Gold Monetization Scheme Explained: Interest Rates, Eligibility And Tax Benefits

Indians have gold just sitting idle in their homes that hasn't been used in a long time - gold like this has value, just as much as a bank account does. Using gold to make money will help the whole country grow if enough of it is turned into working assets.

With the introduction of the Gold Monetisation Scheme (GMS) by the Indian government, new opportunities have become available by taking your old jewellery and creating a new form of investment that pays interest on your deposited gold.

What Is The Gold Monetisation Scheme?

This new program gives individuals an incentive to deposit idle gold at banks instead of allowing it to remain lost or unutilized for many years. In addition, by creating an avenue for Gold to be put back into circulation as an income-producing asset. This scheme will also help significantly decrease the amount of gold that is imported into India each year and thus saving India a significant amount of money.

As a result, any gold deposited will be melted down and purified, then lent out by the bank to either jewellers or industries, thus generating an ongoing stream of interest to the owner while actively contributing to India's overall economy.

How The Gold Monetisation Scheme Works

The process for participating in the gold deposit scheme India is quite simple. You start by going to the banks that have agreed to participate in order to make your deposit. There is an advanced machine available at each bank that will allow them to determine the purity of the gold you are depositing and, therefore, the value of your gold when it has been deposited.

1. Deposit Process

When you make a deposit, you will be paid interest on the value of the gold deposited, and that interest is calculated based on the purity of the gold that you have deposited. Upon the expiration of your tenure, you are entitled to redeem your account balance at your option in either gold coins or cash.

- To make your initial deposit, you would walk into a participating bank with either your gold jewellery or coins ready to be deposited.

- The bank employee will then weigh and test your gold item(s) to determine the purity of the gold you have deposited.

- The employee will then give you a deposit certificate that will have all of the information regarding the quantity and purity of your deposit.

For example, if a family brought in their grandmother's old jewellery to deposit in order to earn interest on the deposit to help pay for their children's education, the deposit transaction would be completed in that time frame.

2. Purity Testing

Banks utilise either fire assays or XRF machines to maintain a precise determination of the karat in the gold, without having to melt the gold piece prior to conducting the assay. Each piece that is stamped with a Hallmark is also processed much faster through the process, whereas every other piece goes through a more thorough and reliable testing process.

3. Tenure Options

Choosing a short term deposit will provide you with more liquid access to funds quickly, while a long term deposit will provide the best possible long term yield from compounding interest. A medium-term deposit of gold investment provides both. Therefore, making it a balanced approach to growth.

4. Interest Earnings

Interest payments will be made to you based on the amount of pure gold deposited in your account and will be paid to you through your bank account every six months. These rates are based on the returns that are determined by the government bond market. Therefore, they can be anticipated to remain stable and predictable at all times.

5. Interest Rates and Returns

The interest rate that you earn based on the gold monetisation scheme will differ depending on the length of time that you will hold your deposit, as the longer you hold onto your deposit, the higher will be your yield on your deposit. To match your needs, short term depositors will earn modest returns based on their urgent need for funding, whereas medium-term depositors will earn yields that provide them with balances as well as access to their funds.

