Car Loan Interest Rate in India 2026: EMI, Bank Rates & How to Reduce Costs

While monthly payments are important, car loan interest rates impact your financing more than just by the monthly payments alone. When you understand the interest rate on a car loan, you can get a better deal when you get out on the road!

The high price of purchasing a vehicle has limited many people's ability to become car owners because of the high initial payment required.

You need to come up with this large amount to purchase outright, or you can provide several payments over time via a car loan interest rate.

It is important to concentrate on the interest rate charged rather than the car loan EMI that is due instead when assessing a finance offer.

Long-term loans often have lower EMIs. However, you generally end up paying a larger amount of total interest on long-term loans.

A small change in the car loan interest rate can save consumers thousands of dollars over the life of the loan.

This guide will assist you in understanding all of the different types of car loan rates available in India.

Current Car Loan Interest Rates In India

Car loan interest rates from banks are generally lower than what can be found through the NBFC due to lower rates and faster approval for loans from the NBFC.

The best rate for a new car can typically be found in the 8% to 10% range, while the best rate on a used car can typically be found in the 10% to 15% range, due to the increased risk associated with used cars.

The lowest car loan interest rates in India will be found at some banks for a prime borrower and should begin to converge at approximately 7.5% by 2026. Electric vehicles continue to be moderately priced in comparison with gasoline-engine vehicles, given the available green incentives.

However, the total cost of an electric vehicle will generally be less than the total cost of the comparable gasoline-engine vehicle.

Here is a table of top banks and their car loan interest rates for new cars:

| Bank | Interest Rate (p.a.) | Car Loan Processing Fee By Banks |

| SBI | 8.70% - 9.85% | Up to INR 1,500 + GST |

| HDFC Bank | 8.15% onwards | 0.5% (INR 3,500-INR 8,000) |

| ICICI Bank | 8.50% onwards | 0.5% of loan amount |

| Bank of Baroda | 8.50% - 9.35% | INR 1,500-INR 2,000 + GST |

| Union Bank | 7.50% - 9.45% | INR 1,000 + GST |

Source Money View1

The interest rates on car loans fluctuate based on the borrower's profile. Check out online car loan interest rate comparisons from banks to get your own best insurance quote. New vs used car loan interest rate differences (when looking at used) generally range from 2 to 4% higher than new.

Also Read: TD Interest Rates 2026

Factors Affecting Car Loan Interest Rate

1. Credit scores have the greatest impact on automotive loan interest rate decisions. Banks typically will give the lowest automotive loan interest rate available to a borrower with a credit score of 750 or higher.

2. The length of the loan is also a factor when determining automotive loan interest rates. Generally, shorter-length automotive loans have lower total automotive loan interest amounts, but will have higher monthly automotive loan payments.

3. A greater down payment will reduce the amount of loan that will have to be borrowed for a vehicle, thereby reducing the overall amount of automotive loan interest that the borrower will pay due to the lower total amount of the loan.

4. The type of vehicle that is being acquired may also affect the loan interest rate. For instance, new and electric vehicles typically have a lower interest rate than used vehicles.

5. Employment stability and income will also have an effect on the interest rates for auto loans. CIBIL Score is an important eligibility requirement for automobile loans, and borrowers should strive for a score of 730 or greater.

