NPS vs Mutual Fund: Which Is Better For Your Long-Term Goals In 2026?

Introduction

Selecting an appropriate investment option for achieving long-term financial goals, like retirement, is one of the most essential elements for a secure future in the year 2026. Understanding NPS vs mutual funds helps you align choices with future goals. The National Pension System (NPS) and mutual funds are the two main popular options in India, each with distinct features, returns, and tax implications

This article compares NPS and mutual funds in order to assist you in making an informed decision, and also incorporates the major differences, historical returns, and a strategic approach with the motive to optimise your investments.

NPS vs Mutual Fund: Key Differences

The National Pension System (NPS) is a government-backed retirement savings scheme introduced by the Pension Fund Regulatory and Development Authority (PFRDA). It is designed to help Indian citizens build a post-retirement corpus through systematic investments in equity, government securities, and corporate debt. NPS is ideal for long-term investors seeking stable retirement income, as it includes a mandatory annuity purchase upon maturity.

Mutual funds, on the other hand, are market-linked investment instruments that offer greater flexibility and can be tailored to various financial goals such as retirement planning, wealth creation, children's education, or buying a house. These funds invest in equity, debt, hybrid, or index-based portfolios, depending on the scheme type, and are managed by professional fund managers.

Key Differences: NPS vs Mutual Funds In 2026

1. Investment Goal:

NPS focuses exclusively on retirement planning in India, with an emphasis on disciplined, long-term saving. Mutual funds cater to a variety of goals including short-term growth, long-term wealth creation, and tax saving through ELSS.

2. Lock-in Period:

NPS has a lock-in until the age of 60, although partial withdrawals are allowed under certain conditions. In contrast, mutual funds, except for ELSS (Equity-Linked Saving Schemes) which have a 3-year lock-in, offer high liquidity, allowing investors to redeem units as needed.

3. Tax Structure:

NPS offers tax deductions of up to INR 2 lakh per year (INR 1.5 lakh under Section 80C and INR 50,000 under Section 80CCD(1B)), making it one of the best tax-saving options for salaried individuals.

Mutual funds offer tax benefits only under ELSS schemes, with a deduction of up to INR 1.5 lakh under Section 80C. Other mutual funds (like debt or hybrid funds) do not provide upfront tax deductions but may offer capital gains tax efficiency if held long-term.

NPS vs Mutual Funds: Quick Comparison Table

The table below summarizes the key features highlighting NPS vs mutual funds for 2026 investors.

Feature | NPS | Mutual Funds |

Purpose | Retirement corpus | Flexible wealth creation |

Lock-in-Period | Until age 60 (partial withdrawal allowed) | None for open-ended funds; 3 years for ELSS |

Returns | 8-10% (equity), 6-8% (debt) | 10-15% (equity funds, historical) |

Tax Benefits | Up to INR 2 lakh (80C + 80CCD(1B)) | Up to INR 1.5 lakh for ELSS (80C) |

Liquidity | Low (restricted withdrawals) | High (except ELSS) |

Risk | Moderate (depends on allocation) | Varies (low to high) |

Tax Implications: NPS vs Mutual Fund

Below is a reference table summarizing major tax implications for NPS and SIP/Mutual Funds in 2026.

Particulars | Equity Mutual Funds (SIP/ELSS) | NPS (Tier I) |

Tax Deduction | INR 1.5 lakh under Section 80C | INR 1.5 lakh under 80C + INR 50,000 under 80CCD(1B) |

Taxation on Returns | LTCG: 10% over INR 1 lakh; STCG: 15% | 60% corpus tax-free; 40% to annuity (taxable as income) |

Lock-in Period | 3 years (ELSS); none for other funds | Till age 60 (partial withdrawal allowed) |

Premature Withdrawal | Allowed (conditions for ELSS) | 25% of own contribution under conditions |

NPS vs Mutual Fund Returns: Long-Term Performance Analysis

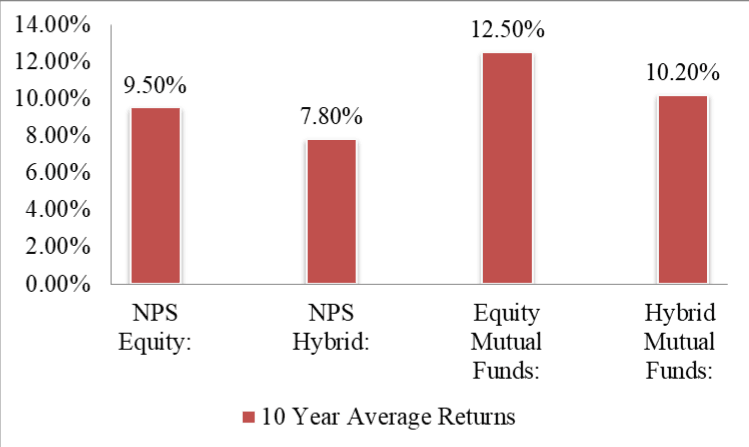

Returns are a key consideration when choosing between NPS and mutual funds. In 2025, NPS Tier 1 equity funds have delivered 13–17% annual returns for the best schemes, while long-term averages remain 8–12%. NPS Tier 1 offers a mix of equity, corporate bonds, and government securities, with historical returns of 8-10% for equity and 6-8% for debt over 10 years1. However, 40% of the NPS corpus must be invested in an annuity at maturity, yielding 5-6%, which caps overall returns.

