Modified Duration Vs Macaulay Duration: Key Differences Every Bond Investor Should Know

With an annual growth rate of approximately 12%, the outstanding corporate bond market in India witnessed a robust growth from INR 17.5 trillion in FY2015 to INR 53.6 trillion in FY20251. A key driver of this sustained growth is the fixed-income-driven capital growth in the bond market. However, successful bond investing depends on an optimal analysis of interest-rate risk in bonds.

The interest rate risk indicates the change in the market price of bonds due to a change in interest rates. When new bonds with higher interest rates enter the market, the market price of existing bonds falls. Similarly, a fall in interest rate results in a rise in the bond market value. Therefore, investors must understand how to ascertain bond price sensitivity through Modified duration vs macaulay duration analysis.

What Is Macaulay Duration?

Investors can anticipate the degree of change in the bond market price due to a change in its interest rates by analysing bond duration.

A bond pays periodic coupon payments and the principal on maturity. For example, Mr A invested INR 1000 in a 10% bond, which has a maturity of 3 years. The table below illustrates his total bond payout.

| Year | Nature of Reture | Amount (INR) |

| 1 | Interest | 100 |

| 2 | Interest | 100 |

| 3 | Interest and Principal | 1100 |

Therefore, bond payments arrive in instalments, rather than in one go. While the maturity period indicates the fixed date for principal repayment, duration in bonds analyses the average time required to recover the total bond payout (principal+interest).

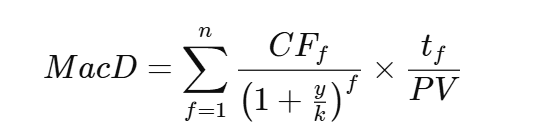

Subsequently, Macaulay duration measures bond duration by calculating the weighted average time required to recover the total anticipated cash flow of bonds, meaning the principal along with interest. To understand the Macaulay duration meaning, the analysis of its formula below is non-negotiable.

Where

- f is the cash flow number.

- CF is the cash flow amount

- y is the yield to maturity

- k refers to the yearly compounding period

- tf means the number of years before the cash flow is received

- PV means Present Value of all cash flows.

For example, if the Macaulay duration is 5 years, it implies that it will take 5 years to recover the investment. A higher Macaulay duration indicates a greater sensitivity to interest rates. Similarly, a lower Macaulay duration indicates a lower sensitivity to interest rates.

However, while Macaulay duration gives an overview of interest sensitivity, it does not indicate the specific percentage change in price with interest rate change. This is where the Modified duration comes into play.

What Is Modified Duration?

Modified duration converts Macaulay duration into price sensitivity. It indicates the specific percentage change in bond price for a 1% change in yield. The formula below can help further understand the Modified duration meaning.

| D mod= D1+y |

Where

- D indicates the Macaulay duration

- y refers to periodic yield to maturity

For example, if the Modified duration is 6, a 1% interest rate rise means a bond price can fall around 6%. Similarly, a 1% interest rate fall indicates a corresponding change 6% approximate change in bond price.

Therefore, while Macaulay duration refers to the average time required to recover the anticipated bond investment, Modified duration converts the Macaulay bond duration formula to analyse price sensitivity to interest rate.

However, a comparative analysis of Modified duration vs Macaulay duration is necessary to thoroughly analyse each concept and understand their use case in bond market investing.

Modified Duration Vs Macaulay Duration: Key Differences

The table below compares Modified duration vs Macaulay duration in detail based on different key parameters.

| Particulars | Macaulay duration | Modified duration |

| Meaning | Weighted average time to generate cashflows (Principal+Interest) from bond investment | Percentage change in price due to 1% change in the yield of bonds |

| Formula | ?(Time×PV of Cashflow)?/Bond Price | Macaulay / (1 + Yield) |

| Interpretation | A 6-year Macaulay duration means that it will take a particular bond investment 6 years to recover the principal and coupon (interest) | If the Modified duration is 6, a 1% yield increase will trigger 6% decrease in market price. Similarly, a 1% yield decrease can trigger a 6% increase in market price |

| Primary Use | Portfolio matching and immunisation to guarantee specific future cash needs | Ascertain individual bond risk by analysing their market price sensitivity to interest rate fluctuation |

A nuanced understanding of Modified duration vs Macaulay duration is incomplete without exploring the wider concept of how duration reflects interest rate risk. Although the meaning and interpretation of each metric is covered before, an overall interest rate impact with respect to duration must be understood for effective analysis.

