Modified Duration Explained: How It Measures Interest Rate Risk In Bonds

Bond investors have significant exposure to rising interest rates because an increase in the rates lowers the price and ultimately reduces the return on bonds.

Modified duration is an important metric offering bond investors a method to evaluate the bond price sensitivity to interest rate fluctuations. This metric enables investors to assess the amount of change in value that a bond will experience based on market interest rate.

It is the preferred tool for identifying the safest bonds and then making an informed decision.

Modified Duration Meaning

Modified duration indicates the bond's exposure to interest rate risk, and it is based on Macaulay duration, or the timing of cash flow receipt. The modified duration formula makes an adjustment for the effect of yield.

The greater the value of modified duration, the greater the price movement will be if interest rates increase or decrease. Investors use this metric as part of their pre-purchase evaluation of the bond valuation risk.

Modified duration is an efficient way for bond investors to evaluate their risk of loss for revaluing bonds. In general, bonds with short maturities will have a lower modified duration than bonds with long maturities.

Modified Duration Formula

The modified duration formula can be stated as Macaulay Duration divided by (1 + yield per period). Macaulay duration gives a weighted average of when you will receive payments from the bond. The yield per period is the total yield divided by the number of payments you receive each year.

This modification makes it easy to estimate how much the bond price will fall as a result of a change in interest rates.

For instance, if you had a 5-year bond with a 5% yield, then the Macaulay Duration would be 4.5 years, and the Modified Duration would be approximately 4.3 years. Similarly, if the interest rate were to increase by 1%, then the bond would decrease in value by 4.3%.

