Joint Home Loan Tax Benefit: How Co-Borrowers Can Save More Tax

Buying a home is one of the biggest financial decisions most Indians will ever make. The sheer size of the commitment — often spanning 20 to 30 years — can feel daunting. But here is an angle that many homebuyers overlook: a joint home loan does not just split the repayment burden; it can effectively double your tax savings.

Whether you are planning to co-borrow with your spouse, a parent, or a sibling, understanding the tax benefits available on a joint home loan can unlock significant savings every year. Let us break this down clearly — with numbers, charts, and actionable insights.

Did You Know? A couple jointly taking a home loan can claim up to INR 10 lakh in total annual deductions — nearly double what a solo borrower gets. This alone can translate into tax savings of INR 3,00,000+ per year at the 30% tax slab.

Tax Benefits Available On Joint Home Loans

The Indian Income Tax Act offers multiple avenues for home loan tax relief. Co-borrowers on a joint home loan can each independently claim the following deductions:

1. Section 24(b) — Deduction on Interest Paid

Each co-borrower can claim up to INR 2,00,000 per year on home loan interest for a self-occupied property.

For a let-out property, there is no upper limit, though set-off of losses is capped at INR 2 lakh per year against other income heads.

2. Section 80C — Deduction on Principal Repayment

Each borrower can claim up to INR 1,50,000 per year on the principal component of their EMI.

This INR 1.5L ceiling is shared across all Section 80C investments — PPF, ELSS, life insurance — so plan your contributions accordingly.

3. Section 80EE — Additional Deduction (Loans Sanctioned Apr 2016 – Mar 2017)

First-time homebuyers with loans sanctioned in this window can claim an extra INR 50,000 per year over and above the Section 24(b) limit. The loan amount must not exceed INR 35 lakh and property value must not exceed INR 50 lakh.

4. Section 80EEA — Extended First-Time Buyer Benefit (Apr 2019 – Mar 2022)

For home loans sanctioned between April 2019 and March 2022, eligible first-time buyers can claim an additional INR 1,50,000 per year under Section 80EEA, provided the stamp duty value of the property does not exceed INR 45 lakh.

Both co-borrowers can claim this benefit independently if each meets the eligibility criteria.

5. Stamp Duty & Registration Charges — Section 80C

Stamp duty and registration fees paid at time of purchase are deductible under Section 80C (subject to the INR 1.5L annual cap). Both co-owners can claim this in the year of purchase.

Table 1: Maximum Annual Tax Deductions — Single vs. Joint Home Loan

| Tax Section | Benefit Type | Single Borrower | Each Co-Borrower |

| Section 24(b) | Interest Deduction | INR 2,00,000 / yr | INR 2,00,000 / yr |

| Section 80C | Principal Repayment | INR 1,50,000 / yr | INR 1,50,000 / yr |

| Section 80EEA | Additional Interest (FTB) | INR 1,50,000 / yr | INR 1,50,000 / yr |

| Stamp Duty (80C) | One-time Deduction | INR 1,50,000 (cap) | INR 1,50,000 (cap) |

| TOTAL POTENTIAL | Combined Annual Savings | INR 3,50,000 / yr | INR 7,00,000 / yr |

Conditions To Claim Joint Home Loan Tax Benefits

Tax benefits on a joint home loan are not automatic. Every co-borrower must satisfy three essential conditions:

Condition 1 — You Must Be a Co-Owner of the Property

Being a co-borrower on the loan is not enough on its own. Each person wishing to claim deductions must also be a registered co-owner in the sale deed or title documents.

A guarantor or a co-borrower without an ownership stake cannot claim deductions.

| Common Mistake: Many couples take joint loans for eligibility purposes but register the property only in one name. This means only one person can claim tax benefits. Always ensure both co-borrowers are co-owners in the property title documents. |

Condition 2 — Each Co-Borrower Must Actually Repay

Deductions are available only to the extent each borrower repays from their own funds. Maintain clear bank records — ideally have EMIs auto-debited proportionally from each borrower's account. Repayment by one person claimed by another is not permissible.

