LIC FD Explained: Features, Returns, And Should Investors Consider It

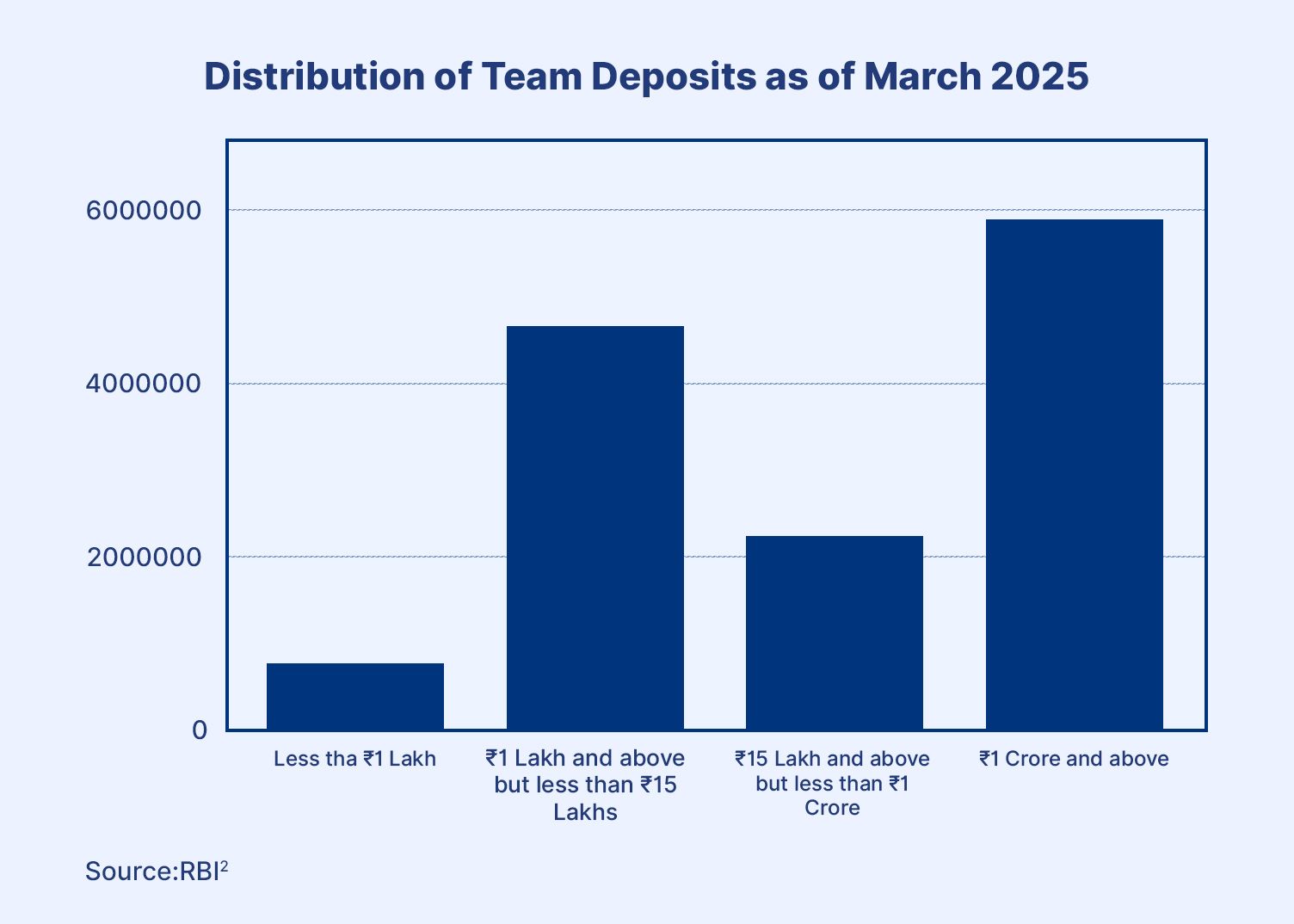

Fixed Deposits have been a popular investment medium among Indian investors primarily due to their fixed and stable income-earning opportunity and low-risk profile. According to reports, fixed deposits or bank deposits grew 10.6% year-on-year as of March 20251.

Growth was higher in the previous fiscal year, at 13%. Furthermore, at 59.5%, FDs account for the largest share of total deposits held by banks as of March 2025.

The table we have provided below highlights the FDs held across different valuations, indicating that the popularity of FDs is not restricted to a particular economic group.

Although FDs are popular, they often suffer from key hurdles like insufficient returns. Therefore, investors need to comparatively analyse the diverse FD schemes offered by different banks to choose one with the most optimal features.

