Corporate Bonds Vs Securitised Debt Instruments SDI’s: Detailed Comparison For 2026

The Fintech revolution has launched many loan products that help entities from different backgrounds gain access to credit. The MSME sector in India consists of 95% of Indian enterprises and accounts for 29.2% of Indian GDP1. Despite this significance, MSMEs struggle to obtain traditional working capital loans due to the strict rules of traditional banks.

As lending agencies need collateral such as mortgages, share pledges, charges on current assets, etc., there is a need for alternate funding mechanisms. One such product is a Securitised Debt Instrument (SDI). When loans or receivables are securitised, they become financial securities called Securitised Debt Instruments.

In this blog, we’ll break down what SDIs are and how they compare to more familiar options like corporate bonds—helping you understand the key differences in corporate bonds vs SDI investments.

What Are Corporate Bonds?

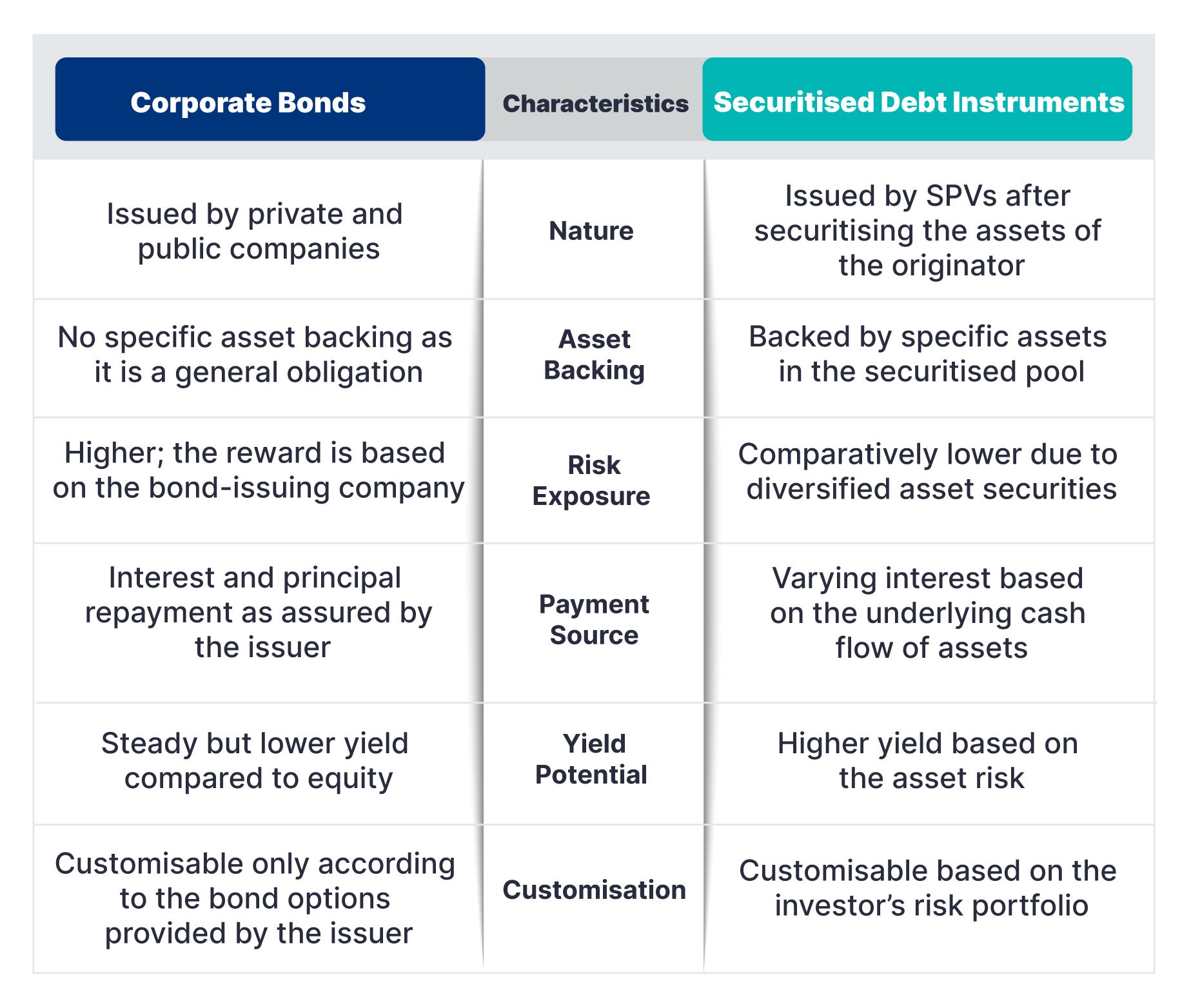

Corporate Bonds are debt obligations when investors lend money to the company issuing the bond, and the company agrees to pay interest on the principal amount. In most cases, the company also returns the principal when the bond matures. Unlike stocks, bonds don't provide equity ownership of the company for the investors.

There are different types of corporate bonds based on credit ratings and return potential. For instance, AAA-rated corporate bonds are considered extremely low-risk and reliable, offering consistent returns with high credit safety. On the other hand, high-yield bonds offer comparatively higher returns but come with slightly elevated risk, making them suitable for investors seeking greater income potential

Corporate Bonds provide a steady income stream, and the company's profitability does not result in a higher interest payment for investors. They also provide more security, as the company is legally obligated to continue making interest and principal payments even if it has financial difficulties. In cases of bankruptcy, bond investors are given priority over shareholders.

Corporate Bonds: Benefits And Risks

Corporate bonds offer the following benefits to the investors:

- Steady income stream.

- Less volatile compared to stocks.

- Choice of corporate bonds and the option to choose the type of reward.

While corporate bonds provide a reliable income irrespective of how the company performs financially, there are still some risks:

- Credit Risk: If the bond issuer goes out of business or declares bankruptcy, investors may lose interest payments and, sometimes, the principal amount.

- Rating Risk: Rating systems may suddenly change the rating of bonds due to unforeseen events.

- Event Risk: Bond issuers may have cash flow problems that affect interest payments and principal repayment.

What Are Securitised Debt Instruments (SDIs)?

