NPS Interest Rate: Returns, Calculation And Investment Strategy

According to research, only 30% of Indians have a structured retirement plan, while the other 70% depends on savings or family support. It is important to have a retirement plan for a better and more relaxed retirement life.

This is why relying solely on traditional saving methods is not enough in modern times. Many smart investors are choosing market-linked options like NPS to build a strong retirement corpus.

If you want to know more about NPS Interest rates and investment strategy, here are all the details you need to know before choosing NPS as a retirement scheme.

What Is NPS?

NPS is a voluntary retirement scheme by the Indian government that is useful for building a strong retirement corpus. This scheme works for salaried and self-employed individual Indian citizens as well as NRIs.

Structure Of NPS

There are two types of NPS accounts.

- Tier 1 Account - This is a primary retirement account with withdrawal restrictions. It is suitable for long-term investors.

- Tier 2 Account - It is an optional account which offers flexible withdrawals to the investors. This is best suited for investors seeking liquidity and flexibility.

Also Read: How To Open An NPS Account: Step-by-Step Guide For Beginners

Asset Allocation In NPS

There are two types of fund allocation patterns that you can choose in NPS.

1. Active Choice

This option allows you to voluntarily distribute your contribution among various assets. It is suitable for investors who want to take risks and control while investing. The different types of assets to allocate your investments to are

- Equity - It is a high-risk asset that offers higher returns as well. NPS subscribers can invest up to 75% in this asset.

- Corporate Bonds - These funds are invested in fixed-income debt instruments.

- Government Schemes - The funds are invested in government securities.

- Alternate Assets - The funds are invested in real estate and infrastructure funds. Only 5% can be allocated to this investment, as it has a higher risk.

2. Auto Choice

Under the Auto choice investment option, the asset allocation is automatically done based on the subscriber's age. Higher equity exposure when subscribers are younger. It gradually shifts to safer assets like bonds and government securities as their age increases. There are three lifecycle options: LC75 (Aggressive), LC50 (Moderate) and LC25 (Conservative). This means the NPS system controls the portfolio for its subscribers.

NPS Interest Rate Explained

NPS does not offer fixed-income rates, unlike other fixed-income schemes. Instead, returns depend on market performance and asset allocations.

1. Market-Linked Returns

NPS invests in equities, bonds and government securities. The return depends on market conditions and how the invested funds perform in the market. So there is no guaranteed return, as confirmed by NPS trust. In 2025, the interest rates range from 9% to 12%, which is higher than the traditional savings schemes.

2. Historical Returns

NPS had a strong track record over the years, especially in long-term investment. The average annual return in NPS is around 9% to 12%. Here is the asset class breakdown with their recorded returns.

- Equity - Equity schemes under NPS have delivered around 10% to 13% results. It remains the highest return scheme in NPS.

- Corporate Bonds - Bonds have a stable return as compared to equity. It offers 8% to 10% with a balance between risk and returns.

- Government Securities - This is known for safety and delivers the lowest returns in NPS, which is around 7% to 9%.

