Credit Card Against Fixed Deposit: Eligibility, Benefits And Risks

When a bank offers you a credit card, it evaluates your creditworthiness by analysing historical patterns. CIBIL and other credit reports are quite effective, as they summarise the individual's previous loans, repayment history, and any defaults or delays. However, there may be circumstances in which an applicant has just joined their first job and has absolutely no credit history.

In such cases, it becomes difficult for banks to assess an individual's creditworthiness. Besides this, there might be people with average to poor credit histories who are looking to apply for a credit card but might find it difficult to obtain one.

There is an excellent alternative to such people in the form of a secured credit card India. Instead of relying on an applicant's credit history and profile, a bank allows a fixed deposit to be used as collateral and issues a credit card against it. This not only reduces the lender’s risk but also simplifies the approval process. A credit card against FD is therefore designed to help individuals access credit even without a strong borrowing history. Let us find out more about it.

What Is A Credit Card Against FD?

It is a bit different from the conventional credit cards, where applicants are ‘pre approved’ for a certain credit limit based on their credit history. A credit card on fixed deposit is a secured credit card in which a customer’s fixed deposit serves as collateral for the card issuer.

The bank often allows a certain percentage of the fixed deposit to be credited to the customer, and the structure is beneficial because the offered credit is already backed by funds deposited with the bank.

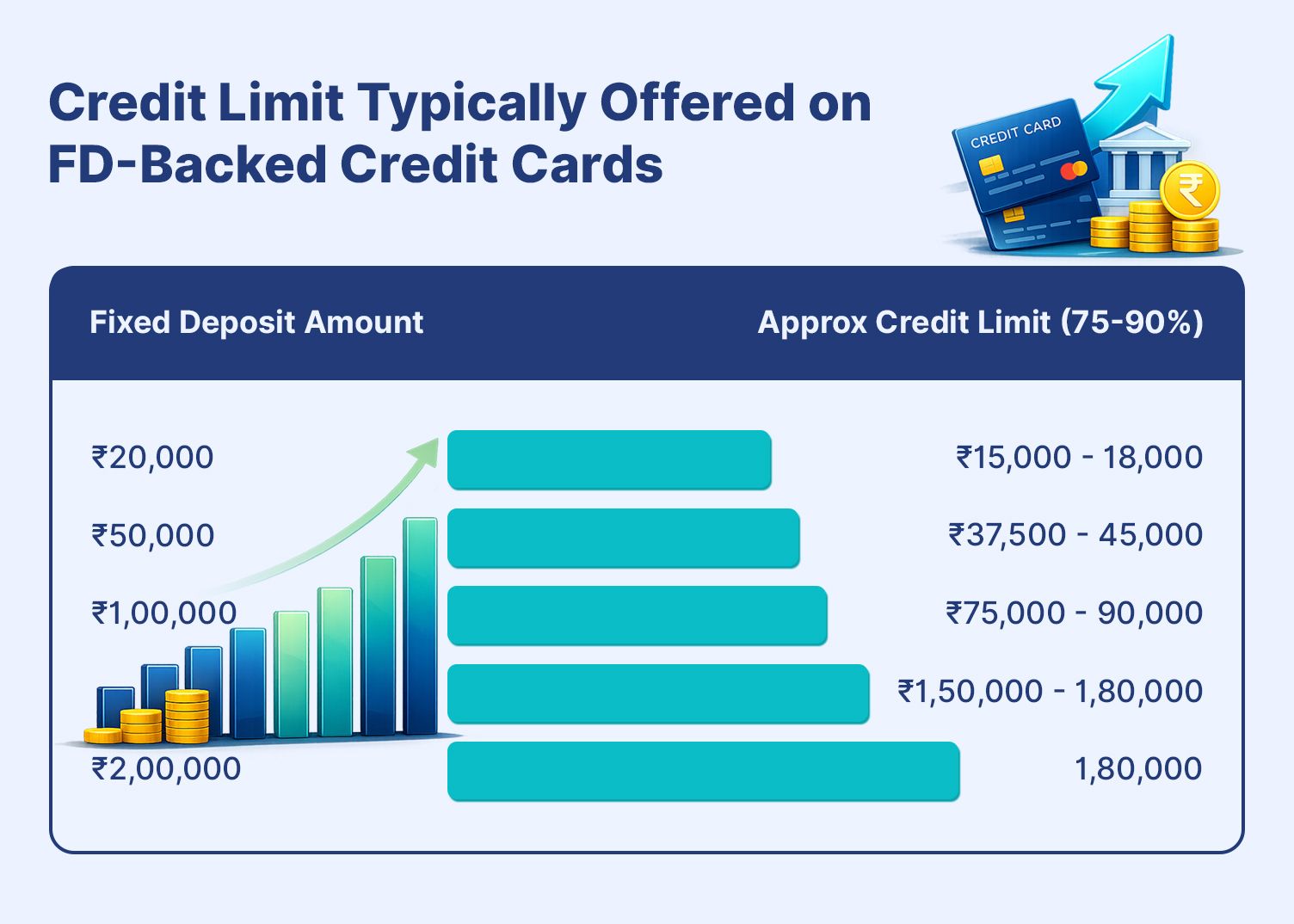

The credit limit can range from 75% to 90% of the fixed deposit value. An FD backed credit card protects the lender against any possible default commonly associated with new borrowers. It also helps increase total deposits and expand the customer base by offering credit cards to people with no or poor credit history.

