Insurance Companies In India: Types, Top Players And How To Choose

The role of insurance is critical in an individual's personal financial management. For businesses, insurance is one of the most important aspects in ensuring the highest standards of risk management.

The insurance sector covers life, health, and property, safeguarding individuals (or their survivors) against financial hardship. Over the past couple of decades, the number of companies in the sector and the percentage of the population insured have increased significantly.

However, there is still almost 38% of the Indian population uninsured or underinsured in one way or another1. This implies that despite the progress, there is a tremendous scope and work to be done for Indian insurance companies.

In the past few years, the number of insurance companies in India has grown significantly, offering services through digital and conventional platforms. The entire insurance process has become easier and more streamlined.

Let us find out which types of insurance are offered by these companies, which are the top players, and what criteria you must follow while choosing your insurance provider.

Types Of Insurance Companies

1. Life Insurance Companies

It is one of the simplest kinds of insurance policies, with a very high premium-to-benefit ratio. Products include term insurance, endowment plans, and ULIPs. While some policies combine savings and protection, pure term plans focus solely on risk coverage, making them more cost-effective.

If the policyholder passes away during the tenure (coverage period) of a life insurance policy, the insurance company pays a pre-agreed sum to their survivors. The life insurance company charges a premium in exchange for this coverage. The premium could be monthly, quarterly or annually.

2. General Insurance Companies

General insurance companies cover non-life risks such as motor, property, travel, liability, and health insurance for individuals. Even though health insurance is often categorised as a different set of insurance in common parlance, it is discussed later.

If you are looking for a general insurance companies list in India, it would include both public and private players offering motor and asset-based protection products.

3. Health Insurance Companies

Health insurance companies insure the health of an individual and their family members (nominated). Health insurance can also be extended to members of an organisation through corporate health insurance plans. In exchange for a periodic premium, the health insurer agrees to cover medical expenses such as hospitalisation, IPD, OPD, and preventive healthcare (based on the terms and conditions of the policy).

When evaluating options, referring to the IRDAI insurance companies (health insurance) list helps identify authorised and regulated providers.

Top Insurance Companies In India

Public vs Private Players

Indian consumers can choose from a wide range of public and private players providing the highest quality of insurance services. In life insurance, LIC (Life Insurance Corporation of India) is the largest public-sector insurance company, dominating the market due to its size, history, and scale. The private sector includes some of the trusted names, starting with Tata AIA, Axis Max, and HDFC Life Insurance.

The debate around private vs public insurance in India often comes down to trust versus efficiency: public players are seen as stable, while private insurers are known for faster service, better customer support, and product innovation.

Key Players

If we talk about the list of top insurance companies in India, there are some prominent names besides LIC, such as HDFC Life Insurance Company, SBI Life Insurance Company, and ICICI Prudential Life Insurance. In the general insurance space, some of the most popular insurance companies are New India Assurance Company, ICICI Lombard General Insurance, and Bajaj Allianz General Insurance.

Standalone health insurers such as Star Health, Allied Insurance and Niva Bupa Health Insurance have also grown rapidly.