Thus, to help investor research into FDs, this blog decodes a key FD plan offered by the Life Insurance Corporation (LIC) of India. Analysing the LIC FD through the LIC FD returns, benefits, risks, etc., whilst comparing it with other FD schemes, can aid informed investing.

What Is LIC FD?

The LIC Housing Finance Limited offers three types of fixed deposits; each caters to investors of different kinds. Let us take a closer look at the LIC FD tenure and eligibility through these three categorisations to understand what it actually means to have an LIC Housing Finance FD.

1. Sanchay Public Deposit Scheme

Launched in May 2007, the Sanchay Public Deposit is an LIC FD scheme, chosen by regular, retail investors3. The LIC FD credit rating is CRISIL AAA/Stable. The deposit can be made by resident individuals, partnership firms, cooperative societies, and more.

Even minors can have this FD through their guardians.

2. Corporate Deposit Scheme

Unlike Sanchay LIC FDs, the corporate deposits are not for individual investors4. They are targeted towards public limited companies, private limited companies, corporations, statutory boards, other banks, financial institutions, etc., meaning institutions of usually larger scale. However, similar to Sanchay FDs, the Corporate FDs or LIC are also rated CRISIL AAA/Stable. The points below explain some of the other features of these FDs.

3. Green Deposit Scheme

The RBI released the Green Deposit Framework to encourage banks, Non-Banking Finance Companies (NBFCs), and Housing Finance Companies (HFCs) to offer deposits to the public that can help fulfil their sustainability goals5.

Such deposits pool investor funds to direct their flow as credit into green initiatives or environmentally friendly, sustainability-specific initiatives. These schemes also safeguard depositor interests, address concerns about greenwashing, and more.

The table below highlights some other key features of LIC FDs in general that are common across schemes.

Also Read: LIC Housing Finance: Home Loan Interest Rates, Eligibility, And Benefits

| Particulars | Description |

| Minimum deposit | Investors can start their deposits with INR 20,000. They can even choose to increase in steps of INR 1,000. |

| Tenure | The flexible tenure ranges from 1 Year, 15 Months, 18 Months, 2 Years, 3 Years, or 5 years |

| Credit Approval against FD | Investors can get a loan of up to 75% of the deposit sanctioned fast against this LIC FD. |

Now that we understand the key features of an LIC FD, let us explore the LIC HFL FD rates 2026.

LIC FD Interest Rates And Returns

Retail investors can choose the Sanchay Public Deposit to make an LIC FD. Like any fixed deposit scheme, the LIC FD can be cumulative and non-cumulative.

While cumulative FDs reinvest the interest, thereby repaying the principal and compounded, accumulated interest together at maturity, non-cumulative interest pays out the interest at regular intervals, like monthly or quarterly.

Provided below are the LIC FD cumulative vs non-cumulative interest rates.

- Cumulative Interest Rate

Investors who want to maximise their wealth choose cumulative interest so that their interest gets reinvested and earns compounding interest. These investors get their principal and interest together on maturity.

| Term | Up to INR 3 Crores | Above INR 3 Crores |

| 1 Year | 6.70% | 6.60% |

| 15 Month | 6.75% | 6.65% |

| 18 Months | 6.75% | 6.65% |

| 2 Years | 6.80% | 6.80% |

| 3 Years | 6.85% | 6.85% |

| 5 Years | 6.90% | 6.90% |

Source: PaisaBazaar6

- Non-Cumulative Interest Rate

Investors who want to generate a passive, periodic income choose non-cumulative fixed deposits, which pay out the interest periodically.

| Term | Up to INR 3 Crores Monthly | Above INR 3 Crores Monthly | Up to INR 3 Crores Quarterly | Above INR 3 Crores Quarterly |

