HUF Account Benefits: Tax Savings And Wealth Planning Explained

As per the definitions laid down by the tax regulations in India, an HUF is a separate legal entity that facilitates capital deployment and offers deductions under Sections 80C and 80D of the Income-tax Act, 1961. Due to its tax-planning features, it has been widely adopted by Indian families for financial planning and getting several benefits, including direct tax optimisation and wealth generation.

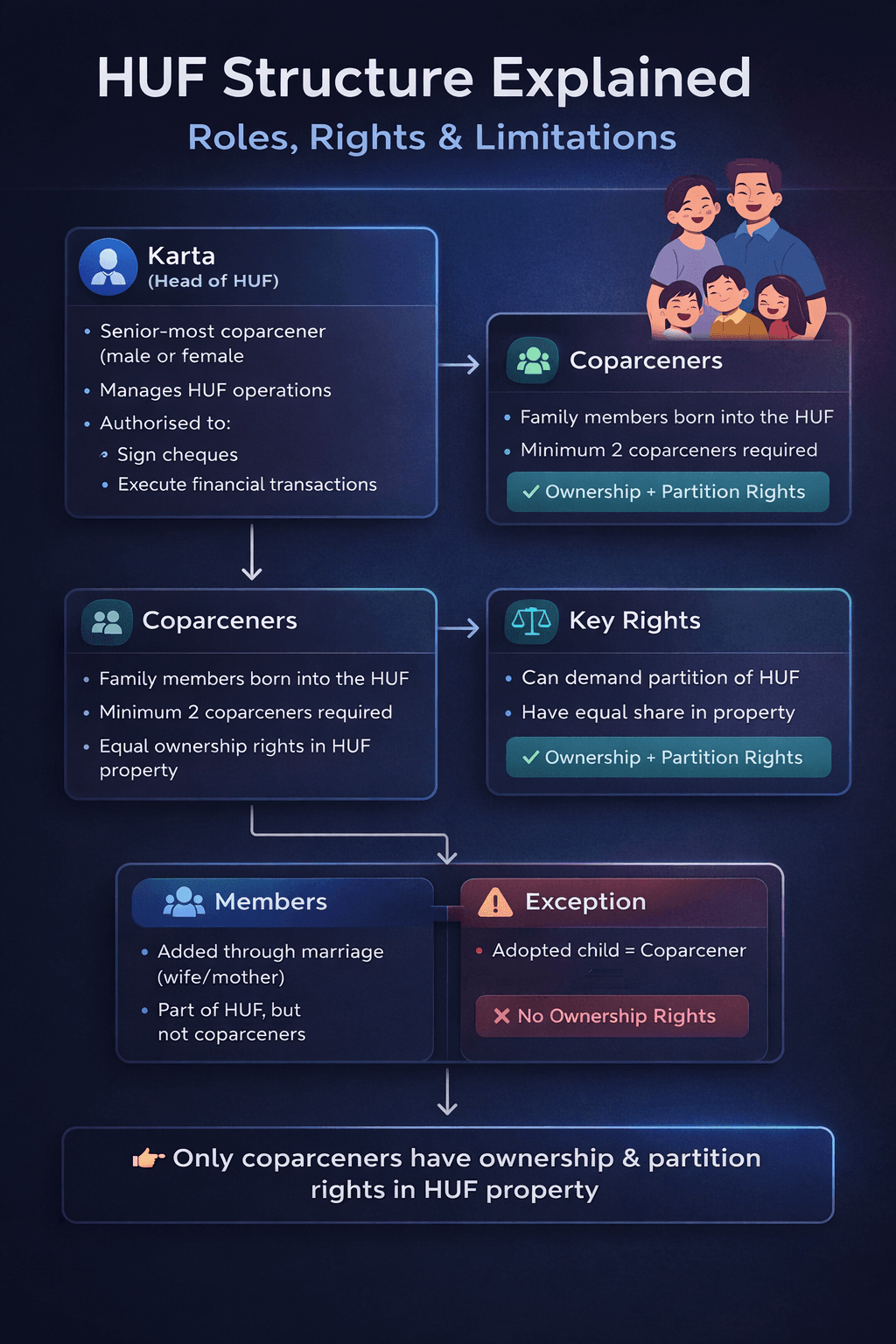

The HUF comprises coparceners (lineal descendants of a common ancestor) and their spouses and unmarried daughters (married daughters are coparceners since 2005). The HUF is managed by the Karta, typically the senior-most male (females eligible since 2016 amendment), who oversees financial decisions.

HUF accounts enable multiple exemptions and deductions per family. It can prevent family income from falling into higher tax brackets and help distribute income among family members based on their tax identities. Let’s understand the HUF meaning and the other factors that help families generate wealth and secure tax benefits in the long run.

