Bond Investing During War: Safe Haven Or Inflation Risk?

As new tensions rise in the Middle East, while past conflicts like the Russia-Ukraine war persist, the rising geopolitical crisis might push investors towards safe-haven assets. Although safe-haven assets like gold are heavily discussed as a hedge, an aspect that is often overlooked is the trend of bond investing in a geopolitical crisis.

These fixed-income asset categories, particularly the high-quality or government-backed bonds, often offer the portfolio stability that investors crave during uncertainties, causing rallies, and further solidifying the role of safe-haven bonds.

For instance, even in the U.S., investors flock towards assets like the U.S. Treasuries or equivalent government bonds during turmoil, boosting the U.S. Treasury bonds war demand. Since investors prioritise capital preservation over growth during turmoil, bond investing during war heightens as they offer a low-risk, fixed-income alternative for a hedge.

Even the central bank takes various steps to boost the rally. However, not all bonds can offer this hedge. Therefore, this blog unpacks the nuances of bond investing in a geopolitical crisis to help with planned investing.

Flight To Safety Explained

Investors participate in a "flight to safety" during times of conflict by accumulating government bonds, which are deemed to be secure due to their sovereign support or high credit rating and minimal default risk. Furthermore, bond prices move inversely to yields. Therefore, as investors flock to bonds, their market value rises, and the yield of existing bonds diminishes. Discussed here is a step-by-step take on investor interaction with bonds during turmoil, bond price trend, and the yield curve in a geopolitical crisis.

- Demand Spike Mechanism: Conflicts and tensions create uncertainties, prompting global sell-offs in global equities and other high-risk, market-linked assets. In such a scenario, investors pivot to fixed-income, low-risk assets, like highly-rated bonds or government securities. As demands rise, the market value of these bonds increases. Thus, as growth assets like equities witness a downturn, fixed-income bonds record growth.

- Reaction of Yield: Since yields represent the return on current prices, increased demand outpaces supply, driving up prices and lowering yields. Therefore, when the market value of bonds increases, their yield tends to fall. Similarly, when yield increases, the market value tends to diminish.

Although yields might diminish, the rising market value of bonds creates an opportunity for a greater capital gain. Therefore, despite a lower yield, bonds remain an attractive opportunity for investors amid a crisis due to the capital gain prospects. However, this bond rally often faces a counter from inflationary pressure.

Inflation Vs Bond Rally Conflict

Inflation-linked bonds face war inflation counter-effects that might hinder their rally. It occurs primarily when oil price hikes are caused by tensions, resulting in an inflationary pressure that typically counters a safe-haven bond rally. Such a scenario creates a dichotomy between falling yields from safety demand and rising yields from inflation fears, resulting in a dilemma for the Central Banks. Detailed below is a nuanced explainer on this.