How Duration Reflects Interest Rate Risk

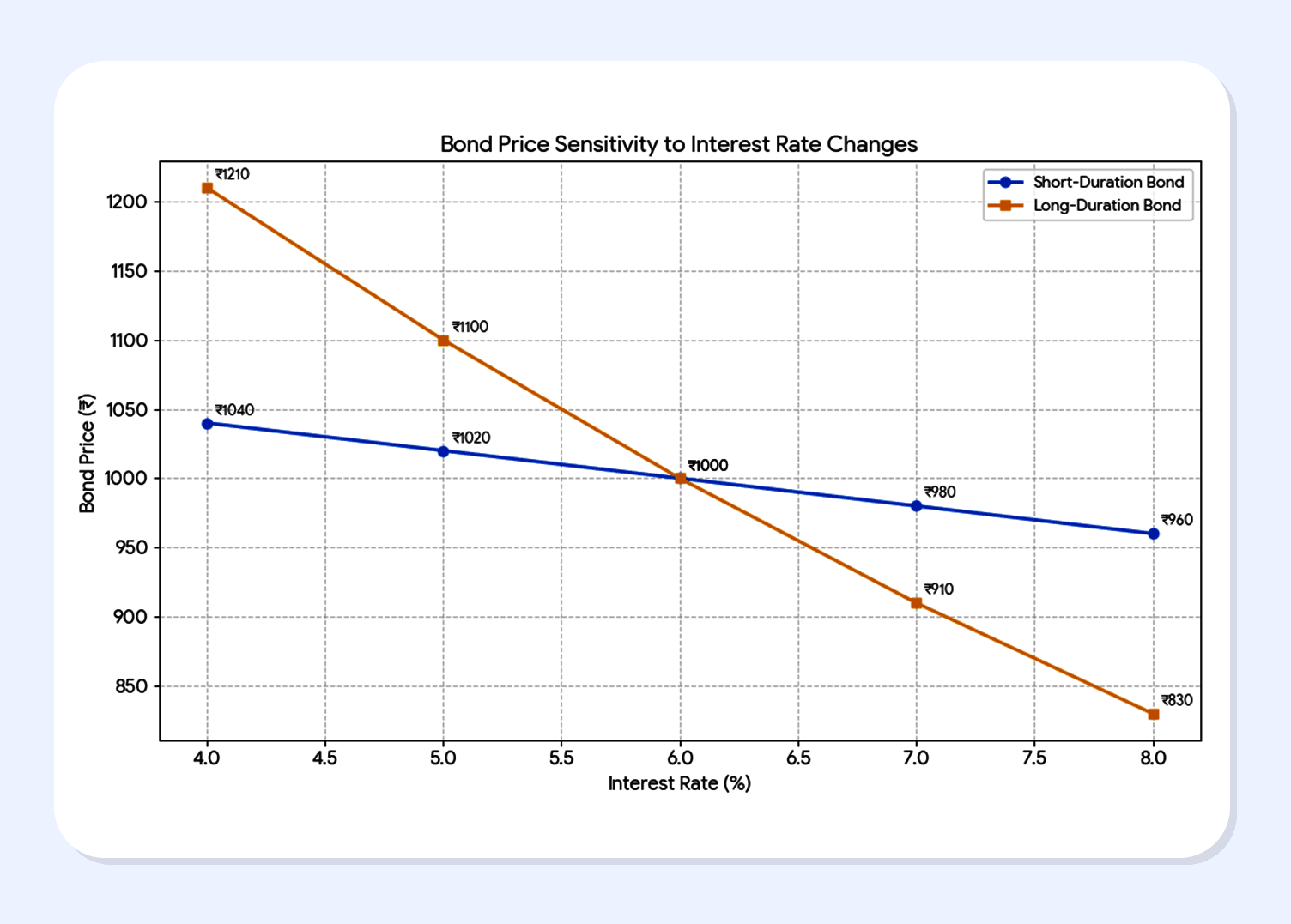

Let us take an imaginary situation to illustrate how duration reflects interest rate risk. The graph below illustrates the price response of a short-duration bond and a long-duration bond.

