Credit Utilisation Ratio: The Hidden Factor Impacting Your Credit Score

Nidhi is a 33-year-old journalist working with a leading news agency. She has been in active employment since she completed her master's in journalism and mass communication. As a daughter of an ex-banker, she was taught financial discipline and the importance of avoiding excessive debt.

She bought her first car in an all-cash deal and has never applied for a credit card. Recently, she wished to buy a flat in her home city and believed she would have no issues obtaining a housing loan. However, she was shocked to find that her CIBIL score was too low, despite maintaining high account balances throughout the past decade.

A CIBIL (Credit Information Bureau (India) Limited) report is one of the most reliable and popular means of adjudging the creditworthiness of an individual. If you have maintained a healthy history of obtaining and repaying loans (and interest) in the past, your CIBIL score will be on the healthier side. On the other hand, if you have missed out on any payments or defaulted on a loan, your CIBIL score is most likely to be poor, which further jeopardises your chances of obtaining new loans.

Most individuals think that repayment history and new loan inquiries are among the most critical factors in building their credit score. However, an equally important factor, your credit utilisation ratio, is often ignored.

This simple percentage reflects how much of your available credit you actively use and serves as a strong signal of borrowing discipline. A consistently high ratio can lower your score, even if you never miss payments.

Let’s understand everything you need to know about the credit utilisation ratio and how to improve it.

Also Read: Credit Score Vs CIBIL Score: What's The Difference?

What Is Credit Utilisation Ratio?

The credit utilisation ratio is the proportion of utilised credit compared to the total available limit. For example, you have two credit cards with a total available limit of 5 lakhs each. You have spent 1.5 lakhs on each credit card. It implies your credit utilisation ratio is 30% (3,00,000/10,00,000)*100.

A low and stable utilisation level signals financial discipline, while a high one suggests greater dependency on credit.

Credit Utilisation Ratio Formula:

Credit Used ÷ Total Credit Limit × 100

If you use a high limit consistently, it could negatively impact your CIBIL score. Most financial institutions and credit bureaus recommend maintaining an ideal credit utilisation of 30 per cent or lower. Excessive use above this range, especially when sustained for several billing cycles, may negatively impact your credit score and raise lender concerns.

If you have more than one credit card, a credit utilisation ratio calculator can help you assess your overall usage as well as card-wise utilisation.

Why It Matters For Your Credit Score

If you are consistently utilising a large portion of your total available credit, it sends a negative signal to credit agencies, banks, and financial institutions. Your risk levels will be deemed too high, even when you make timely payments.