Individual loans and debt are securitised to create Securitised Debt Instruments. Investors who invest in these securities can receive income from the underlying assets. SDIs are asset-backed securities. Banks and financial institutions securitise debt to free up capital and lower interest rates.

In the securitisation process, multiple types of loans are collected and pooled together in one bucket to create a debt product. Pass-through certificates (PTCs) are issued to interested investors against these securitised loans. Investors can diversify their portfolios by investing in these asset classes, enabling MSMEs to obtain funding according to their needs.

Originating institutions can pool different types of assets backed by loans to securitise. The Special Purpose Vehicle (SPV) buys these assets and issues PTCs to interested investors on the open market. Based on the types of assets, there are two types of securities: Mortgage-Backed Securities (MBS) and Asset-Backed Securities (ABS). The pooled securities are split into tranches to market to investors based on risk levels or other characteristics. For investors, a tranche is several related securities offered together as a part of a single transaction. These SDI tranches usually have different yields, risk levels, maturities, and repayment privileges.

SDIs: Benefits And Risks

The SDIs benefit banks, SPVs, and investors in many ways. Banks can offer securities at varying risk levels by dividing bonds into risk tranches. SPVs can profit by getting the most value out of previously unavailable or illiquid assets. Investors can determine their risk level and choose the tranches they want to invest in. Some of the key benefits of SDIs for investors are:

- Diversification by investing in varying assets.

- Higher yield compared to traditional assets.

- Access to new markets.

- Customised risk exposure.

Like any other investment option, SDIs have some risks too:

- Credit Risk: The underlying asset's credit quality can impact the value of securities.

- Market Risk: Fluctuations in the market can affect yield.

- Liquidity Risk: Some securitised assets may have limited secondary market liquidity.

- Prepayment Risk: Early repayment of mortgage assets can affect cash flow.

Comparative Analysis Between Corporate Bonds And Securitised Debt Instruments

Both corporate bonds and SDIs provide great options for investors to diversify their risks. Understanding the similarities and differences between these two can help you make better investment decisions.

Considerations For Investors

The Indian securitisation market is growing rapidly, as loan securitisation volumes in the final quarter of FY 2022 increased by 50%, reaching more than INR 50,000 crore2. Microfinance loans are emerging as a popular asset segment due to the fintech revolution in India. Compared to other developed economies, this contribution is much lower. The Sarfaesi Act, 2002, promotes the securitisation of NPAs regulated by RBI guidelines.