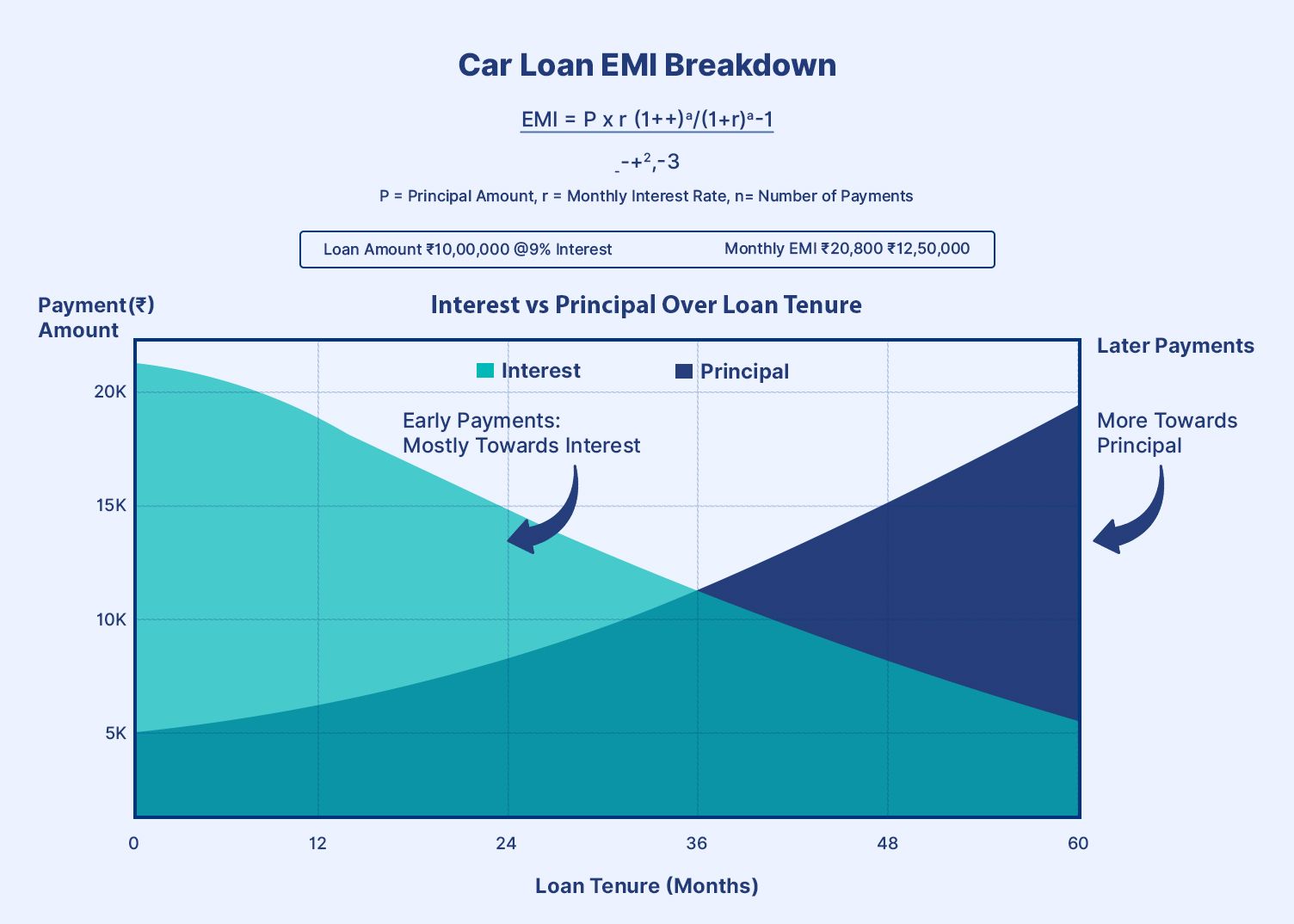

How To Calculate Car Loan EMI

The formula used to determine the equated monthly installment (EMI) for your auto loan is as follows: EMI = P x r x (1 + r)n/[(1 + r)n – 1], where P is the principal amount of the loan, r is the monthly interest rate and n is the total number of payments (term in months).

Hypothetical Example

For example, if you have hypothetically borrowed INR 10 lakhs at a 9% interest rate and are paying it off over 5 years (60 months), your monthly car loan EMI would work out to be approximately INR 20,800, and your total loan repayment would be approximately INR 12.5 lakhs.

Tips To Get Lower Interest Rates

1. Improve your credit score well before you apply for an auto loan in India by paying your bills in a timely manner and reducing your total debt.

2. To find competitive rates like the SBI car loan interest rate or HDFC car loan interest rate, you can compare car loan lenders using a car loan interest rate comparison website.

3. When negotiating with a car dealership, try to negotiate the best deal on your car loan by using bundling options.

4. If you want a more predictable car loan EMI, a fixed rate may be preferable to a floating rate, as the fixed rate would remain constant, while the floating rate could fluctuate based on current market conditions.

5. Be aware of the car loan process fees that are charged by lenders, which generally range between 0.25 percent and 2 percent. You should also ask your lender to waive this charge.