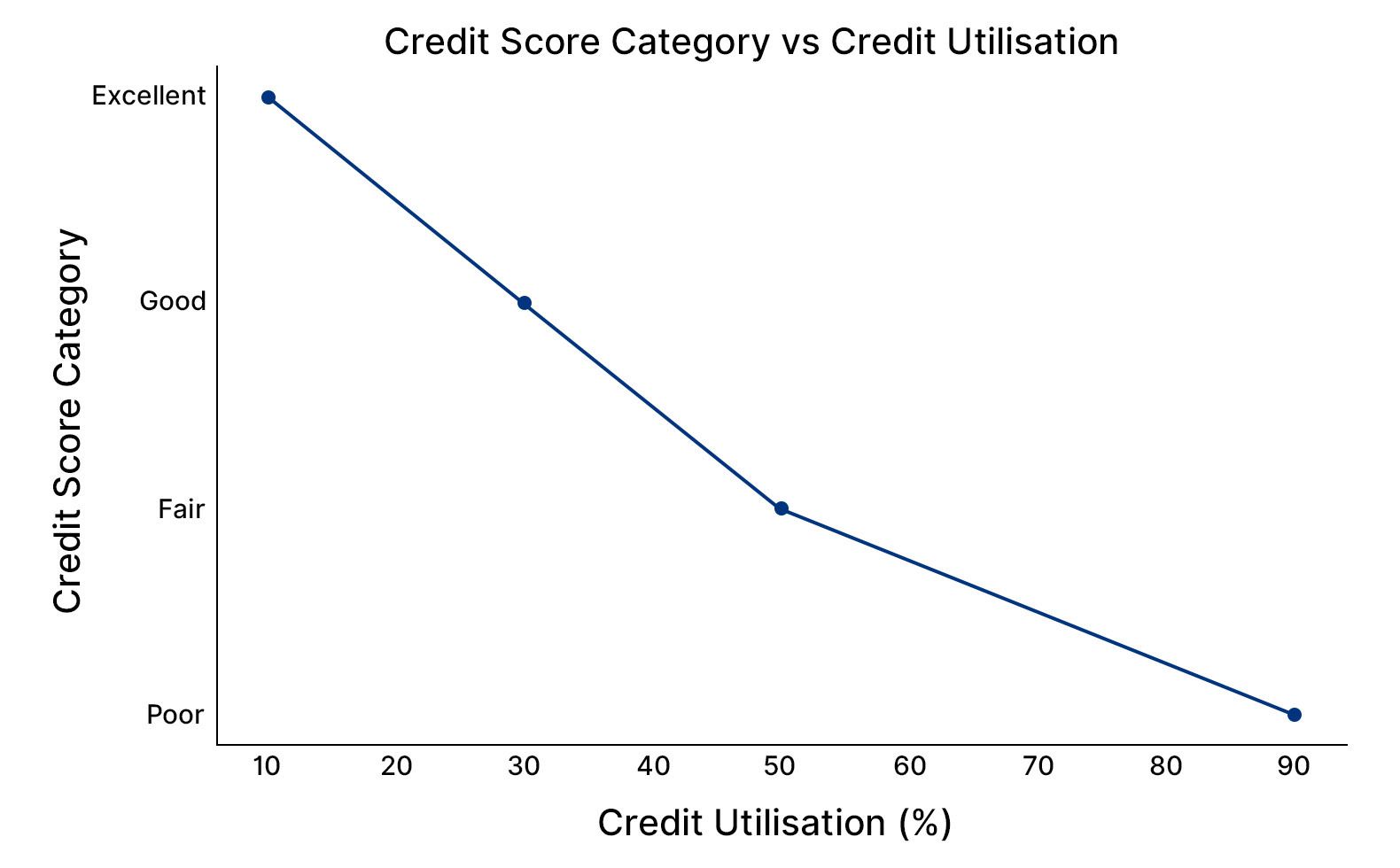

A utilisation level of 30 per cent or below is generally healthy, while usage of 50 per cent may start pulling down your score. When utilisation touches 80–90 per cent, it signals heavy credit dependence and can significantly reduce your CIBIL score. A high credit utilisation impact on credit score will be negative.

Your chances of obtaining future and larger loans (such as a home loan or business loan) depend on your CIBIL score. Here is a chart showing the tentative relationship between the credit score and credit utilisation:

You must remember that consistently utilising a high ratio of your available credit can eventually jeopardise your credit score and creditworthiness. The chart above is representative as the credit agencies do not publish exact values depicting the relationship between a credit utilisation ratio and its relevant impact on the credit score (in basis points or otherwise).

Also Read: Credit Card Vs Debit Card : Which One Is Better?

Tips to Maintain Healthy Utilisation

The most critical mantra here is to keep your spending in check and ensure you never spend more than your monthly income. Credit cards often create the illusion of having money in the bank, whereas it is nothing but a loan at an extremely high interest rate (up to 40% per annum).

Hence, your outstanding amount can easily double in a matter of a few months.

Here are a few credit utilisation tips:

- Track monthly spending closely to keep your credit utilisation ratio within the ideal credit utilisation range of 30 per cent.

- Make multiple small repayments during the month to reduce your closing balance and improve credit utilisation.

- Consider a credit limit increase only if you can maintain disciplined spending; higher limits naturally lower utilisation.

- Spread expenses across multiple cards to avoid high utilisation on any single account.

- Use a credit utilisation ratio calculator or app alerts to monitor usage and prevent sudden spikes.

Long-Term Credit Management

It is important to follow strict financial discipline to ensure your creditworthiness improves over the period. Having a stable credit utilisation ratio is one of the components that not only helps build the CIBIL report but also develops healthy financial habits. As your finances grow, consider increasing your credit limit to keep utilisation low without changing your spending patterns.

Avoid habits such as frequent max-outs or sudden spikes, as they can negatively impact your profile. Credit utilisation and credit limit are inversely related, so you should consider limiting your expenses and cutting down on unnecessary spending.

You can also use apps such as a budgeting, spending tracker, and a credit utilisation ratio calculator to keep track of your expenses and maintain discipline.

Conclusion

The credit utilisation ratio is a simple, effective, and quite underrated factor that shapes your credit score. Keeping utilisation consistently low, tracking monthly spending, and managing your credit limit responsibly can significantly improve long-term financial reliability. By maintaining disciplined usage across cards and monitoring utilisation patterns, you build a stronger credit profile, better loan eligibility, and healthier borrowing power.

Eventually, everything boils down to your financial discipline. Always remember to use debt effectively and avoid spending beyond your monthly or annual income.

Visit Grip Invest today!

FAQs On Credit Utilisation Ratio

1. What is the ideal credit utilisation ratio in India?

The ideal credit utilisation ratio is 30 per cent or lower. Staying below this threshold signals disciplined usage and supports a stronger CIBIL score. For top-tier scores, keeping utilisation in single digits is even more effective.

2. How can I reduce my credit utilisation quickly?

You can lower utilisation by making multiple small repayments during the month, spreading expenses across cards, or requesting a credit limit increase without increasing spending. Reducing large one-time purchases or switching them to debit also helps immediately.

3. Does closing old cards affect my utilisation ratio?

Yes. Closing an old card reduces your total credit limit, which can increase your overall utilisation ratio even if your spending stays the same. This may negatively impact your score, especially if the closed card had a high limit or long history.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001