The SDIs provide better yield with low market correlations for investors. Since retail investors can also diversify their portfolios with SDI, there is a need to evaluate multiple factors before investing:

- Examine underlying asset quality to compare performance and risks.

- Assess the creditworthiness of the issuer and the credibility of the SPV.

- Conduct cash flow analysis of underlying assets or company.

- Compare returns offered by different types of investment options.

- Pay attention to the securitisation structure to understand risk exposure and complexity.

- Evaluate risk tolerance and diversification strategy to find the right investment instrument

If you're looking to explore high-yield investment options, Grip Invest offers a range of securitised debt instruments and corporate bonds tailored for investors like you.

How To Analyse And Choose Between SDIs And Corporate Bonds

A structured approach helps in evaluating Securitised Debt Instruments India and corporate bonds. A stepwise checklist supports decisions based on risk tolerance, liquidity needs, investment horizon, and income expectations.

Step 1. Assess risk tolerance

Corporate bonds with strong ratings provide predictable stability. SDIs diversify risk by pooling many underlying loans, but carry SDI investment risks like prepayment and asset quality fluctuations.

A clear Investment risk comparison corporate bonds vs SDI helps determine suitability.

Step 2. Evaluate liquidity needs

Corporate bonds usually trade more frequently. Many platforms also provide quick exit features. SDIs depend on the quality of the pool and may have lower secondary activity. This difference influences Liquidity in SDIs vs corporate bonds.

Step 3. Define investment horizon

Corporate bonds suit medium to long horizons with fixed maturity dates. SDIs fit medium horizons where cash flows arise from underlying receivables. Investors with shorter horizons may prefer corporate bonds. Those seeking higher periodic income may review SDI structures.

Step 4. Compare expected returns

Corporate bond returns vary by rating and tenure. A typical range for Corporate bond yields India is 9% to 12% for investment-grade issuers. SDIs often deliver higher returns based on loan pool characteristics. Some SDIs fall in the 11% to 14% range and are considered among the Best alternative investments India 2026 in the fixed income space.

Step 5. Review taxation effect

Taxation differences influence net outcomes. Corporate bonds and SDIs have similar interest taxation but differ in capital gains rules depending on listing status. This makes tax-adjusted return comparison important for the final decision.

Market Liquidity And Exit Strategies

Liquidity is not uniform across fixed income products. Corporate bonds generally offer higher trading activity on exchanges. SDIs trade less often because demand depends on the underlying asset pool. These distinctions shape Liquidity in SDIs vs corporate bonds.

Corporate bonds

Corporate bonds offer clearer price discovery through exchange listings and platform-based selling. Many retail platforms allow early exit for a wide range of issuers. Liquidity improves for higher-rated issuers and popular maturities.

SDIs

SDIs rely on the pool’s structure and investor demand. Some SDIs list on exchanges but trading volumes may remain limited. Many platforms provide assisted exit mechanisms that improve accessibility. Liquidity improves when underlying assets are short tenure and cash flows are predictable.

Corporate bonds remain stronger on the immediacy of exit. SDIs depend on platform support and investor interest. Investors reviewing Corporate bonds vs SDI India should evaluate the expected need for early withdrawal.

Regulatory Environment And Framework

Both corporate bonds and SDIs are regulated in India, but fall under different frameworks. This affects transparency, investor protection, and the perception of SDI investment risks.

Corporate bonds

Corporate bonds fall under SEBI regulations for issuance, listing, disclosure, and credit rating. Issuers must maintain reporting standards. Trustees monitor asset protection. This ecosystem ensures oversight for investors in fixed income and High yield bonds India.

SDIs

SDIs are governed under the securitisation framework defined by the Reserve Bank of India. Rules cover pool creation, minimum retention requirements, due diligence, reporting, and credit enhancement norms. Listed SDIs also follow SEBI listing rules.

This structure ensures that Securitised Debt Instruments India operates under clear guidelines and that disclosure remains consistent.

Both categories operate under regulated frameworks. Corporate bonds follow capital market rules. SDIs follow RBI securitisation norms. These systems enhance credibility and support the growth of Best alternative investments India 2026 within the fixed income market.

Taxation Nuances And Capital Gains Treatment

Taxation works differently for corporate bonds and SDIs in India. This affects interest income, holding period rules, and capital gains. These differences matter when comparing tax treatment of SDIs vs corporate bonds.

