TD Interest Rates: Meaning, Types, Factors Affecting Returns, and TD vs FD Explained

The growing sophistication of the Indian investment landscape has led to the rise of varied assets that can cater to different investor needs.

However, often investors are either unaware of the choices available to them or mistakenly assume different assets to be synonymous due to their overlapping features. A prime example of this is a term deposit vs a fixed deposit.

Despite similarities, bank TD rates and meaning have key differences from those of FD. This blog primarily focuses on TD interest rates, along with their meaning to help efficient investor understanding.

What Are TD Interest Rates?

Primarily, a term deposit (TD) is a kind of deposit in which investors deposit for a fixed duration, called a term, at a predetermined interest rate. The defining aspect of this investment is that investors commit to leaving the principal untouched in return for the set term deposit interest rates.

Therefore, TDs are a broader concept that includes fixed deposits, recurring deposits, senior citizen deposits, etc.

A TD can be issued by banks, non-banking finance companies, small finance banks, post offices, etc. Think of it as a contract between the investor and the issuer, say a bank.

The steps below explain how it works.

1. Creation of deposits: Investors approach a bank and create a TD online or offline by choosing the deposit amount, tenure, payout option, etc. For instance, Mr K decides to make a TD of INR 5 lakhs for 3 years at a rate of 6% p.a.

2. Bank locks the fund: The bank maintains the deposit for the fixed tenure, meaning the investor cannot liquidate the principal, and use it to extend credit. In case the investor withdraws prematurely, penalties are levied.

3. TD interest rates accrue: If the investor chooses a cumulative FD, the interest is added back to the principal and compounded over time. In case non-cumulative interest is selected, the interest is paid out periodically at the chosen interval, i.e., monthly, quarterly, etc.

4. Maturity: At maturity, the principal, along with interest in the case of cumulative TD and only the principal in the case of non-cumulative TD, is credited to the linked savings account. If the investor had chosen auto-renewal during TD creation, at maturity, the TD will be renewed at the previous tenure and prevailing rate.

The popularity of safe investment TDs is due to their low risk profile. Unlike assets like equity, the principal in TD is not exposed to market volatility, and they deliver fixed interest returns. It can provide passive income or predictable growth.

How Banks Calculate TD Interest Rates?

The TD rates in India vary from one issuer to another, based on the distinct policy of the bank or other financial institution.

Discussed below are the factors that determine TD rates.

1. Deposit tenure: Most banks and institutions set rates based on tenure ranges. While the tenure-based interest varies, a common trend usually exists.

- Short-term tenures, ranging from a few days to a few months, have lower rates because the banks don’t have sufficient time to use the funds for long-term lending.

- Mid-term TDs have the highest term deposit rates because they deliver a balance between longer tenure, meeting funding needs, and risk.

- Risk increases with an increase in tenure, as the distant future is more unpredictable. Therefore, the rates often decline for very long tenure TDs.

2. Principal amount: TD returns are directly proportional to the principal amount. If the principal invested increases, the returns earned also rise.

3. Compounding frequency: Very short-term deposits, made for a few days, or non-cumulative deposits often carry simple interest, where interest is levied only on the principal. However, cumulative TDs and medium to long-term deposits carry compound interest, according to the formula below.

Amount = Principal (1 + Rate/Compounding Frequency) Compounding frequency x Tenure

The number of times interest is added to the principal annually, enabling investors to earn interest on interest that has already accrued, is known as compound frequency.

For example, if a TD is compounded quarterly, then compounding frequency will be 4. An increase in compounding frequency results in a higher effective yield for the same nominal rate.

4. Bank policies: The internal policies and constraints of the bank also determine its TD rate card. The table below highlights some of these parameters.

| Cost of funds | If demand for loans rises, and other methods of funding are more expensive compared to TDs, the banks may increase TD rates to attract more funds. |

| Risk considerations | The interest rate falls if the risk for the bank increases. This is why very long-term tenure often carries a lower rate than medium-term deposits. |

| Target customer segment | Banks can choose to offer unique rates to special customer segments. For example, senior citizen deposits carry a higher interest rate than regular deposits. |

Besides these bank-specific policies, other economic and macro factors also determine the fixed-term deposit returns.