6. Making a larger down payment can help you qualify for the best interest rate possible for your auto loan in India.

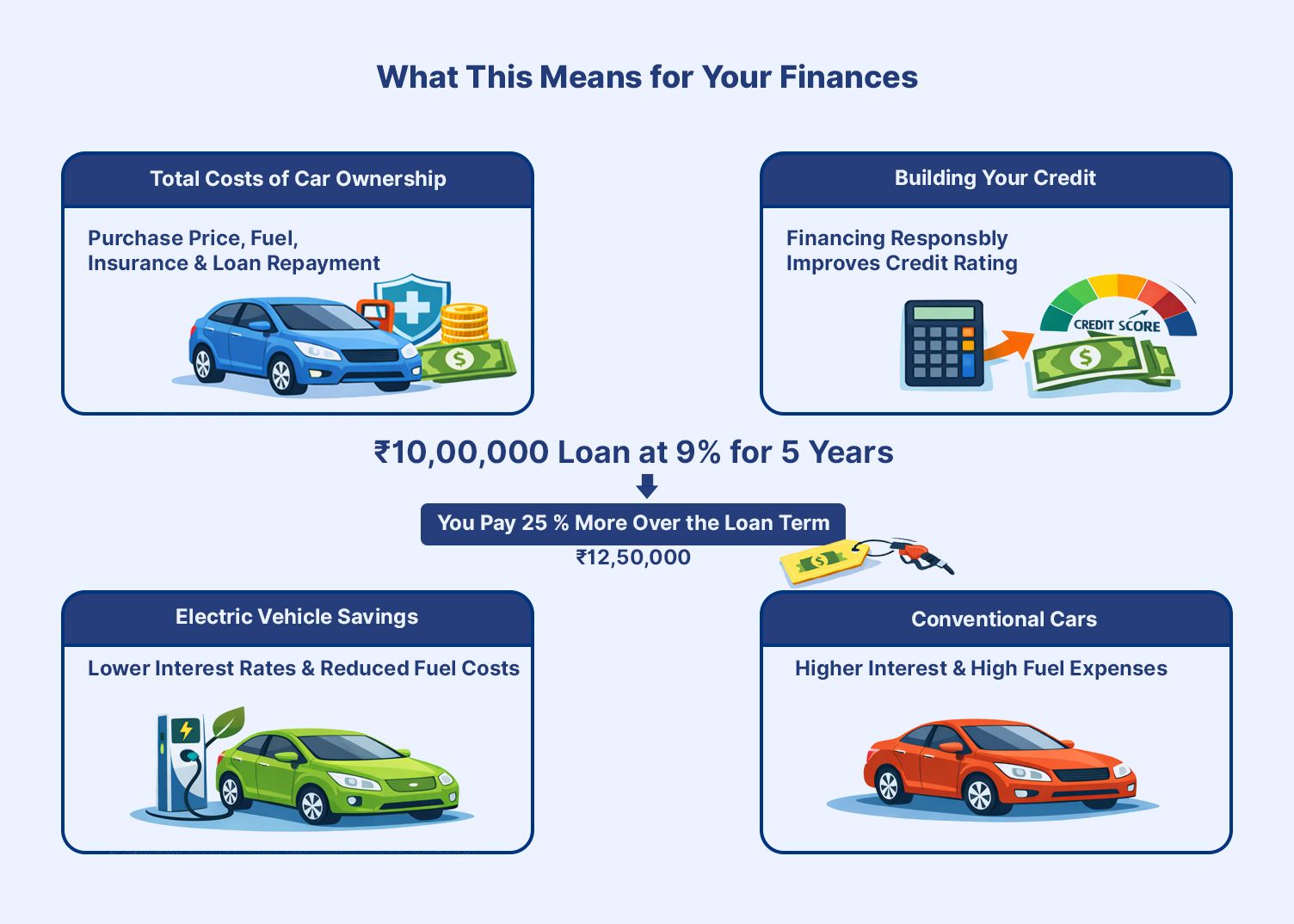

What This Means For Your Finances

The total cost you will incur to own a car will include the cost of purchasing your car, paying for fuel, paying for insurance, and completely repaying your loan. If you finance a INR 10,00,000 vehicle at 9% for 5 years, you will pay 25% more than you would at the end of the loan period, when compared to the original sticker price.

When deciding whether to finance your purchase or buy your car with cash, it is important to factor in how financing can allow you to build your credit rating, if done responsibly. For electric vehicles, financing will often result in a lower vehicle loan interest rate than financing other types of vehicles. In addition, you will be saving on gas or diesel purchases, which should make buying an electric car more financially attractive than purchasing a non-electric vehicle.

Make Your Money Work While You Repay

A car loan is a long-term financial commitment. While you manage your EMIs, your idle savings shouldn't sit still. Here are a few fixed-income options that generate predictable returns alongside your repayment plan:

| Instrument | Expected Returns | Liquidity | Risk Level |

| Corporate Bonds | 8%–12% p.a. | Medium (exchange-listed) | Low to Moderate |

| Corporate FDs | 8%–10% p.a. | Low (lock-in period) | Low to Moderate |

| Debt Mutual Funds | 6.5%–8.5% p.a. | High (T+1 redemption) | Low |

| Government Securities | 6.8%–7.5% p.a. | Medium | Very Low |

| Bank FDs | 6.5%–7.5% p.a. | Low (penalty on exit) | Very Low |

The key principle: if your car loan costs you 9% per annum, investing in instruments yielding 10%–11% means your portfolio is effectively subsidising your borrowing cost, reducing the real financial impact of the loan over its tenure.

Platforms like Grip Invest offer SEBI-regulated access to corporate bonds and fixed-income products, helping you build a stable return stream even while repaying a loan.

Conclusion

Car loan interest rates play a crucial role in determining the real cost of owning a vehicle. While EMIs may seem manageable, even a small difference in interest rates can significantly impact your total repayment over time. By understanding how rates work, comparing lenders, maintaining a strong credit score, and choosing the right loan structure, you can make a more cost-effective borrowing decision.

As you plan your finances, it is equally important to balance liabilities like loans with stable income-generating investments, platforms like Grip Invest can help you explore alternative investment opportunities to strengthen your overall financial strategy.

FAQs On Car Loan Interest Rates In India

References:

1. Money View, accessed from: https://moneyview.in/loan-insights/car-loan-interest-rate

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001