Credit Spread Explained: What The Yield Gap Tells Investors About Risk

Investors do not evaluate bonds solely by comparing interest rates; they also assess the level of risk they are willing to accept to earn those returns. Even bonds with the same maturity can offer significantly different yields, and such variations are rarely coincidental. This difference is known as the credit spread. Credit spreads reflect how the market prices risk, credit quality, and uncertainty associated with an issuer.

For fixed-income investors, especially in the corporate bond segment, understanding credit spreads is essential. Investment decisions are not merely about chasing higher yields, but about making informed choices that balance return expectations with underlying credit risk.

What is Credit Spread?

A credit spread, in simple terms, is the yield difference between two bonds of similar maturity but different credit ratings. This comparison is most commonly made between a corporate bond and a government bond. Government securities are considered almost risk-free because they are guaranteed by the sovereign, whereas corporate bonds have varying default risks based on the issuer's financial standing.

The additional yield investors require to hold a risky bond over a government bond is referred to as the credit risk premium, captured in the credit spread.

The difference between the yields of a government bond and a corporate bond spread of similar maturity is not the same. For instance, if a 5-year Government of India security yields 6.5% while an AAA-rated corporate bond of the same maturity offers 7.5%, the credit spread is 1.5% (150 basis points). This yield spread represents the additional return investors demand for taking on corporate credit risk instead of investing in a sovereign-backed instrument.

Why Credit Spreads Change Over Time

The spreads of credit do not remain constant; they change continuously with market conditions. The additional yield investors require to take on credit risk depends on changes in economic growth, interest rate environments, issuer financial health, and investor behaviour.

1. Economic Cycles and Interest Rates

Earnings and stable cash flows reduce perceived default risk during economic expansions, and therefore, credit spreads tend to decrease. Conversely, inflationary interest rates and economic growth slowdowns raise borrowing costs, intensifying uncertainty and increasing risk aversion, which widens spreads.

2. Company-Specific Credit Risk

A corporate bond’s credit spread is directly related to its financial strength. Increased leverage, declining profitability, or governance issues increase the risk of default, and issuers must offer a wider yield to compensate investors for the risk of credit deterioration.

3. Market Sentiment and Liquidity

Credit spreads are highly influenced by investor sentiment and market liquidity. During risk-off periods, risky assets become less popular, leading to low liquidity in corporate bonds and wide spreads. Once confidence is restored and liquidity increases, spreads between issuers generally converge.

Credit Spread in India: Government vs Corporate Bonds

The analysis of bond credit spread India can help investors understand the differences in risk and returns between sovereign-based securities and corporate issuers, that is, how risk and returns vary across the bond market by creditworthiness, liquidity, and perceived default risk.