Key Benefits Of HUF Account

In India, a Hindu Undivided Family (HUF) offers families earning income from multiple sources, such as real estate, businesses, or investments, a structured way to manage their finances. It enables better tax efficiency, facilitates income distribution, and allows for the legal segregation of family assets.

1. Tax savings

The HUF tax benefits in India include the ability to claim tax exemption for each individual member. HUF enjoys the same basic exemption limit as individuals (INR 2.5 lakh old regime). It offers a separate INR 1.5 lakh Section 80C deduction (old regime only), potentially doubling family savings.

2. Income Splitting

Income splitting is a key feature of an HUF (subject to clubbing provisions of Section 64), allowing families to transfer income-generating assets to the HUF structure and optimise their overall tax liability. The income is then taxed in the hands of the HUF rather than in the hands of an individual, making it a commonly used approach in India for achieving tax efficiency at the family level while remaining compliant with tax laws.

3. Separate entity

The HUF separate tax entity is governed by its own PAN number, bank account and financial identity. This separate identity enables families to plan for finances, file taxes and make investment decisions. In addition, regarding risk management, it creates distinct assets and obligations that do not affect family members.

4. Tax Planning Using HUF

When planning taxes for an HUF, the plan should include strategies to allocate income, maximise deductions, and manage assets to minimise overall tax liability while complying with national tax guidelines and regulations.

5. Strategic Use Of HUF For Tax Efficiency

HUF tax planning focuses on leveraging its separate tax status to minimise the family’s tax burden. Income may be earned by conducting businesses, investing, or owning property.

6. Utilisation of Section 80C Deduction

The HUF Section 80C deduction is up to INR 1.5 lakh (as per the old tax regime). Premium payments for life insurance policies and principal repayments for home loan schemes fall under this provision.

A joint strategy in which both individuals and HUFs maximise their deductions under Section 80C will be quite useful.

7. Leveraging Basic Exemption Limit

The HUF basic exemption limit is INR 2.5 lakh (old tax regime); e.g., income up to INR 2.5 lakh is tax-free (New regime: INR 3 lakh, no 80C). For instance, if the HUF earns income of up to INR 2.3 lakh from investments, it attracts no tax liability, effectively enhancing the family’s overall tax-free income.

Limitations Of HUF

However, while HUF has its advantages, it is important to recognise certain limitations of the structure before implementing it.

1. Restricted Membership

Individuals who belong to Hindu, Jain, Sikh, or Buddhist families are only eligible to form an HUF. An HUF cannot be created by an individual; it requires at least two people. However, it can also be created upon marriage.

2. Complexity in Partition

Partitioning an HUF is a complicated procedure, and once the property has been distributed, tax advantages will no longer be available.

3. Clubbing Provisions

Some transactions made in favour of the HUF may be subject to clubbing rules under the Income Tax Act.

4. Limited Flexibility

Compared with other entities, such as corporations, it provides less room for ownership transfer and governance.

Investment Options for HUF

HUFs can invest across a range of asset classes, including equities, mutual funds, and fixed-income instruments. This enables them to build a well-diversified portfolio aligned with their risk-return profile and long-term wealth creation goals.

1. Equity Investments

HUFs can directly invest in equity markets. However, it can also create risk due to market volatility, but it can help in capital appreciation and dividend income. So if a HUF invests some amount in stocks to generate long-term capital gains, it can avail of concessional tax rates.

2. Mutual Funds

Mutual funds are an ideal investment channel for HUFs due to their diversification and expert management. There are equity funds, debt funds, and hybrid funds that suit different levels of risk tolerance.

Systematic Investment Plans (SIPs) can also be created using HUFs for systematic investments and compound returns.

3. Fixed Income Instruments

Fixed-income securities include fixed deposits, bonds, and treasury bills, which yield a stable rate of return. Such assets play an important role in preserving capital and ensuring liquidity.

Building Wealth Through HUF

The core strength of an HUF lies in its ability to accumulate wealth through disciplined investing, tax efficiency, and strategic allocation across asset classes. This structure encourages a long-term approach to financial growth while facilitating seamless intergenerational wealth transfer.

An HUF also enables families to consolidate their resources into a unified pool, allowing for larger and more diversified investments than would typically be possible at an individual level. This collective approach enhances both scale and efficiency in wealth creation.

By incorporating stable fixed-income avenues, such as those available through platforms like Grip Invest, an HUF can generate predictable income streams that help cushion the impact of market volatility. This aligns well with a balanced investment philosophy, where returns are optimised in line with the level of risk undertaken.

FAQs On HUF Account Benefits

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001