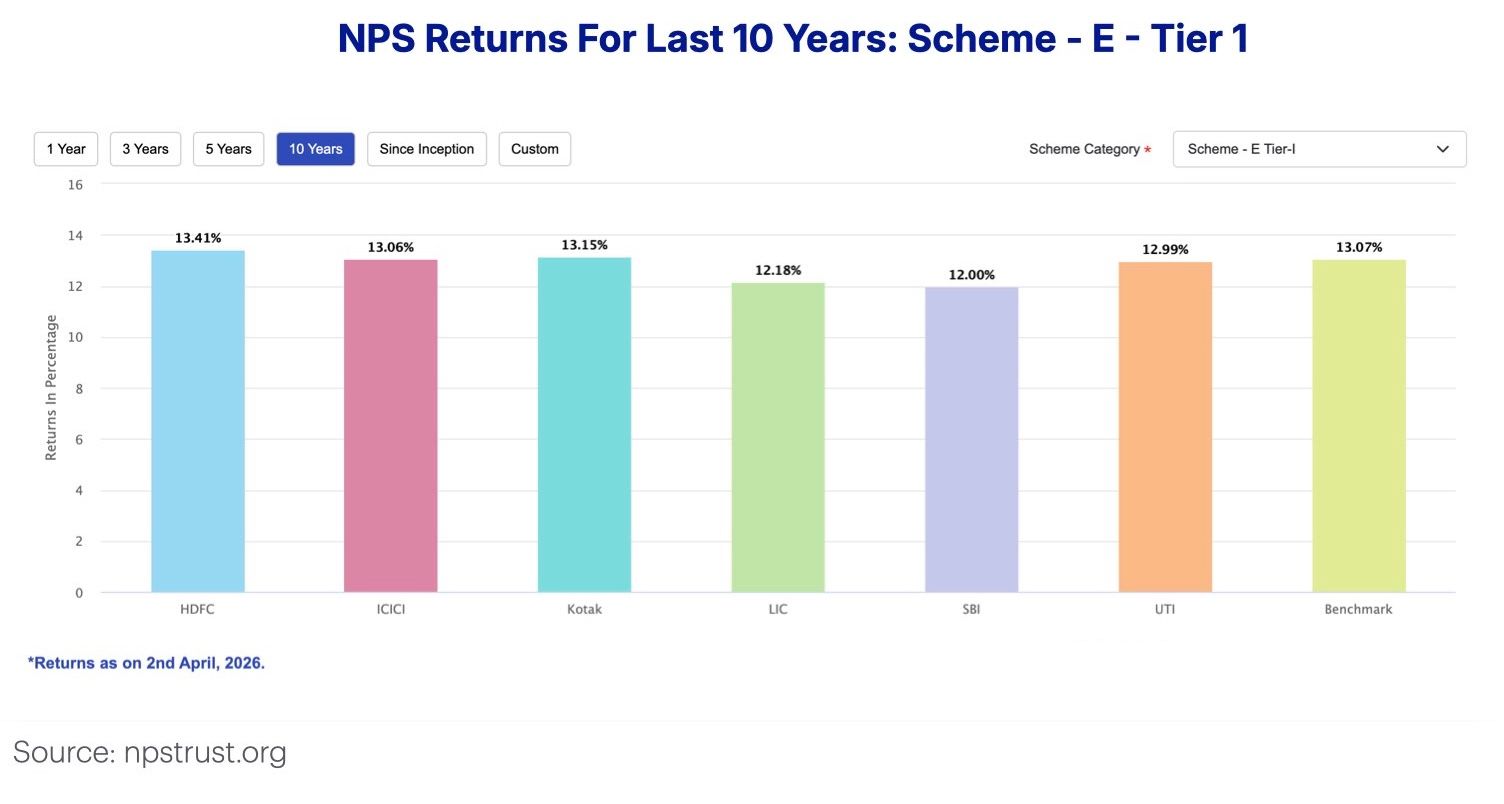

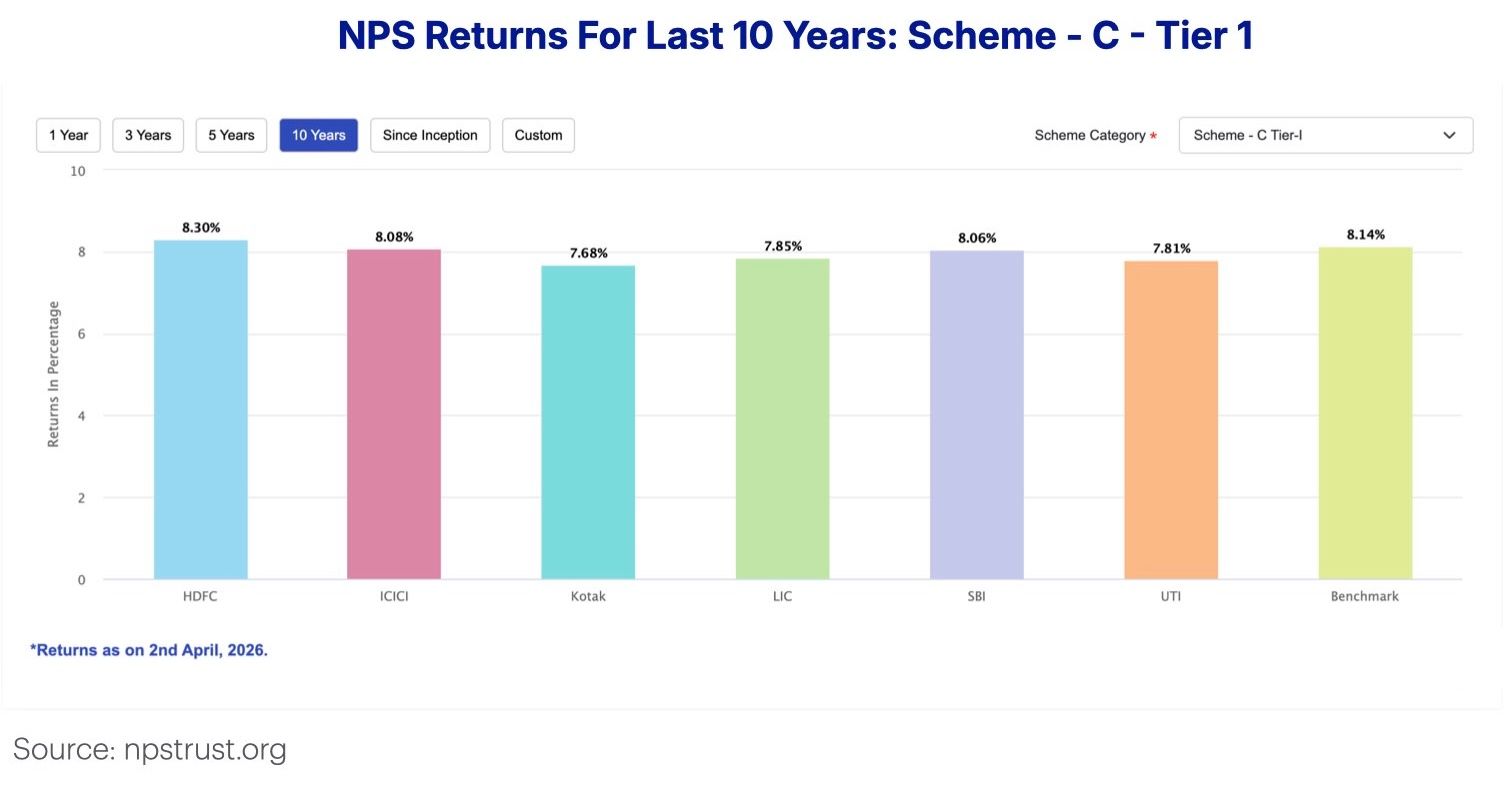

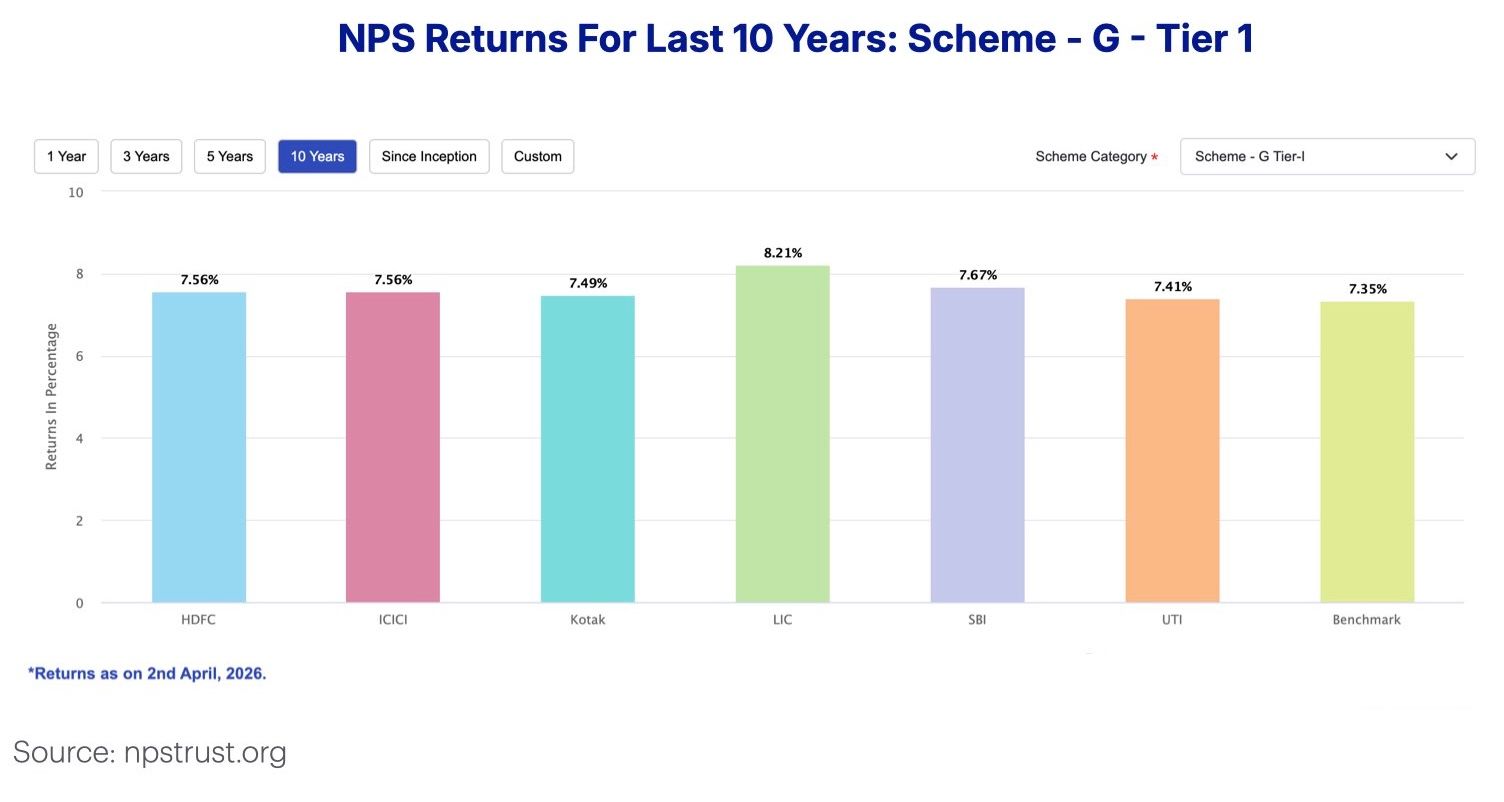

Following are the charts represting the NPS returns over the last 10 years for Tier 1 account for different schemes:

Factors Affecting Returns

Multiple factors can affect the returns in NPS. Understanding these factors can affect your investment strategy.

1. Equity Exposure

Higher equity allocation in NPS increases return potential. Young investors can invest up to 75% corpus in equity as per PFRDA norms. Equity has historically delivered the highest return in NPS.

2. Funds Manager Performance

NPS allows you to choose multiple fund managers with their own investment strategy, research approach and risk management style. Fund managers select stocks and bonds based on their market research. They also adjust portfolios based on market conditions to maximise return.