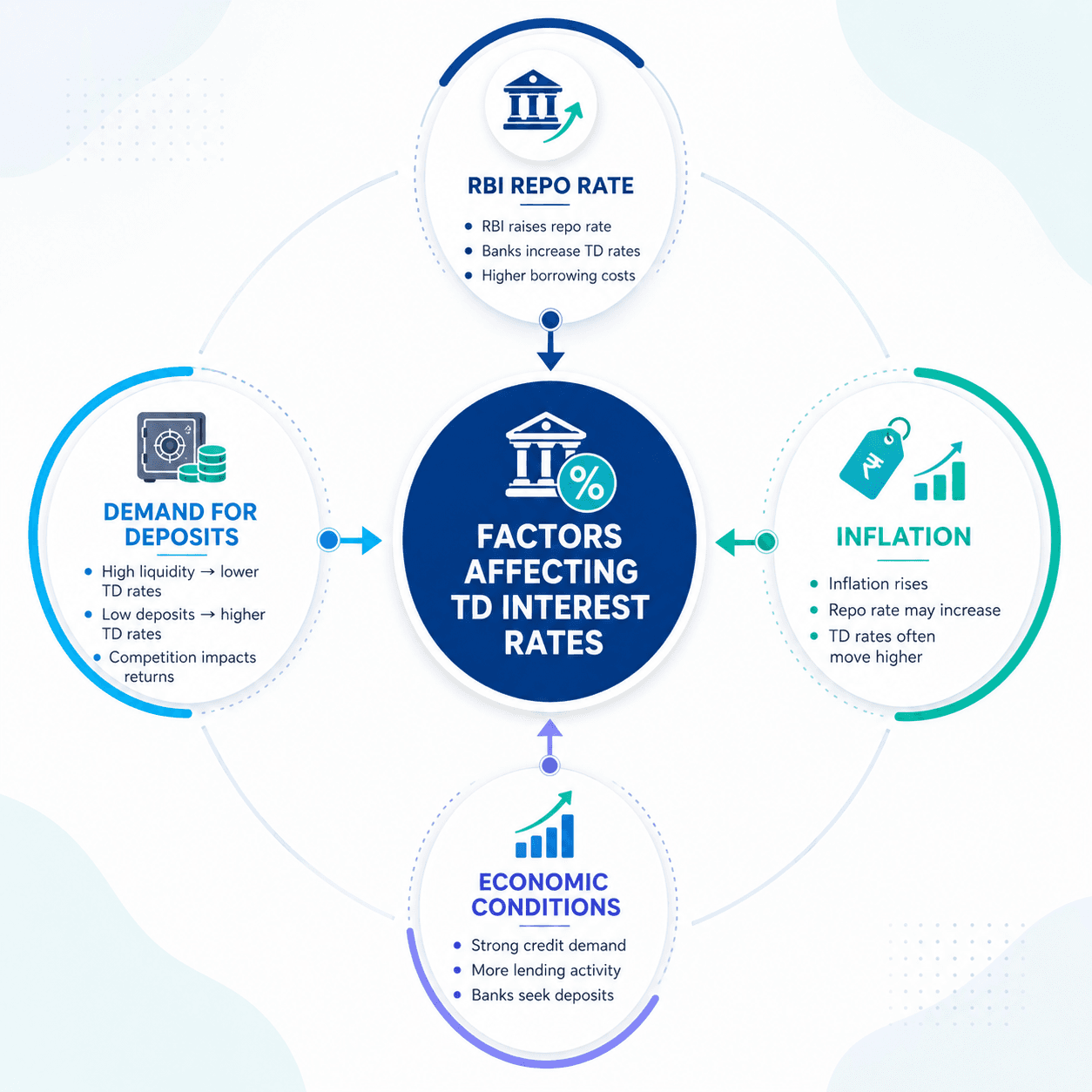

Factors Affecting TD Interest Rates

The wider economic factors that affect TD rates are discussed below.

1. RBI Repo Rate: The rate at which the RBI loans to commercial banks is known as the repo rate. If the repo rate is increased, the cost of borrowing for the bank goes up. Thus, they charge higher interest on loans to recover.

