Interest = INR 1,06,00,000 × 6% = INR 6,36,000

New amount after Year 2 = INR 1,12,36,000

In this case, the interest continues to compound on the principal each year, and the total amount is received at maturity rather than in monthly payouts.

While the calculation is simple, it can be time-consuming and a bit overwhelming as well. If you feel the same, you can use a 1 crore FD interest calculator online to quickly estimate returns.

Risks Of Relying Only On FDs for Income

Fixed deposits are often considered a relatively safe investment option. However, no financial product is entirely risk-free. There are potential risks associated with fixed deposits that should be considered before making any investment, especially for people who rely solely on FDs.

1. Taxation on interest

The first thing to consider is that the interest earned from fixed deposits is taxable. While the tax on interest from 1 crore FD depends on the investor’s income tax slab, as a rule of thumb, the higher the income, the higher the tax.

As a result, it is often observed that the actual income received after tax is significantly lower than the calculated interest amount. Therefore, investors should consider this factor when estimating their monthly income from 1 crore FD. For exact calculations, please contact your tax advisor.

2. Inflation risk

Another major consideration is the inflation risk. Inflation can reduce the purchasing power of fixed returns over time. Even if an FD generates stable monthly income, rising prices may reduce the real value of those earnings. As a result, investors who rely solely on fixed deposits might find their income does not keep pace with rising living expenses.

What Is Corporate FD

Corporate fixed deposits are what they sound like. They are fixed deposits issued by corporations, such as companies or financial institutions, instead of banks. Since deposits are not offered by banks, investors consider factors such as the company’s financial stability and credit rating before investing.

What sets them apart from bank FDs is that they usually offer higher interest rates than regular bank deposits. This can lead to better returns for investors seeking higher fixed income. Some key benefits of investing in Corporate FDs include:

- Potentially higher interest rates than standard bank FDs

- Multiple interest payout options, such as monthly or cumulative

- Flexible investment tenures

You can refer to the Grip Invest platform to find out more about corporate FDs and how you can include them in your portfolio.

Monthly Interest On INR 1 Crore FD

The 1 crore FD interest per month depends on several factors, such as the type of institution offering the FD and the investor's age. For example, traditional bank fixed deposits usually offer lower rates compared to corporate FDs. Furthermore, senior citizens are often eligible for slightly higher interest rates than regular investors.

Here is a simplified comparison showing how interest rates can affect fixed deposit monthly income on a INR 1 Crore investment.

| FD Type | Interest Rate | Monthly Interest | Annual Interest |

| Regular Bank FD | 6% | INR 50,000 | INR 6,00,000 |

| Senior Citizen Bank FD | 7% | INR 58,333 | INR 7,00,000 |

| Corporate FD | 8% | INR 66,666 | INR 8,00,000 |

This interest rate difference can significantly impact the total income earned from the same investment amount. Given the higher return potential, it is a good idea to explore corporate fixed deposit opportunities on investment platforms like Grip Invest, where fixed-income options may offer better yields than standard bank FDs.

This interest rate difference can significantly impact the total income earned from the same investment amount. Given the higher return potential, it is a good idea to explore corporate fixed deposit opportunities on investment platforms like Grip Invest, where fixed-income options may offer better yields than standard bank FDs.

Diversifying Monthly Income Investments

While fixed deposits are great financial tools, especially when your goal is to generate a reliable income, it is never a good idea to depend on them solely. To ensure you have a comprehensive portfolio, diversify by including other income-generating instruments that provide periodic returns.

Doing so will allow you to balance stability with potentially higher returns while still maintaining predictable income streams. Having your investments spread across different fixed-income opportunities, you will have a more balanced strategy for long-term monthly income planning.

FAQs

1. How much interest does INR 1 crore FD generate monthly?

The 1 crore FD interest per month depends on the interest rate. For example, at 6% interest, the monthly income is about INR 50,000, while at 8% interest it increases to roughly INR 66,666.

2. Is FD interest taxable?

Yes. Interest earned from fixed deposits is taxable according to the investor’s income tax slab. The tax on interest from 1 crore FD can reduce the final income received.

3. Which banks give the highest FD rates?

Different banks offer varying rates depending on tenure and deposit schemes. Institutions such as SBI, HDFC, and ICICI provide fixed deposits with multiple payout options, and the rates may change periodically.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001