Interest income

Interest from both corporate bonds and SDIs is taxed as income from other sources. The rate depends on the tax slab of the investor. This applies to listed and unlisted securities. The treatment is similar for Taxation on SDIs India and for corporate bonds.

Capital gains on corporate bonds

Corporate bonds held for up to twelve months result in short-term capital gains. These gains are taxed at the investor’s slab rate.

Corporate bonds held for more than twelve months result in long-term capital gains. LTCG is taxed at 10% without indexation. This rule applies only to listed bonds. Unlisted bonds require a longer holding period of 36 months for LTCG classification.

Capital gains on SDIs

Capital gains on listed SDIs follow the same rules as listed corporate bonds. Short-term capital gains apply to units sold within twelve months. Long-term capital gains apply after twelve months and are taxed at 10% without indexation.

Some SDIs are unlisted. In such cases, the holding period for LTCG becomes thirty six months. This increases the effective tax impact.

These differences are important for investors comparing Corporate bonds vs SDI India from a tax efficiency point of view.

Indexation is not available for listed corporate bonds or listed SDIs. This makes post-tax returns more dependent on nominal yields and holding period strategy. These factors influence decision-making for those considering High yield bonds India or SDIs

Conclusion

Investors must look beyond traditional investment instruments and diversify their portfolios to avoid wealth reduction due to increasing inflation. The high-yielding non-equity market-related instruments provide better returns and offer protection. Many SEBI-regulated investment instruments previously available only to HNIs are now accessible to retail investors. Investors can continue using their Demat account and invest in SDIs listed on the National Stock Exchange (NSE). Corporate bonds continue to provide reliable income even though the yields are lower than other investment options. In the context of corporate bonds vs SDI investments, retail investors can now use investment discovery platforms to explore alternative investment opportunities offering better yields and diversification. They should carefully examine SDIs and Corporate Bonds and invest per their risk profile and investment goals.

Grip introduced the first SDI listed on the NSE, pioneering SDI investment opportunities in India. Explore different alternative investments with Grip Invest to build wealth without worrying about inflation.

FAQs On Corporate Bonds Vs SDIs

1. Are SDIs riskier than corporate bonds?

Securitised Debt Instruments (SDIs) are risky as they depend on the performance of underlying loan pools. However, each SDI comes with a credit rating and security cover. If the credit rating of the SDI is A or above, you can consider it a low-risk investment option. Further, SDIs are structured by pooling thousands of loans together, and hence, the risk gets diversified.

On the other hand, Corporate Bonds are also risky as they do not offer diversification benefits. If you want to diversify your portfolio of bonds, then you will be required to purchase different bonds of different issuers. Although they are also rated by credit rating agencies. Hence, to assess the risk of Corporate Bonds, you should look at the rating of the bond.

2. How does liquidity compare between SDIs and corporate bonds in India?

Corporate bonds generally offer better secondary market liquidity, while SDIs are less frequently traded and can be harder to exit early. However, Grip Invest offers a sell-anytime feature to its investors for Corporate Bonds and SDIs. With this feature, investors can sell their bonds and SDIs units anytime on Grip Invest.

3. What are typical yields on Indian corporate bonds vs SDIs?

Corporate bonds usually offer 9%–12% annually for quality issuers (investment-grade bonds). SDIs often yield higher 11%–14%, reflecting their higher risk profile.

4. Can retail investors access SDIs like they access corporate bonds?

Earlier, direct access to SDIs was limited for retail investors. Most participants participated through debt funds or platforms offering fractional investment in such instruments. However, Grip Invest has made this possible for retail investors to invest in SDIs by offering them at a minimum investment of just INR 10,000.

5. How is taxation different for corporate bonds and SDIs?

Both are taxed on interest income as per the investor’s slab. However, capital gains tax treatment may vary depending on the holding structure and investment vehicle.

References:

- Press Information Bureau <https://tinyurl.com/386yzutu>

- CRISIL Ratings <https://tinyurl.com/3ssd5mej>

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip, the latest financial knick-knacks and shenanigans that take place in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities are subject to risks. Read all the offer-related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading. This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for the consequences of any actions taken based on the information provided. For more details, please visit https://www.gripinvest.in/.

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001.