| 1 Year | 6.50% | 6.40% | 6.55% | 6.45% |

| 15 Month | 6.55% | 6.45% | 6.60% | 6.50% |

| 18 Months | 6.55% | 6.45% | 6.60% | 6.50% |

| 2 Years | 6.60% | 6.60% | 6.65% | 6.65% |

| 3 Years | 6.65% | 6.65% | 6.70% | 6.70% |

| 5 Years | 6.70% | 6.70% | 6.75% | 6.75% |

Source: PaisaBazaar6

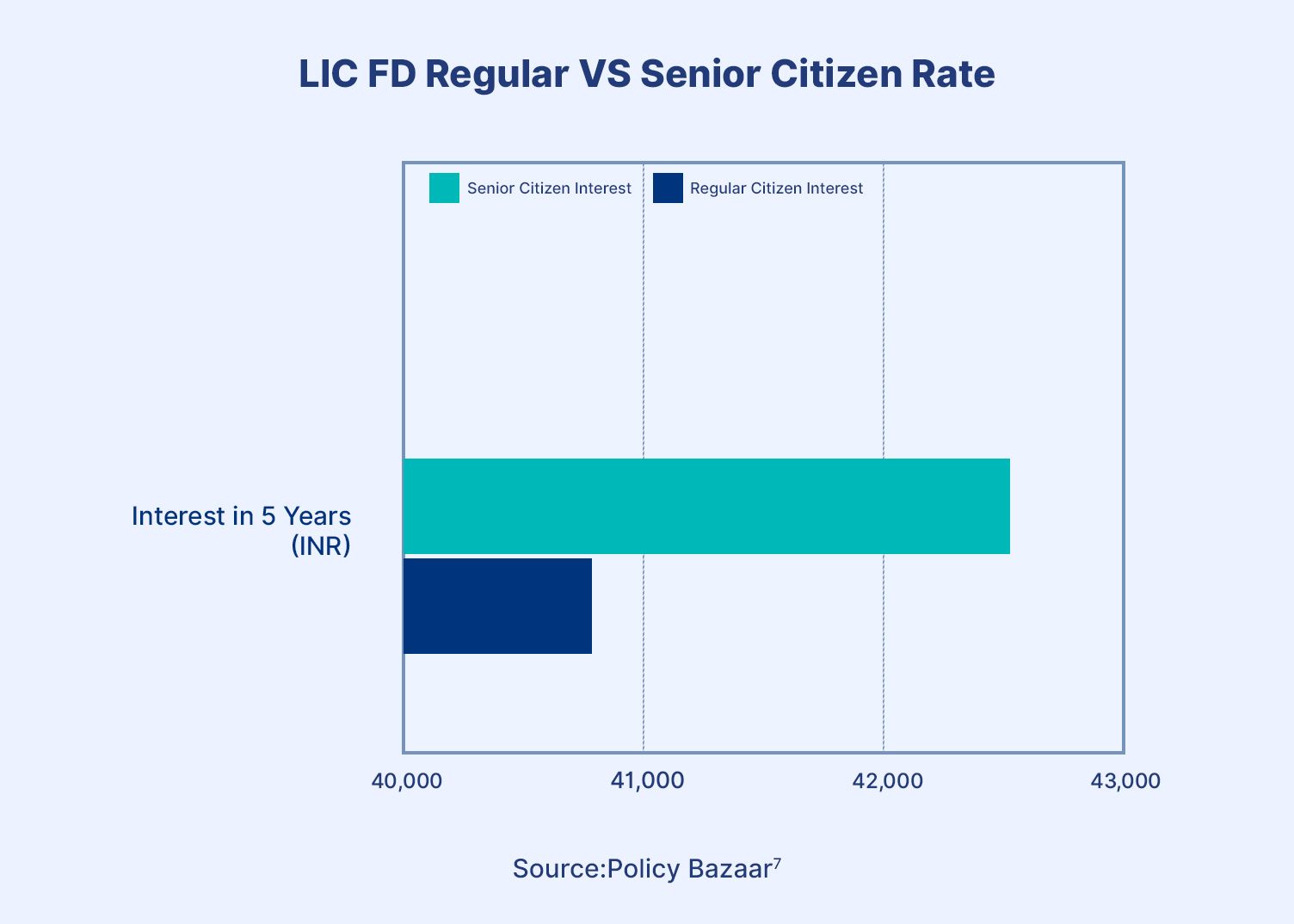

The LIC FD interest rates for senior citizens are also higher than those for regular citizens. Senior citizens receive an additional 0.25% p.a. in interest, over and above the regular rate on all tenures. Let us take an example to understand this in detail.

Suppose Mr K invested INR 1,00,000 in the LIC FD for 5 years. Assuming a cumulative interest rate, if Mr K were a regular citizen, he would have earned a 6.90% p.a. interest. Therefore, his interest would be INR 40,784.

However, had he been a senior citizen, he would have earned an extra 0.25% interest, making the total interest rate 7.15%. In such a scenario, he would have earned INR 42,524.

Interest stability is the key feature of fixed deposits that makes them beneficial and suitable for various investors. A closer look at the benefits of an LIC FD might help investors make a comprehensive analysis.

Benefits Of LIC Fixed Deposit

Discussed below are the key benefits of an LIC FD.

- Stable returns: The LIC fixed deposit scheme provides investors with the opportunity to earn passive income. The interest rates of FDs do not change, despite market fluctuations.

- LIC Housing Finance FD monthly income plan: When investors choose a non-cumulative interest, they can generate a passive income from their FD investment.

- Trusted financial institute: LIC is not only a government agency, but also has a strong brand value. The company is a trusted corporation, resulting in investor confidence.

However, there are certain risks and factors that investors must consider before investing.