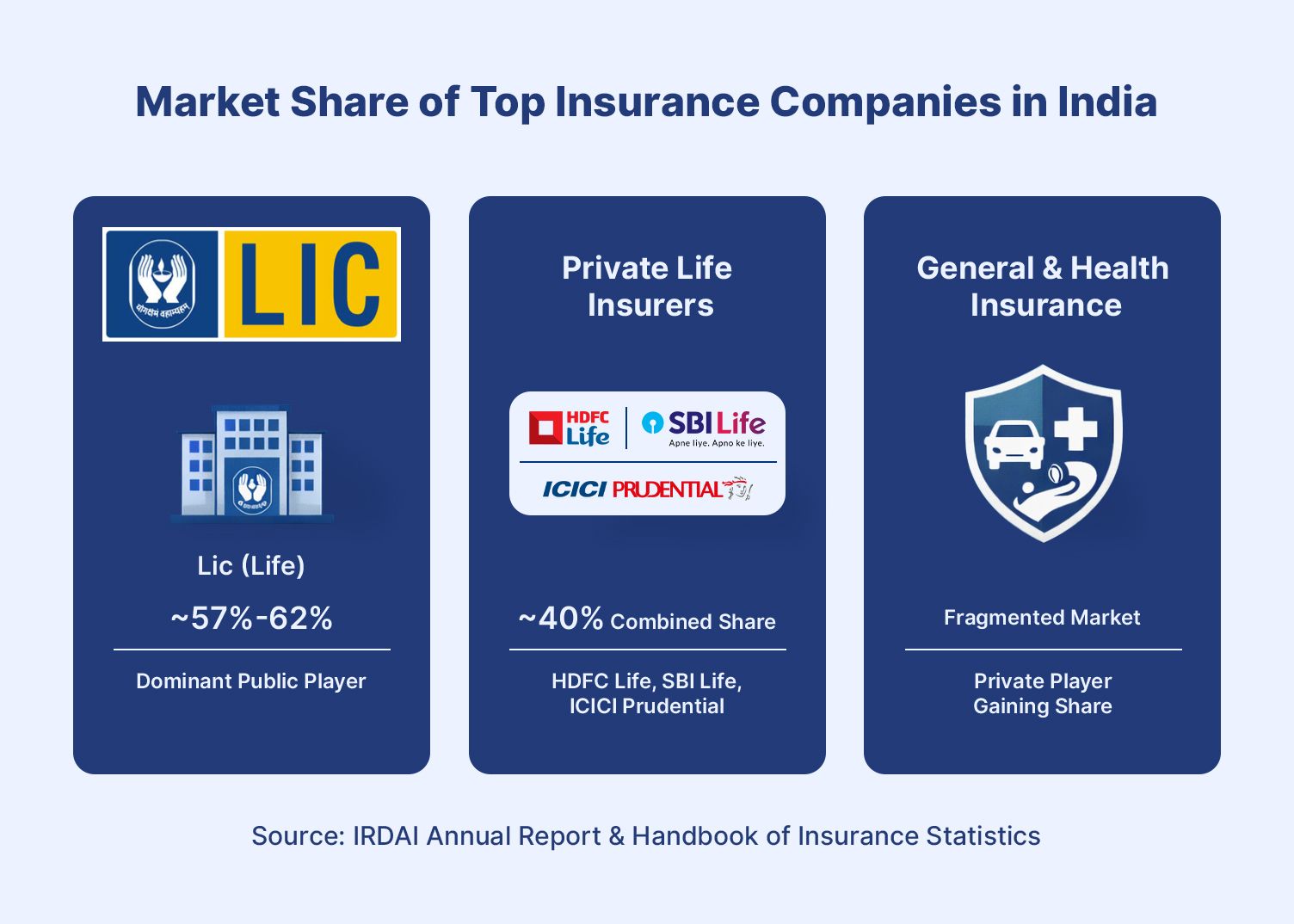

Market Share Overview

Here is the graph showing the market share enjoyed by different private and public sector insurance companies in the Indian market.

How Insurance Companies Make Money

Premium Collection

The most common way of generating revenue and profitability is through premium collection. The premiums are calculated based on customers' risk profiles, and companies maintain underwriting margins while paying claims from the pools.

Investment Income

The collected premium pool is further invested in bonds, equities, and other investments. This implies that insurance companies have a float or corpus that continues to grow even as regular payments are withdrawn from it in the form of insurance claims.

How To Choose The Right Insurance Company

1. Claim Settlement Ratio

The claim settlement ratio in India is a key metric for evaluating life insurance companies. It shows the percentage of claims settled by an insurer. A high ratio indicates that a company has paid a large number of claims with a low rejection rate. Indian insurance companies generally boast a very high CSR.

2. Solvency Ratio

It refers to the financial position and solvency of an insurance company. As per IRDAI norms, insurance companies operating in the market should maintain a minimum solvency ratio of 1.50, indicating no liquidity risks in the short- and long-term.

3. Customer Experience & Product Fit

The best life insurance companies in India need not be the largest ones, but those that align with your exact insurance needs. You should consider ease of claim processing, network hospitals (health insurance), number of affiliated workshops (motor insurance), and other policy features before making the decision.

Insurance vs Investment

There are a few endowment-based life insurance policies that have been sold conventionally as ‘investments’ to investors with a low risk appetite. However, with better knowledge and understanding of personal financial management, one thing is clear: insurance is not an investment (and vice versa). Both of them are an integral part of your financial planning, but must not be confused with each other.

You do need insurance to provide a financial blanket, protect your savings and investments, and support your family in critical circumstances.

However, if you are looking for low-risk investment options, the best choice would be fixed income securities (such as corporate bonds) as offered by Grip Invest, which you can combine with term and health insurance for comprehensive financial protection of yourself and your family.

Conclusion

Insurance plays a critical role in building a strong financial foundation by protecting individuals and businesses from unexpected risks. With a wide range of insurance companies in India offering life, health, and general coverage, choosing the right provider depends on factors such as claim settlement ratio, solvency, product fit, and overall customer experience.

Understanding the difference between public and private insurers can further help in making an informed decision based on your priorities.

At the same time, it is important to remember that insurance and investment serve different purposes. While insurance safeguards your financial well-being, wealth creation requires separate, well-planned investment strategies across asset classes.

A balanced financial plan should combine adequate insurance coverage with diversified investments to achieve both protection and growth over the long term.

Platforms like Grip Invest can complement this strategy by offering curated fixed-income opportunities, helping you build stable and predictable returns alongside your insurance planning.

FAQs On Insurance Companies In India

References:

1. Insurance Asia, accessed from: https://insuranceasia.com/insurance/news/over-38-indians-remain-uninsured-despite-sector-growth

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001