Is NPS A Good Investment?

Before choosing NPS as a retirement option, check these pros and cons of NPS.

Pros

- NPS provides tax benefits to its subscribers under sections 80C and 80CCD.

- It provides market-linked returns by investing in equity, bonds and government securities.

- You can withdraw 60% corpus upon retirement, and the remaining 40% used to buy an annuity, which will provide a regular pension income.

- NPS provides transparency to its customers by giving regular statements, which help track pension savings.

Cons

- NPS's biggest drawback is that it offers limited withdrawal and you can only upto 25% of total savings.

- The nature of investment in NPS is market-linked and has some market risks.

- Unlike traditional schemes like PPF or FDs, NPS does not offer fixed guaranteed returns.

Where Does NPS Fit In Your Investment Portfolio?

NPS offers tax benefits, cost efficiency and competitive market returns. It is a suitable choice for long-term investors and to grow a strong retirement corpus. However, it should be a core investment component in your portfolio, but not as your only investment. This is why diversifying for investment in FDs, bonds, and mutual funds is a smart investment decision.

Conclusion

NPS is not a fixed return scheme, but it is for long-term wealth creation with patience and discipline. The historical return of 10 to 12% has proven that it is a smart choice for a strong retirement corpus. However, the key to maximising NPS is asset allocation and diversification.

If you are looking for diversified investment options beyond NPS, visit Grip Invest, which is a SEBI - regulated platform offering fixed income opportunities like corporate bonds, SDIs, and FDs all at one place.

FAQs On NPS Interest Rate

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001