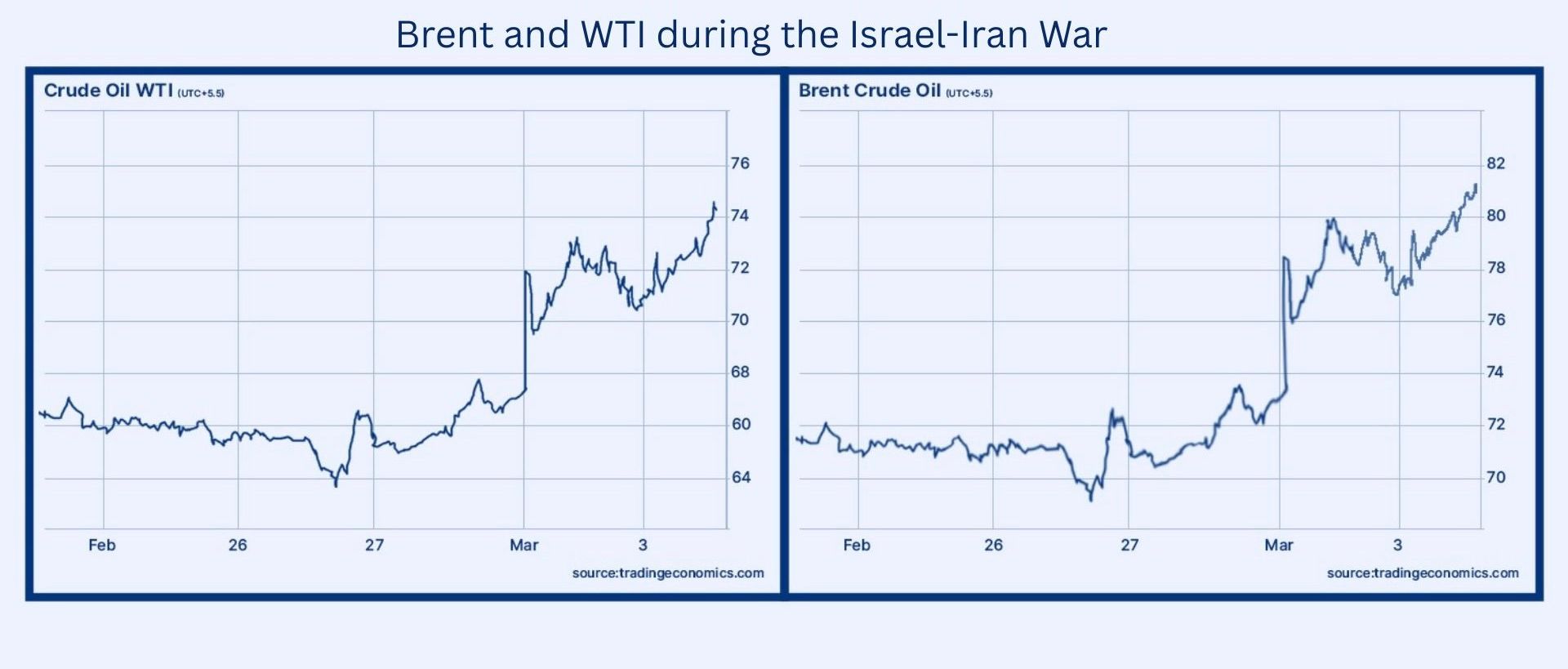

- Oil Price Spikes, Inflation, and Impact on Bonds: Wars in oil-producing countries in the Middle East endanger oil supplies and supply chains. It increases oil prices, which creates inflationary trends. Elevated inflation pressure triggers investor demands for a higher yield on new bonds to combat declining purchasing power, thereby prompting a decline in the market value of bonds. For instance, on 3 March 2026, Brent rose over USD 3, as the Brent Crude Futures increased more than 4.1% to hit USD 80.89 a barrel1. Even the U.S. West Texas Intermediate crude grew 3.6% to reach USD 73.38 per barrel. Furthermore, the contract had reached its highest level since June 2025. The graph below illustrates the movement of Brent and WTI over the past week.

- Central Bank Reaction: Amid this dichotomy, the central bank is pushed into a dilemma. It can either cut repo rates to support growth and boost bond rallies, or it can increase the rates to combat inflationary pressures. In such a situation, the decision of the RBI on the repo rate cut in a war scenario is based on a holistic analysis of the current situation and priorities to balance growth and stability amid volatile situations.

For instance, let us analyse the government bonds war rally in India. Amid the latest Middle East crisis, the government bonds in India traded low as crude prices skyrocketed2. The benchmark 6.48% 2035 bond yield increased to 6.6894% after concluding its previous trading session at 6.6601%. Such a movement of G-Sec yields during Middle East tensions reflects the relation between bond movements and crude rates.

While this phenomenon of inflation and bond rally dichotomy is macroeconomic and managed by the Central Banks of different countries, it is beyond the control of individual investors. However, there are certain other trends that investors can analyse to make optimal portfolio decisions.

Credit Risk In Corporate Bonds

Some other key trends emerge as the bond market reacts to crisis investments. Let us take a brief look at them.