Also Read: Joint Home Loan Tax Benefit: How Co-Borrowers Can Save More Tax

Risks And Things To Consider

Discussed here are the key factors that investors must consider before choosing a fixed deposit.

1. Liquidity: An investor cannot withdraw their principal from an FD without paying a penalty, despite interest being cumulative or non-cumulative. According to the LIC HFL FD premature withdrawal rules, an investor gets no interest if an FD is withdrawn within 3 months. If the withdrawal is made after 3 months but up to 6 months, individual depositors get only 3% interest.

However, for withdrawal after 6 months, the rate of interest will be 1% lower than the rate at which the deposit is actually held.

For example, Mr N made an FD for 3 years at 6% interest, but her prematurely withdrew after 2 years. If the rate of interest for 2-year deposits were 5%, Mr N would receive 4% interest (5% - 1%).

2. Interest rate changes: Once a fixed deposit is made at a certain interest rate, the rate does not change, despite reforms in the rate structure. For instance, if Mr P made an FD for 5 years at 7% interest, but the bank changes the 5-year rate to 6%, Mr P would continue to earn 7% interest.

While this is an advantage when the rates fall, it is a risk when rates increase. If the bank increases its interest rate, an FD created at a previous lower rate will continue to earn a lower interest rate.

Therefore, before making an FD, an investor should use an LIC FD calculator online to anticipate the amount of return they can expect. Furthermore, the LIC FD tax implications are the same as any FD, meaning the return is taxed at the applicable tax slab.

However, another key concern is that the FD interest, even the LIC FD rate, often ranges from 6-7%, which might not be enough to meet inflation and market expectations. In such a scenario, high-yield corporate FDs on Grip can offer 8-10% interest.

Also Read: Personal Loan Interest Rates In India: What Determines Your Loan Cost

Conclusion

LIC FD remains a reliable option for investors seeking predictable and stable returns, especially in uncertain market conditions. With interest rates ranging between 6.70% and 6.90%, a low minimum investment of INR 20,000, and flexible tenures from 1 to 5 years, it caters well to conservative investors. The CRISIL AAA rating and LIC’s strong credibility further add to its appeal.

However, while safety and consistency are key strengths, returns may not always outpace inflation. This makes it important for investors to compare options and align investments with their financial goals and risk appetite.

For those looking to complement stable FDs with potentially higher returns, Grip Invest offers access to fixed-income opportunities with yields in the 8–12% range, helping build a more balanced and growth-oriented portfolio.

FAQs

1. What is a LIC fixed deposit?

The Life Insurance Corporation of India offers three key fixed deposit schemes, namely the Sanchay Public Deposit Scheme, the Corporate Deposit Scheme, and the Green Deposit Scheme. These schemes offer a fixed return to investors against their principal, like any other FD scheme. Deposits start from INR 20,000, with flexible tenures like 1 year, 15 months, 18 months, 2 years, 5 years, etc.

2. Is LIC FD safe?

Any fixed deposit scheme carries fixed interest despite market fluctuations. Furthermore, every deposit is insured up to INR 5,00,000 by the Deposit Insurance and Credit Guarantee Corporation (DICGC), a subsidiary of RBI. Furthermore, LIC is one of the most-trusted brands, with decades of experience. However, caution and optimal research are key.

3. What are LIC FD interest rates?

The LIC interest rates vary across the three different schemes, namely the Sanchay Public Deposit Scheme, the Corporate Deposit Scheme, and the Green Deposit Scheme. Cumulative rates for Sanchay FDs, the one most commonly used by individual investors, have interest rates starting from 6.70% for deposits below INR 3 crores, as of 18 March 2026. Interest on deposits above INR 3 crores starts from 6.60%.

References:

1. ET, accessed from: https://economictimes.indiatimes.com/industry/banking/finance/banking/bank-deposits-grew-by-10-in-fy25-growth-decline-from-13-recorded-in-fy24-rbi-data/articleshow/121566544.cms?from=mdr

2. RBI, accessed from: https://data.rbi.org.in/BOE/OpenDocument/2409211840/OpenDocument/opendoc/openDocument.jsp?logonSuccessful=true&shareId=0

3. LIC Housing, accessed from: https://www.lichousing.com/sanchay-public-deposit

4. LIC Housing, accessed from: https://www.lichousing.com/corporate-deposits

5. LIC Housing, accessed from: https://www.lichousing.com/green-deposits#renewalrepayment

6. PaisaBazaar, accessed from: https://www.paisabazaar.com/fixed-deposit/cumulative-vs-non-cumulative-fd/

7. PolicyBazaar, accessed from: https://www.policybazaar.com/lic-of-india/lic-fd-interest-rates/

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001