Condition 3 — Individual Deduction Caps Apply

The Section 24(b) cap of INR 2,00,000 and Section 80C cap of INR 1,50,000 apply per individual — not per loan. Each borrower independently claims their deduction up to these limits. Claims should ideally be in proportion to each person's actual repayment share.

Key Conditions To Claim Joint Home Loan Tax Benefits

To claim joint home loan tax benefit in India, each borrower must meet a few essential eligibility rules under the Income Tax Act.

1. Co-ownership of the Property

Both borrowers must be listed as co-owners in the property title or sale deed. A co-borrower without ownership cannot claim deductions.

2. Active Loan Repayment

Each borrower must contribute to EMI repayment from their own income. Tax deductions apply only to the portion actually paid.

3. Individual Deduction Limits Apply

Tax benefits are per person, not per loan. Each co-borrower can claim up to INR 2 lakh interest deduction (Section 24b) and INR 1.5 lakh principal deduction (Section 80C).

4. Old Tax Regime Requirement

Most joint housing loan tax benefits apply only under the old tax regime, as deductions like Section 24(b) and 80C are not available in the new regime.

5. Proportionate Claim Rule

If co-borrowers repay different EMI shares, deductions must be claimed in the same proportion as their repayment contribution.

Example Calculation Of Joint Home Loan Tax Savings

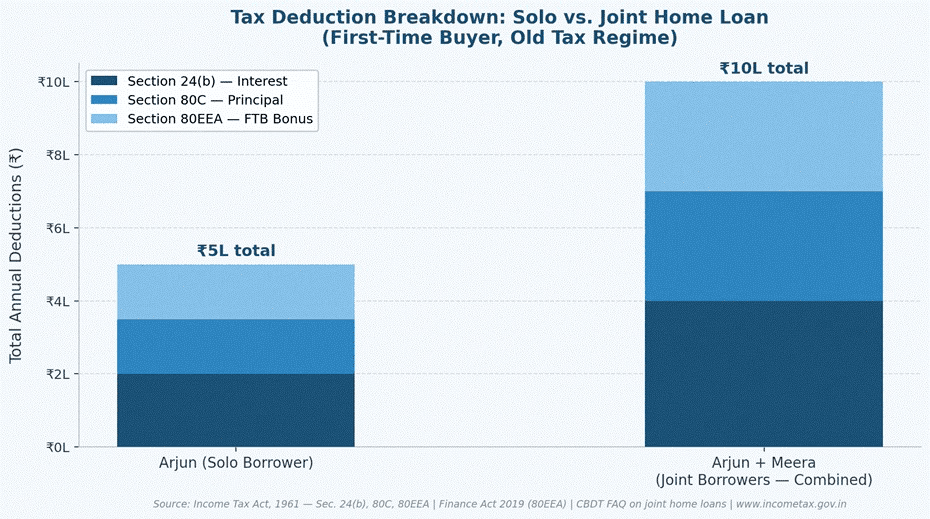

Hypothetical Scenario: Arjun (Software Engineer, INR 18 LPA) and Meera (School Teacher, INR 9 LPA), both first-time homebuyers, purchase a flat worth INR 42 lakh in Pune. They take a joint home loan of INR 35 lakh at 8.5% p.a. over 20 years. In Year 1, the interest component is approximately INR 2,92,000 and the principal component is INR 92,000.

Table 2: Tax Deduction Calculation — Arjun (Solo) vs. Arjun + Meera (Joint)

| Deduction Component | Arjun (Solo) | Arjun + Meera (Joint) |

| Section 24(b) — Interest | INR 2,00,000 | INR 2,00,000 × 2 = INR 4,00,000 |

| Section 80C — Principal | INR 1,50,000 | INR 1,50,000 × 2 = INR 3,00,000 |

| Section 80EEA — First-Time Buyer | INR 1,50,000 | INR 1,50,000 × 2 = INR 3,00,000 |

| Total Annual Deductions | INR 5,00,000 | INR 10,00,000 |

| Estimated Tax Saved (@ 30%) | ~INR 1,50,000 | ~INR 3,00,000 |

Chart 2: Deduction Breakdown — Solo vs. Joint (Stacked)

Note on the New Tax Regime: Under India's new tax regime (default from FY 2024–25 per Finance Act 2023), home loan interest under Section 24(b) and principal under Section 80C are not deductible.