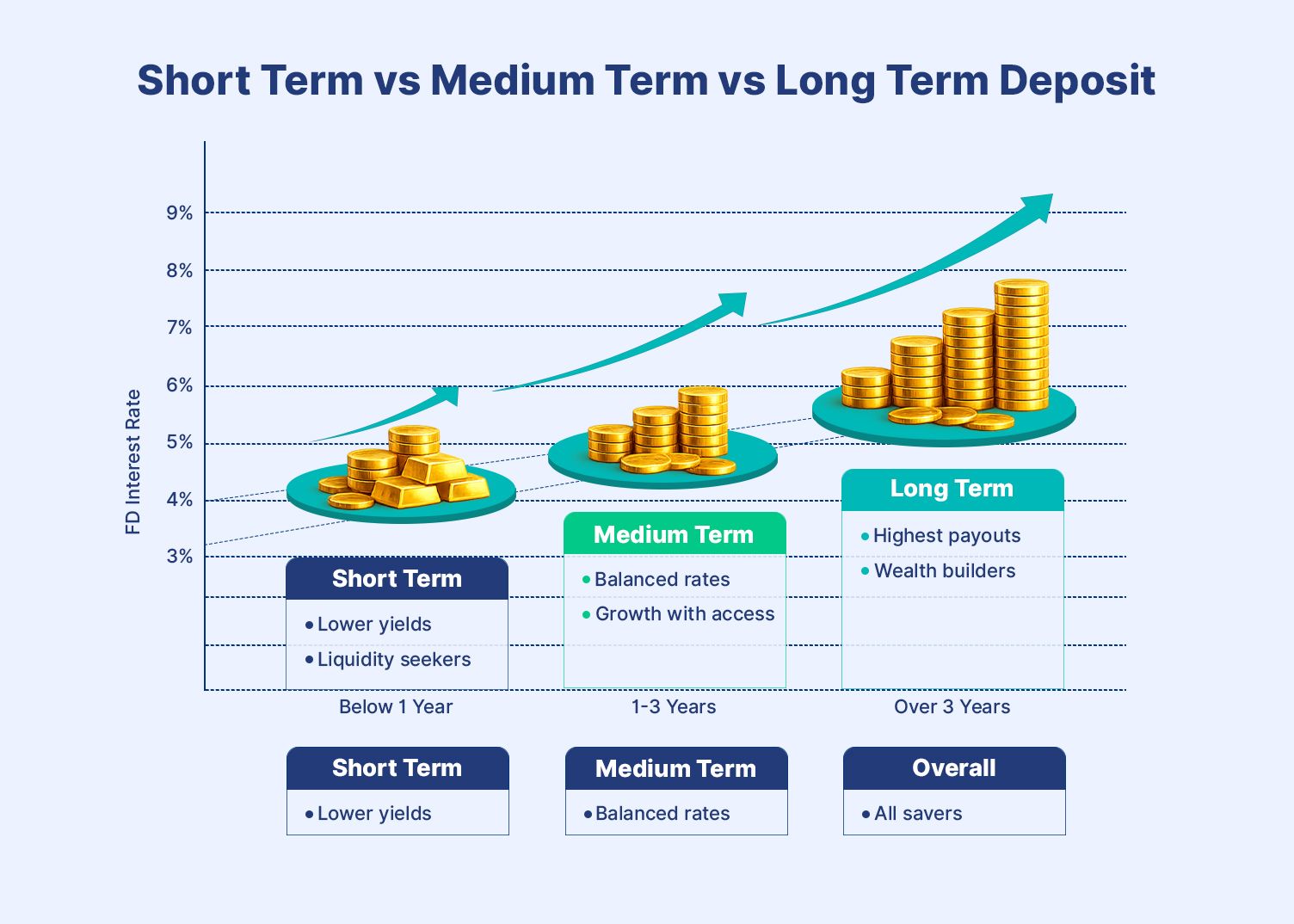

Short Term Vs Medium Term Vs Long Term Deposit

Short-term deposits below one year give basic interest for those needing funds soon after the deposit. Medium tenures from one to three years strike a sweet spot blending decent returns with reasonable access. Long-term, over three years, maximises the gold monetisation scheme interest rate through sustained holding benefits fully.

| Tenure Type | Interest Range | Best For |

| Short Term | Lower yields | Liquidity seekers |

| Medium Term | Balanced rates | Growth with access |

| Long Term | Highest payouts | Wealth builders |

| Overall | Competitive | All savers |

Tax Benefits Under The Scheme

GMS benefits India include attractive tax treatments that enhance the attractiveness of the Scheme for all investors globally.

- Depositor-interest income will never be taxed, irrespective of the annual amount.

- Any capital gain tax on the redemption of the maturity in gold or cash is avoided as opposed to the sale of physical gold.

- No wealth tax will apply to deposited assets therefore the compliance process is much less complicated. As a result, the GMS structure significantly improves overall returns versus other options.