The minimum FD for credit card India can start as low as INR 2000 to higher amounts, depending on the bank and type of card applied. There are various popular banks offering this alternative, such as the Axis Bank FD credit card, SBI credit card against FD, ICICI FD secured card, and the IDFC FIRST WOW card FD.

Each of these credit card have different limits, terms, and conditions, as finalised by the issuing banks.

Also Read: FD Auto Renewal: What Are The Risks & Benefits and How To Do It?

Benefits And Limitations Of FD Backed Credit Cards

There are numerous benefits of FD Credit Cards, especially for individuals with poor to no credit history. However, it is not restricted to such individuals only, as anyone can apply for a credit card against FD in India.

Let us start with the most obvious advantages. The biggest advantage is easier approval. Since the card is backed by a fixed deposit, banks do not need to rely heavily on credit history. This makes it easier for students or individuals without prior borrowing records to access a credit card.

These cards have almost identical features to regular credit cards: you can shop online, earn reward points, and get complimentary benefits, depending on the card’s terms and conditions and the issuer.

The spending limit on these cards is usually linked to the deposit value. The credit limit on an FD card typically ranges from 75% to 90% of the deposit amount, helping maintain disciplined spending while still providing access to credit. Here is an illustration:

Figure 1.0: Credit Card Limit Vs. FD Amount

However, there are a few limitations and considerations to keep in mind. First, your funds must remain locked in the fixed deposit until the card is active. While the deposit continues to earn interest, the money cannot be accessed freely.

In addition, when you compare a secured card vs unsecured card, you find out that the secured ones often have lower credit limits and fewer premium benefits compared to high-end unsecured cards issued to experienced borrowers; however, this depends on the chosen card and the issuer’s terms and conditions.

How Does It Helps Build Credit Score?

One of the major reasons people opt for such cards is to build a CIBIL with FD card usage. Credit card activity is typically reported to credit bureaus such as CIBIL, Experian, Equifax, and CRIF High Mark. However, you must remember that maintaining a decent repayment behaviour is paramount, even if you have taken up an FD-backed credit card.

Over time, responsible usage can improve credit scores and make individuals eligible for higher-limit credit cards or other borrowing products. Many financial experts recommend secured cards as a starting point for individuals with no credit history who want to gradually establish their credit profile.

Who Should Use It

Besides the individuals who are finding it hard to get a pre-approved credit card, this is best suited for:

1. Students

Students who are beginning their financial journey may not have an established credit record. A secured card can help them start using credit responsibly and gain experience managing repayments.

2. First Time Credit Users

Young professionals new to borrowing often struggle to secure approval for traditional credit cards. Understanding the eligibility for secured credit card FD products can help them start building a credit profile with minimal risk.

Today, most banks also allow customers to how to apply FD credit card online through internet banking or mobile apps, making the process simpler and faster for new applicants. With an Aadhaar-based client onboarding system, it takes only a few minutes to evaluate an individual’s credit history and determine whether they are eligible for a pre-approved card.

Many banks instantly offer an FD credit card to people with poor credit scores to ensure they not only get a card but also start building their credit history for future loan enquiries.

Conclusion

A credit card against a fixed deposit is a practical way to begin using credit even when traditional approval may be difficult. By using an FD as collateral, banks are able to offer credit cards to individuals who may not yet have a strong borrowing history. At the same time, the cardholder benefits from the convenience of digital payments, reward programmes, and the opportunity to gradually build a healthy credit profile through responsible usage.

However, like any financial product, it should be used carefully. Timely repayments, disciplined spending, and understanding the terms of the card are essential to ensure that the card works in your favour rather than becoming a financial burden.

While a secured credit card helps establish a credit footprint, building long-term financial stability requires a broader approach to financial planning. Alongside responsible credit usage, allocating savings into instruments like fixed deposits, corporate bonds, or other fixed-income investments can help strengthen your overall financial position. Platforms such as Grip Invest enable investors to explore curated fixed-income opportunities, allowing them to diversify their savings while maintaining predictable returns. By combining disciplined credit habits with structured investment choices, individuals can steadily build both a strong credit profile and a resilient financial future.

FAQs

1. What is a credit card against FD?

A credit card against an FD is a secured credit card issued by a bank, with the fixed deposit serving as collateral. The bank places a lien on the FD and offers a credit limit typically linked to a percentage of the deposit amount.

2. Can FD backed credit card build a credit score?

Yes. Transactions and repayments on an FD-backed credit card are reported to credit bureaus such as CIBIL. If the cardholder uses the card responsibly and pays dues on time, it can help build or improve their credit score.

3. Is FD blocked for a credit card?

Yes. The bank places a lien on the fixed deposit while the credit card remains active. This means the FD continues earning interest but cannot be withdrawn until the card is closed or all outstanding dues are cleared.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001