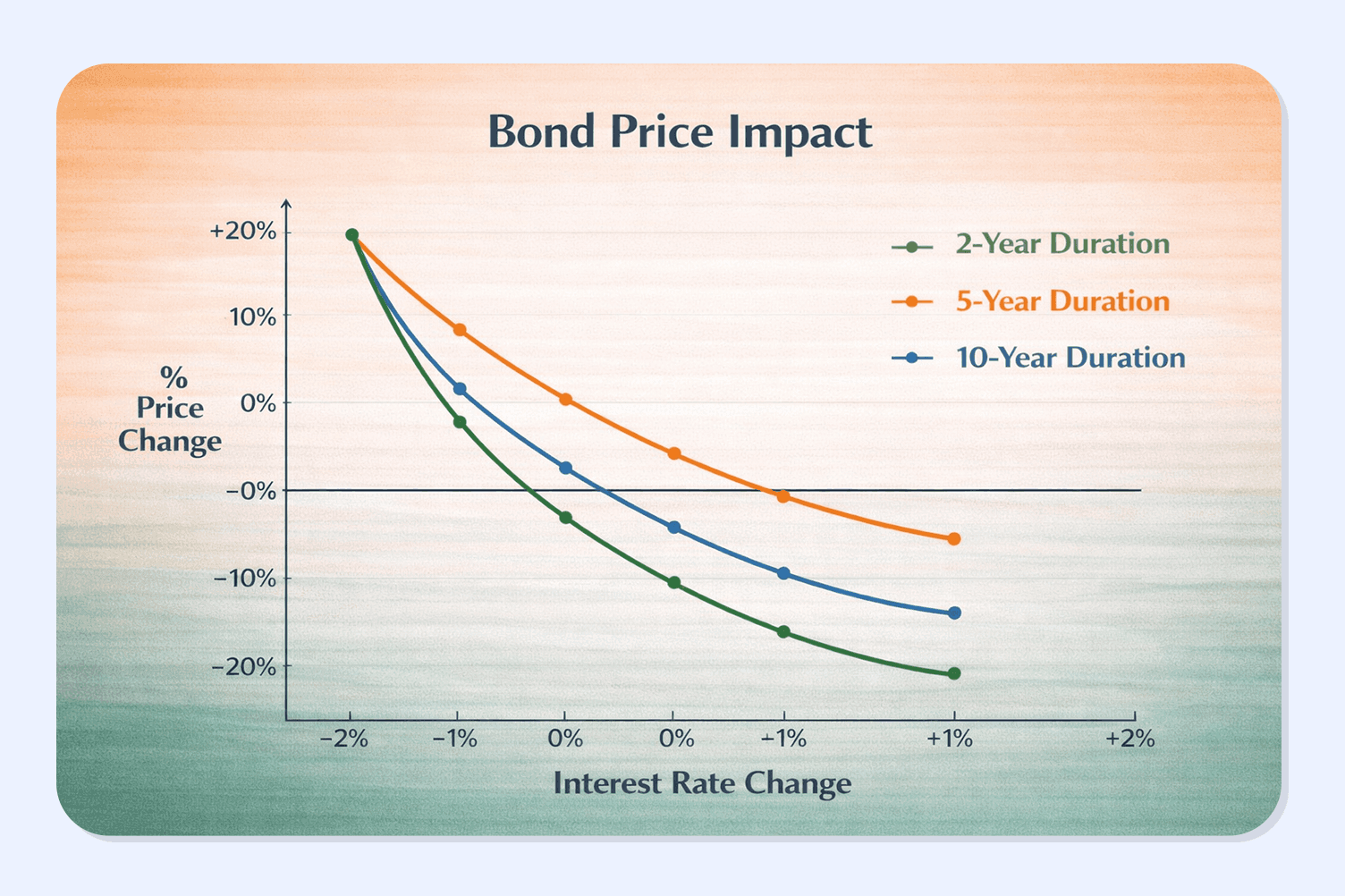

Bond Price Impact

Knowing that the bond price and the bond price sensitivity, modified duration are inversely proportional to interest rate fluctuations. It will assist in making decisions when constructing your portfolio. By matching your views on interest rates to the Bond Price Sensitivity, you will be creating the possibility of achieving your investment goals.

1. Rate Rise Effect

If you owned a bond with a Modified Duration of 5, your bond would decline in value by 5% as a result of a 1% increase in the interest rate.

2. Rate Drop Benefit

If you owned the same bond as before, after an interest rate decrease of 1%, your bond would increase in value by 5%.

3. Convexity Role

Duration assumes straight-line change, but convexity adds a curve. It refines estimates for big shifts. Example: Actual drop is less than predicted for sharp rises.

Modified Duration: Hypothetical Example

A 10-year bond pays 6% annually and has a yield of 6%. Its Macaulay duration measures approximately 7.5 years. We can calculate its modified duration by dividing the Macaulay duration by (1 + 0.06). This gives us a modified duration of about 7.1 years.

Recently, as market interest rates rose to 7%, the value of this bond has decreased by approximately 7.1%. Conversely, should market rates decline to 5%, the bond's price would rise by 7.1%. The difference in prices at different interest rates signifies the effect of duration on the value of a bond.