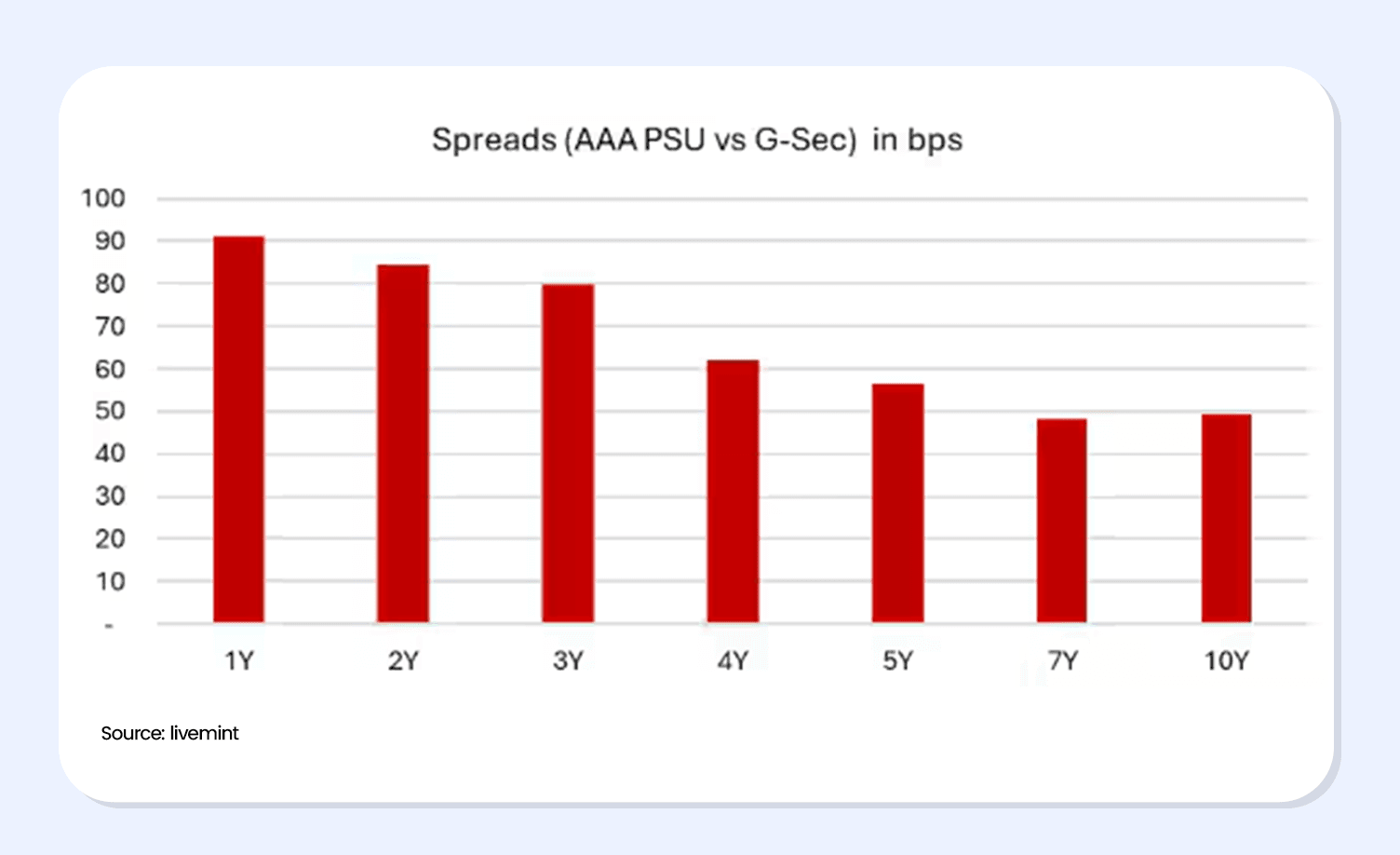

- PSU Bonds vs Private Corporate Bonds

PSU bonds tend to be issued at narrower credit spreads than private corporate bonds, reflecting perceived government support and investor confidence. Yields for private issuers are higher because of a wider corporate bond spread driven by business risk and low liquidity.

- Investment-Grade vs. Lower-Rated Issuers

Investment-grade bonds have moderate interest rates that are relatively stable and narrower credit spreads, indicating a low default risk. Issuers with lower ratings have wider spreads to cover increased credit risk premiums, greater volatility, and a higher likelihood of payment stress in a downturn.

How Investors Use Credit Spread in Portfolio Decisions

Credit spreads are a risk-assessment tool used by investors, not a guarantee of returns. While wider spreads may appear attractive, they often signal higher uncertainty or weaker credit quality. Focusing only on bonds with the highest spreads can expose portfolios to concentrated credit risk and potential losses in the event of default. Experienced investors evaluate whether a spread adequately compensates for credit risk, liquidity, and duration.

Balancing yield and credit quality is central to fixed-income portfolio construction. Conservative investors typically prefer lower spreads from higher-rated issuers to preserve capital, while more aggressive investors may allocate a limited portion of their portfolios to higher-spread bonds to seek incremental returns. Credit spread analysis also helps investors tactically shift between government and corporate bonds in response to changing market conditions.

Credit Spread and Fixed Income Options

Credit spread analysis is particularly relevant when evaluating fixed-income options such as listed corporate bonds, PSU bonds, and other market-linked debt instruments. These instruments offer different spreads based on issuer credit quality, tenure, and prevailing market conditions. Comparing spreads helps investors assess whether the additional yield adequately compensates for the incremental risk.

Today, certain digital platforms, such as Grip Invest, allow investors to view and compare bond yields, tenors, and credit ratings across issuers in a transparent manner, supporting more informed, risk-aware fixed-income allocation decisions.

FAQs

1. What does a widening credit spread indicate for investors?

A widening credit spread usually signals rising credit risk or uncertainty in the market. Investors are demanding higher compensation to hold corporate bonds instead of government securities, often during economic slowdowns or risk-off phases.

2. Are higher credit spreads always better for returns?

No. Higher credit spreads mean higher yields, but they also reflect higher default risk or weaker credit quality. Returns only improve if the issuer remains financially stable and meets all interest and principal obligations.

3. How do credit spreads differ between PSU bonds and private corporate bonds in India?

PSU bonds typically have narrower credit spreads due to perceived government backing and better liquidity. Private corporate bonds usually offer wider spreads to compensate for higher business and credit risk.

4. How can retail investors track and compare credit spreads easily?

Retail investors can track credit spreads by comparing corporate bond yields with government securities of similar maturity and credit rating. Digital bond platforms like Grip Invest simplify this by displaying yields, tenors, and ratings in one place for easier comparison.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001