As the interest rate increases from 4% to 8%, the price of both bonds falls, indicating an inverse relationship between bond price and interest rate. However, the decline is sharper for the long-duration bond, indicating that for the same interest-rate movement, a change in long-duration bond price is greater than the change in short-duration bond price.

For example, when interest increased from 5% to 6%, the short-duration bond price fell by INR 20, but the long-duration bond price fell by INR 100.

Therefore, the steeper slope indicates a greater price sensitivity. Thus, in this case, duration reflects interest rate risk through the steepness of the price-yield line. Since duration measures how strongly the bond price reacts to interest rate movements, a flatter line (low duration) indicates lower interest-rate risk and a steeper line (higher duration) indicates greater interest-rate risk.

Given this understanding of the duration vs yield concepts, retail investors must explore their practical implementation for optimal bond market investing.

Practical Application For Retail Bond Investors

Retail investors can make bond investments either by directly investing in them or by investing in bond mutual funds. In either scenario, duration can help judge interest rate risk.

- Individual Bonds: In case the bond rates are expected to increase, choosing shorter-duration bonds can help because their prices fall less with a rate increase. Similarly, if the interest rate is expected to fall, long-duration bonds can offer higher capital gain because their price rises more when yields decline.

- Bond Mutual Funds: Since funds do not mature on specific dates and the Net Asset value (NAV) changes with market yield, duration becomes crucial. Short-duration funds anticipate lower volatility, while long-duration or gilt funds witness greater volatility. This is why investors aim to match fund duration with investment horizon. For instance, long-term investors prioritise capital growth and can sustain short-term volatility that eases over time, and thus, can choose long-term funds.

Optimal analysis of fixed income risk measures requires a holistic analysis of different parameters. Therefore, platforms like Grip provide transparent and comprehensive bond data, including credit rating, yield, duration, etc. This allows investors to choose bond investments that match their investment horizon and capital growth expectations.

Conclusion

Understanding the difference between Modified Duration and Macaulay Duration is essential for evaluating interest rate risk and making informed bond investment decisions. While Macaulay Duration helps investors understand the weighted average time required to recover a bond’s cash flows, Modified Duration provides a practical estimate of how much a bond’s price may change when interest rates move. Together, these measures enable investors to better assess portfolio sensitivity, compare fixed-income instruments effectively, and align investments with their risk tolerance and investment horizon.

As India’s corporate bond market continues to expand, applying duration-based analysis can help investors select bonds that balance stability and return potential. Platforms like Grip Invest make it easier for investors to explore curated bond opportunities and build diversified fixed-income portfolios aligned with their long-term financial goals.

FAQs

1. What is the difference between Macaulay duration and modified duration?

Macaulay duration can help understand the tenure required to generate sufficient bond cash flow to recover principal and interest from a bond investment. Subsequently, Modified duration is an extension of Macaulay duration, as it suggests the specific degree of bond price change with 1% change in yield

2. Which duration is better for measuring interest rate risk?

Modified duration is an extension of Macaulay duration, as it suggests the specific percentage change in bond price with 1% change in yield. Therefore, while both can help gauge price-sensitivity, Modified duration provides a more nuanced take.

3. Does higher duration mean higher risk?

Yes, a longer duration often translates into higher bond risk, particularly in terms of interest rate risk. Therefore, investors aim to match the duration with the investment horizon. For instance, long-term investors prioritise capital growth and can sustain short-term volatility that eases over time, and thus, can choose long-term bonds.

References:

1. NITI, accessed from https://niti.gov.in/sites/default/files/2025-12/Deepening_the_Corporate_Bond_Market_in_India.pdf

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001