Hypothetical Example

A retiree may deposit gold into GMS while not being concerned about receiving any tax-issues notice when withdrawing their half-yearly interest; therefore, allowing the retiree to continue living with peace of mind throughout his/her retirement.

Gold Monetization Scheme Vs Sovereign Gold Bonds Vs Physical Gold

When evaluating which option to pursue between the three options including gold monetization scheme, Sovereign Gold Bonds, or physical gold.

| Aspect | Gold Monetization | Sovereign Gold Bonds | Physical Gold |

| Risk | Bank guaranteed | Govt backed | Theft/purity issues |

| Return | Interest + gold value | Interest + appreciation | Price rise only |

| Liquidity | Tenure-based | After 5 years/trade | Sell anytime |

| Taxation | Interest & maturity tax-free | Maturity tax-free | Gains taxed |

Eligibility And How To Participate

- Being an initial participant, each resident must deposit at least 8 grams of pure equivalent to participate.

- Terms and conditions meet the Government of India's standards for testing and accepting gold, such as jewelry, coins, scrap, etc.

- There are certain provisions for NRIs to open accounts with repatriation rights, which allows NRIs to track their interest on an expeditious basis. All banks participate under an established lender group with public sector banks being represented nationally.

Additional Perks And Extensions

A key contributing factor to the successful implementation of this scheme is the full value of gold that the scheme allows individuals to recycle, which will indirectly support the stability of the Indian Rupee.

Scheme participants are given first priority for service and access to electronic tracking for full transparency in participating. Partial withdrawals can be made after fulfilling the minimum period for holding gold and are based upon the remaining principal.

Common Concerns Addressed

- Common concerns such as purity are rare; as the tests are certified, and transit insurance is provided by the scheme.

- Gold will not be melted unless asked by the depositor. All forms of difficulty experienced with the current methods of holding gold for long periods will not apply to the scheme.

- You can track your transactions through e-banking or passbooks successfully.

Conclusion

Here’s the thing: most households treat gold as an emotional asset, not a financial one. The gold monetization scheme changes that. Instead of letting jewellery sit idle in lockers, you can convert it into a productive asset that earns interest, enjoys tax advantages, and supports the broader economy.

If you’re someone who values steady returns and smarter asset allocation, GMS can complement your overall portfolio rather than replace physical gold entirely. It adds structure, safety, and income to something that would otherwise just sit there.

And while GMS helps you unlock value from existing gold, platforms like Grip Invest make it easier to explore other fixed-income opportunities alongside it. That way, you’re not just relying on one asset class — you’re building a more balanced, income-focused strategy with clarity and control.

FAQs

1. What is the purpose of the Gold Monetisation Scheme?

The government offers a deposit facility to keep gold that can be utilized productively and create jobs at the local level.

2. Who is eligible to deposit into the Gold Monetisation Scheme?

Individuals who have a minimum quantity of gold and prove its genuineness through a bank certificate of at least 0.5% purity.

3. Are there taxes on the interest generated from gold deposits in a Gold Monetisation Scheme?

No, the Gold Monetisation Scheme is exempt from federal income tax.

4. Can I deposit gold jewellery with stones or only plain gold?

Yes, jewellery can be deposited, but stones and other non-gold components are removed during purity testing. Interest is paid only on the net pure gold content.

5. What happens to my gold after I deposit it under the gold monetization scheme?

Once tested and accepted, the gold is refined and monetized by banks, typically lent to jewellers or used for other approved purposes, while you earn interest on the deposited quantity.

6. Can I withdraw my gold before maturity?

Premature withdrawal is allowed after a minimum lock-in period, but it may attract penalties or reduced interest depending on the tenure selected.

References:

1. Bajaj finserv, accessed from: https://www.bajajfinserv.in/what-is-gold-monetization-scheme

2. Shri ram finance, accessed from: https://www.shriramfinance.in/articles/gold-loan/2026/what-is-a-gold-monetisation-scheme

3. Poonawaala fincorp, accessed from: walhttps://poonawallafincorp.com/blogs/gold-loan/gold-monetisation-scheme-eligibility-process-benefits

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001