This results in a rise in TD deposit rates to attract more deposits so that the bank has sufficient funds to give out loans. The opposite happens when the repo rate falls.

2. Inflation: The purchasing power of money falls when inflation increases. The RBI increases the repo rate when inflation increases, resulting in a rise in TD rates as well.

3. Economic conditions: Under a strong or growing economy with rising credit demand, the TD rate also increases because the banks want to increase their fund availability to extend loans. The opposite occurs under declining economic conditions.

4. Demand for deposits: If the demand for TD increases and there is a flush of liquidity, banks no longer need to compete aggressively, resulting in lower TD rates. However, if demand falls and banks need funds, they increase TD rates to attract investments.

Now, let us analyse the different types of term deposits.

Types Of Term Deposits

The different terms of term deposits are explained below in detail.

- Regular TD: The typical deposit for those who are not senior citizens is called a regular term deposit. Unlike senior citizen TD rates, these deposits have standard return rates based on tenure, without any special extra rate purely based on age.

- Senior citizen TD: Term deposits where the bank gives an extra interest spread above the standard card rate to residents who are older than a certain age, often above 60 years, are called senior citizen TDs.

- Tax-saving TD: Some term deposits get tax benefits and have a certain lock-in; they are called tax-saving TDs. For instance, tax-saving fixed deposits have a mandatory 5-year lock-in, and investors can claim deductions under section 80C of the Income Tax Act.

- Cumulative and Non-Cumulative TDs: The interest is reinvested into the deposit and compounds as interest rate is levied on principal and accrued interest. In the case of non-cumulative deposits, the interest is not reinvested but paid out periodically to the investor.

Now, to choose the best bank term deposits, investors need to compare the TD rates.

How To Compare TD Interest Rates?

Along with a direct comparison of interest rates offered by different banks and financial institutions, investors should also consider the following parameters.

- Interest payout: Analyse the payout options, namely cumulative and non-cumulative, offered by the issuer. The payout mechanism must match the liquidity needs of the investor.

- Tenure flexibility: Investors must also study the range of tenure offered by the bank. A specific tenure carries the highest interest rate. Investors should ensure that the tenure corresponding to the interest chosen aligns with their needs.

- Premature and withdrawal charges: The penalty charged by the bank during premature closure of a TD must also be considered. In case of emergency or sudden liquidity needs, a bank with lower penalties seems more efficient.

- Senior citizen benefits: TDs offer higher rates for senior citizens, compared to those of regular investors. Furthermore, issuers also offer additional benefits like at-home services, etc. Understanding these benefits can help choose an optimal medium.

Investors should use a term deposit calculator to compare different terms and choose one that fits them better. Furthermore, understanding the difference between TD and FD can aid efficient investing.

TD vs FD: Is There A Difference?

TD and FD are often used interchangeably, but in reality, there lies a key difference between them.

Both TD and FD refer to deposits made for a fixed term at a particular interest rate. However, term deposits are an umbrella term that includes not only FDs but also recurring deposits, post office fixed deposits, etc.

The table below shows the key differences between them.

| Parameter | Fixed Deposit | Term Deposit |

| Principal | Lump sum investment | Lump sum or periodic investment |

| Scope | Narrow | Wide |

| Subcategories | Regular fixed deposit, tax-saving fixed deposit, etc. | Fixed deposit, recurring deposit, etc. |

Therefore, investors can choose from the range of term deposit assets the one that fits them the best.

Conclusion

Term deposits remain one of the most popular investment options for investors seeking stability, predictable returns, and capital preservation. Understanding TD interest rates, the factors that influence them, and the different types of term deposits can help investors make informed decisions that align with their financial goals.

While comparing TD rates in India, it is important to look beyond the interest rate and consider factors such as tenure flexibility, payout options, premature withdrawal charges, and additional benefits offered by the issuer.

Since term deposits are designed to offer relatively low-risk returns, they can play an important role in a balanced investment portfolio. However, investors looking to potentially enhance their returns may also consider other fixed-income options after evaluating their risk appetite and investment objectives.

Looking beyond traditional term deposits?

Explore corporate bonds and fixed-income investment opportunities on Grip and diversify your portfolio with assets designed to generate predictable returns.

FAQs On Term Deposits

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001