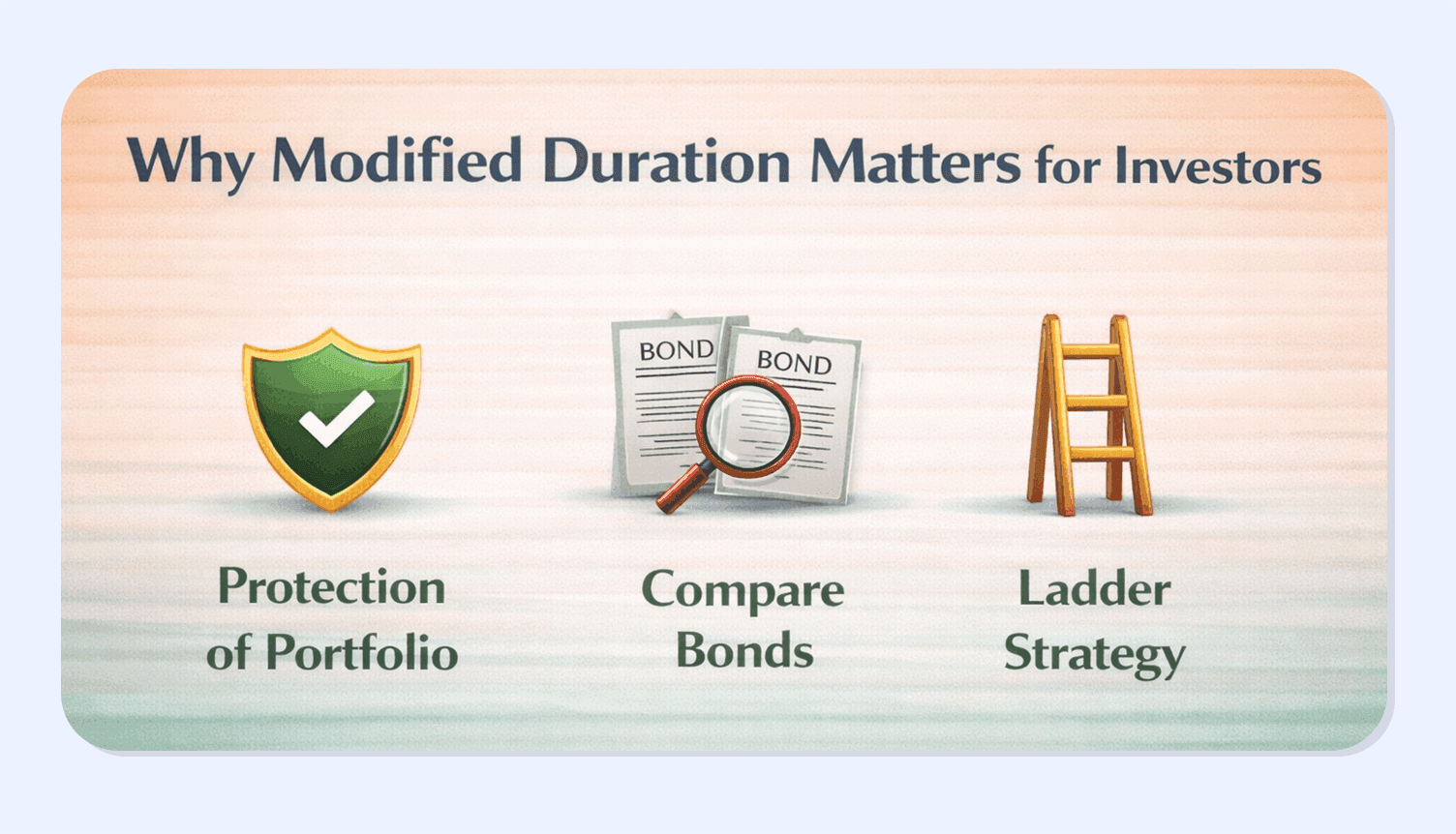

Why Modified Duration Matters for Investors

Investors can use modified duration to assess and manage their bond investments based on interest rate risk. Modified duration provides investors with a quick way to identify which bonds in their portfolios are subject to interest rate changes, allowing for quick adjustments in allocation.

1. Protection of Portfolio

Select bonds that match your outlook on future interest rates. If you believe that market interest rates are going to rise (i.e., 10-year bonds), then you may want to reduce your exposure by investing in short maturities.

2. Comparison between Bonds

Use modified duration as a comparison tool to compare bonds side-by-side to help improve overall portfolio performance and avoid bonds with large interest rate exposure.

3. Ladder Strategy

Create a bond ladder to assist with your investment planning; invest in bonds of varying maturities to achieve a steady cash flow over a period of time.

Beyond Basics

Near the end of their respective maturities, the modified duration of zero-coupon bonds is different from that of coupon bonds, which have a lower modified duration than zero-coupon bonds. Callable bonds require an effective duration rather than a modified duration, as they have less interest rate risk than the other two types of bonds. As the interest rates of Floating rate Notes reset, they have no modified duration. After tax duration will also be impacted by tax law or rules. Always verify yield expectations; to find out how to do this, read our article “Floating Rate Bonds vs Fixed.”

Conclusion

Modified duration is one of the most practical tools bond investors can use to understand interest rate risk before it impacts returns. By knowing how sensitive a bond’s price is to rate movements, investors can make smarter choices around maturity, yield, and portfolio balance—especially in changing rate cycles. Platforms like Grip Invest simplify this process by offering access to curated fixed-income opportunities and clear risk insights, helping investors align duration exposure with their financial goals and risk appetite.

FAQs

1. What is the effect of modified duration on price?

A change in the price of a bond can be estimated through the use of modified durations (shown as percentages) when interest rates change (+ or -). Therefore, as interest rates rise (+/), a greater percentage change will occur to the bond than an equalisation to the lower coupon bond will have, resulting from an equalisation to the higher coupon bond.

2. What is the benefit of a high modified duration?

The increased duration (of bones and floats together) means there will be a greater amount of fluctuation in the price of the bonds during times of declining interest rates, and as a result, greater profit opportunities exist (although there is no loss for bonds upon convergence).

3. Do Fixed and Floating Rate bonds, respectively, apply?

The relationships between fixed rate and floating rates are as follows: both fixed rate and floating rate have either positive or negative modified durations; therefore, floating rate bonds do not have any modified duration due to the fact that floating rate bonds re-evaluate rate intervals.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001