Co-borrowers opting for the new regime forgo these benefits in exchange for lower flat tax rates. Individuals with large deduction claims are generally better served under the old regime. Always run a comparison or consult a qualified tax advisor.

Tax Planning Beyond The Home Loan: Building A Smarter Portfolio

Claiming your full home loan tax benefits is an excellent start — but smart investors do not stop there. The INR 1,50,000 Section 80C ceiling is shared across multiple instruments. If your principal repayment already exhausts your 80C limit, further ELSS or PPF contributions may not deliver additional tax relief — making strategic portfolio planning essential.

Here is how a joint home loan fits alongside other popular investment options:

Table 3: Portfolio Diversification — Home Loan vs. Other Investment Instruments

| Investment | Returns (Approx.) | Tax Benefit | Liquidity |

| Home Loan (Joint) | 8–10% (capital gain) | Up to INR 10L deductions/yr | Low |

| Corporate Bonds | 9–12% (fixed income) | Interest taxable | Medium-High |

| PPF | 7.1% p.a. (FY25) | Section 80C (INR 1.5L cap) | Low (15-yr lock) |

| ELSS Mutual Fund | Market-linked | Section 80C (INR 1.5L cap) | Medium (3-yr lock) |

| Grip Invest | 9–12% (target) | Diversified fixed income | High |

Investors who maximise home loan tax deductions often seek fixed income instruments to counterbalance the illiquidity and concentration risk that real estate brings to a portfolio. Corporate bonds and marketplace investment platforms offer predictable yields and greater liquidity — making them natural complements.

Grip's fixed income marketplace provides access to curated corporate bonds, securitised instruments, and other yield-generating products — helping investors balance their portfolios beyond the equity-real estate axis. Home loan borrowers increasingly deploy their tax savings through Grip to generate consistent, risk-calibrated returns.

Conclusion

A joint home loan is not just a strategy to boost loan eligibility or share EMI burden — it is one of the most powerful and fully legal tax optimisation tools available to Indian taxpayers. When structured correctly, with both parties being co-owners and co-repayers, a couple or family can double their annual tax deductions and potentially save lakhs over the loan tenure.

But the smartest borrowers know that tax savings are only the first step.

The money saved on taxes deserves to be put to work. Whether through fixed income instruments, diversified bonds, or structured marketplace products, channelling your home loan tax savings into the right investments can compound your wealth far beyond the property itself.

Grip Investment Platform offers a curated selection of fixed income and debt instruments — from high-grade corporate bonds to alternative fixed-yield products — that are ideal for home loan borrowers looking to diversify. With target returns between 10–14% p.a. and transparent risk disclosures, Grip bridges the gap between idle tax savings and purposeful wealth creation. Explore Grip Invest offerings to make every rupee of your tax benefit count.

FAQs On joint Home Tax Benefits

1. What is the tax benefit of a joint home loan?

Each co-borrower can independently claim deductions — up to INR 2,00,000 on interest (Section 24b) and INR 1,50,000 on principal (Section 80C). Two co-borrowers can therefore claim a combined maximum of INR 7,00,000 per year — and up to INR 10,00,000 if Section 80EEA also applies.

2. Can both borrowers claim a tax deduction on the same home loan?

Yes — provided both are co-owners of the property and each actually repays a portion of the loan from their own income. Claims should be in proportion to each person's repayment share, subject to individual limits.

3. What are the maximum deductions allowed on a joint home loan?

Per person: INR 2,00,000 under Section 24(b) for interest; INR 1,50,000 under Section 80C for principal; INR 1,50,000 under Section 80EEA for eligible first-time buyers. With two co-borrowers, the combined potential reaches up to INR 10,00,000 per year.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001