1. Corporate Bonds Spread Widening in Conflict: Corporate bond spreads (or credit spreads) reflect the gap in yield between a corporate bond and a risk-free government bond of comparable maturity. This spread serves as a risk premium, meaning the additional yield of a corporate bond is a payoff for the extra risk taken. A wider spread indicates a higher perceived risk, resulting in investors demanding more compensation for that risk. During conflict and geopolitical tension, bond spreads typically widen. Investors prefer low-risk, government bonds and highly rated assets, compared to riskier corporate bonds with low ratings. Therefore, during a conflict, not just any bond, but only highly-rated sovereign bonds incur flight to quality in war, as illustrated by this phenomenon of credit spreads geopolitics risk-off.

2. Emerging Market Bonds Crisis Premium: Bonds issued by developing countries or rapidly evolving sector companies form the emerging bond market. Investors of such bonds claim an extra yield to hold on to the emerging bonds, as such bonds have a greater risk profile compared to stable, highly rated bonds.

3. Yield Curve Inversion War Risk: If during uncertainty, short-term rates exceed long-term rates, it indicates high investor pessimism and recessionary trends. Economic contractions have historically been preceded by such inversions, which are motivated by concerns about recession, geopolitical unrest, or Central Bank policies.

4. High-Yield Risk: Bonds offering high interest do so due to their high risk profile. Amid rising economic volatility, such high-yield bonds might lose their appeal as investors prioritise stability over growth.

Therefore, either through rising market value of bonds that create a capital gain opportunity or through rising yield, bonds often offer an opportunity for hedging amid uncertainties. However, the dynamic nature of the market requires careful observation to make an optimal investment choice.

Let us now analyse the impact on the Indian bond market.

Indian Bond Market Impact

As the price of crude rose sharply post the crisis in the Middle East, the bond market in India witnessed a tumble. The benchmark 6.48% 2035 bond yield increased to 6.6894% after concluding its previous trading session at 6.6601%. On the other hand, the Reserve Bank of India (RBI) had bought bonds worth INR 28.15 billion as of 20 February 2026. The data about its operations in the last week, that is, the week amid the conflict, would be released on Friday, 6 March 2026. Therefore, it is still early to gauge the impact on the Indian bond market, as it is an ongoing conflict and the patterns are just starting to emerge. However, highly-rate bonds, like the AAA bonds can offer safe haven in India during war over the long-term, if the bond market remains positively stable.

Nevertheless, investors must employ optimal investment techniques like bond laddering or a duration extension strategy in a crisis. Under the bond laddering technique, an investor invests in different bonds with varying maturity dates, while the duration extension strategy allows investors to increase the average duration of the entire bond holding by investing in longer-maturity securities. Employing both duration extension and bond laddering during volatility helps diversify tenures to reduce the impact of adverse yield movements in a particular tenure. Furthermore, a strategy called floating rate notes give conflict hedge by suggesting investment in debt assets of varying interest rates to mitigate the impact.

Grip offers a range of fixed-income securities, like corporate bonds, high-yield FDs, debt mutual funds and more, with up to 12.5% YTM. Visit Grip Invest Today!

FAQs

1. Why do bonds often perform well during geopolitical crises?

During geopolitical conflicts, investors usually shift from risky assets like equities to safer investments such as government bonds. This “flight to safety” increases demand for bonds, pushing their prices up and yields down.

2. How does inflation during war affect bond investments?

Wars can push commodity prices, especially oil, higher, leading to inflation. Higher inflation reduces the real return from bonds, which may cause investors to demand higher yields and weaken bond prices.

3. Are corporate bonds safe during geopolitical uncertainty?

Not all corporate bonds are equally safe. During crises, investors generally prefer highly rated corporate bonds, while lower-rated bonds may face widening credit spreads as perceived risk increases.

4. What strategies can investors use to manage bond risk during crises?

Investors can use strategies such as bond laddering, investing in different maturities, extending duration selectively, or choosing floating-rate instruments to reduce the impact of interest rate volatility.

References:

1. Reuters, accessed from: https://www.reuters.com/business/energy/oil-rises-expanding-us-israeli-conflict-with-iran-elevates-supply-risks-2026-03-03/

2. Live mint, accessed from:

https://www.livemint.com/market/bonds/usisraeliran-war-indian-bond-yields-spike-as-middle-east-conflict-lift-crude-oil-prices-11772436601448.html

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001