Equity mutual funds, particularly large-cap and multi-cap funds, have historically delivered 10-15% annualized returns over 10 years, though they are subject to market volatility2. Hybrid mutual funds, balancing equity and debt, offer 8-12% returns with moderate risk.

Bar Chart: 10-Year Average Returns (Hypothetical)

Below is a hypothetical comparison of 10-year average annualized returns based on historical trends (as of 2025 estimates):

Risk And Flexibility

NPS offers controlled risk through diversified asset allocation (up to 75% in equity for Tier 1). Investors can choose active or auto allocation, but the mandatory annuity reduces flexibility. Mutual funds provide greater flexibility, allowing investors to select funds based on risk appetite (e.g., small-cap for high risk, debt funds for low risk). Evaluating NPS vs mutual funds which is better for your risk tolerance is important. It helps you allocate more effectively between stable and volatile assets.

Systematic Investment Plans (SIPs) in mutual funds enable disciplined investing without a long lock-in, unlike NPS.

Example: Priya is a 35-year-old professional and her portfolio is a practical example to understand the difference between NPS and mutual fund investments. She allocates 50% of her portfolio to NPS for tax benefits and retirement security, and 50% to equity mutual fund SIPs for higher returns and liquidity to fund her child’s education in 10 years.

Which One Should You Choose and When?

Your choice between NPS and mutual funds depends on your financial goals, risk tolerance, and liquidity needs. Here’s a strategic approach:

- Young Investors (20s-30s): Combine NPS for tax benefits and retirement planning with equity mutual fund SIPs for higher returns. Example: Raj, 30, invests INR 50,000 annually in NPS for tax savings and INR 10,000 monthly in an equity mutual fund SIP for wealth creation.

- Mid-Career (40s): Increase NPS contributions for a secure retirement corpus while maintaining a balanced mutual fund portfolio for goals like children’s education.

- Pre-Retirement (50s): Shift mutual fund investments to hybrid or debt funds for stability, while maximizing NPS contributions for tax benefits.

- Strategy: Invest in both NPS and mutual funds to optimize tax savings, liquidity, and returns. Allocate 60% to mutual funds for flexibility and 40% to NPS for retirement security.

Conclusion

The National Pension System (NPS) and mutual funds serve distinct investment purposes for Indian investors. NPS is best suited for long-term retirement planning, offering stable returns, low management costs, and significant tax benefits under Sections 80C and 80CCD(1B).

On the other hand, mutual funds, especially equity mutual funds, provide greater flexibility, higher return potential, and liquidity, making them ideal for a range of financial goals like wealth creation, education, or short-term investing.

When comparing NPS vs SIP or mutual funds, each investment option offers unique advantages. By understanding NPS vs mutual funds returns individually, such as lock-in periods, taxation, risk levels, and return expectations, you can strategically combine both in your investment portfolio. This hybrid approach helps you balance security with growth, aligning your investments with your financial goals in 2026 and beyond.

If you are looking to further diversify your long-term portfolio, consider exploring high-yield corporate bonds and alternative investment options on Grip Invest.

FAQs On NPS vs Mutual Funds

1. Can I invest in both NPS and mutual funds?

Yes, investing in both diversifies your portfolio, optimizes tax benefits, and balances liquidity and retirement planning.

2. What is the lock-in period for NPS and ELSS?

NPS has a lock-in until age 60, with partial withdrawals allowed under specific conditions. ELSS mutual funds have a 3-year lock-in.

3. How is NPS taxed at maturity?

At maturity, 60% of the NPS corpus is tax-free, while 40% must be invested in an annuity, with annuity income taxable as per your slab rate.

For more on retirement planning, explore our blog on Retirement Planning in India for 2025.

4. Is NPS better than a mutual fund for retirement?

NPS is ideal for those who are seeking a disciplined retirement savings option that benefits tax and stable returns. Mutual funds yield more growth but less risk and flexibility. NPS is better for longer-term retirement savings, and mutual funds are better for shorter-term goals.

5. Can I invest in both NPS and Mutual Fund?

Yes, you can diversify your portfolio by investing in both. NPS offers retirement tax benefits, and mutual funds provide liquidity and growth. To effectively fund a comprehensive financial strategy, a mix also balances stability, tax savings, and wealth creation.

6. What are NPS tax benefits compared to mutual funds?

NPS has up to 2 lakh in deductions (1.5 lakh under 80C plus 50,000 under 80CCD(1)B) and 1B. This allows ELSS mutual funds only 1.5 lakh deduction under 80C, and NPS is tax-efficient for salaried investors.

7. Is NPS risk-free?

It is not risk-free, but risk is controlled through diversified asset allocation with small equity exposure. It is a low risk asset that is stable government securities and bonds and suitable for short-run investors .

8. Which gives higher returns - NPS or mutual fund?

Mutual funds, particularly equity funds, generally return higher (10–15%) returns but they are more volatile. As a growth prospect, mutual funds are better for investment than NPS returns and are high in return for an annuity purchase , making them easier to get with mutual funds .

References

1. NPS Trust, accessed from: https://www.npstrust.org.in

2. Association Of Mutual Funds In India, accessed from: https://www.amfiindia.com

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks and shenanigans that take place in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001