Satyam Computers Share Price History: Lessons From India’s Biggest Corporate Fraud

2009 was a challenging year for both Indian and global companies. The world was still recovering from the aftermath of the Subprime Crisis, which had pushed major economies into financial recession.

During that time, the Satyam Scandal, often dubbed as India’s own ‘Enron Case’, was reported and shook investors, regulators, and the general public alike.

Founded in 1987, Satyam Computers Services Limited was among the largest IT services companies in the country. Along with TCS, Infosys, and Wipro, the company was regarded as a critical part of the country’s flourishing IT Sector. The company served clients mainly in the US, including 185 Fortune 500 companies.

However, the company’s strong reputation came crashing down when the founder, B. Ramalinga Raju, confessed to being part of a massive accounting fraud that had been ongoing for many years, resulting in the company inflating its assets by over $1 billion.

Source: Screener1

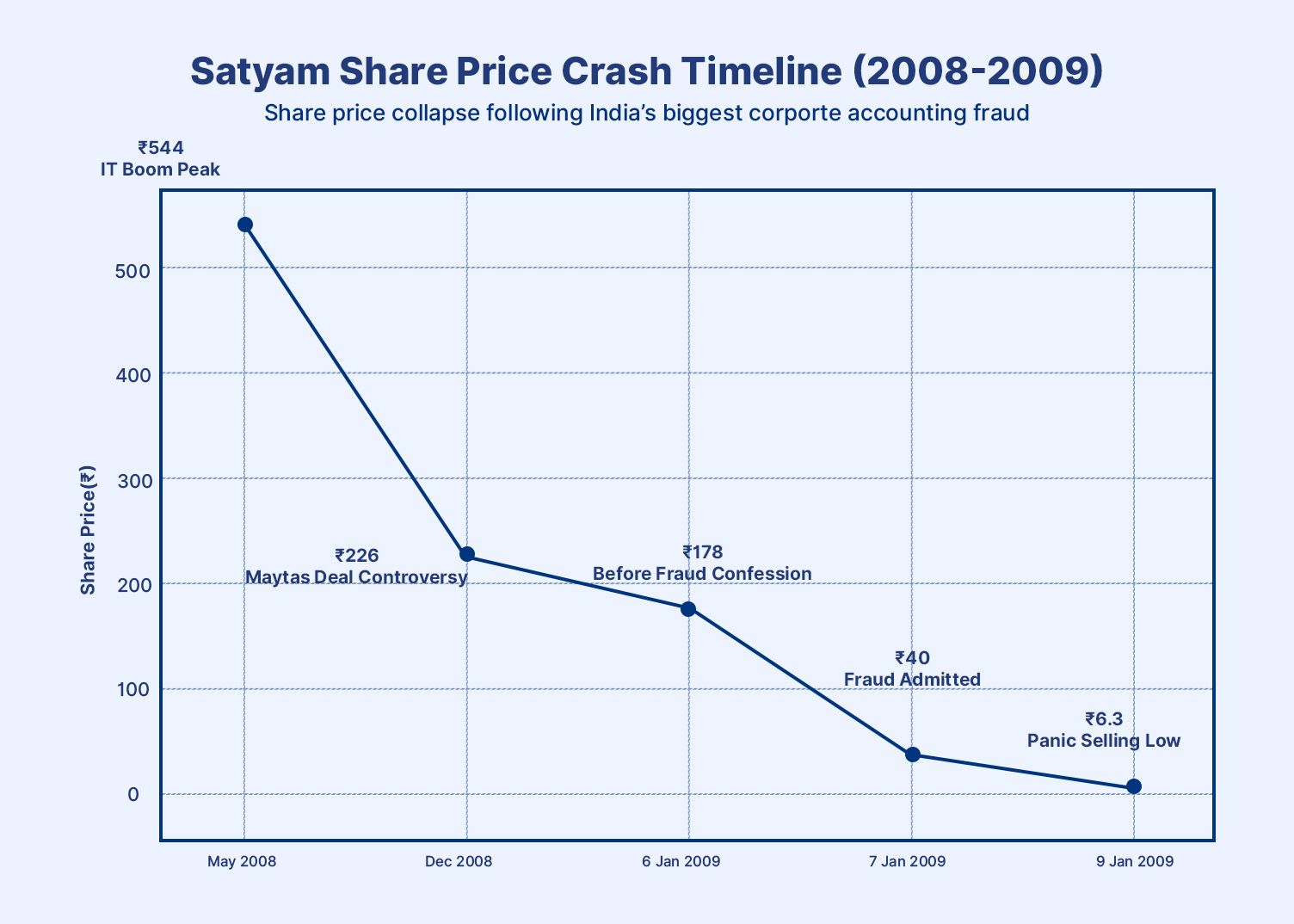

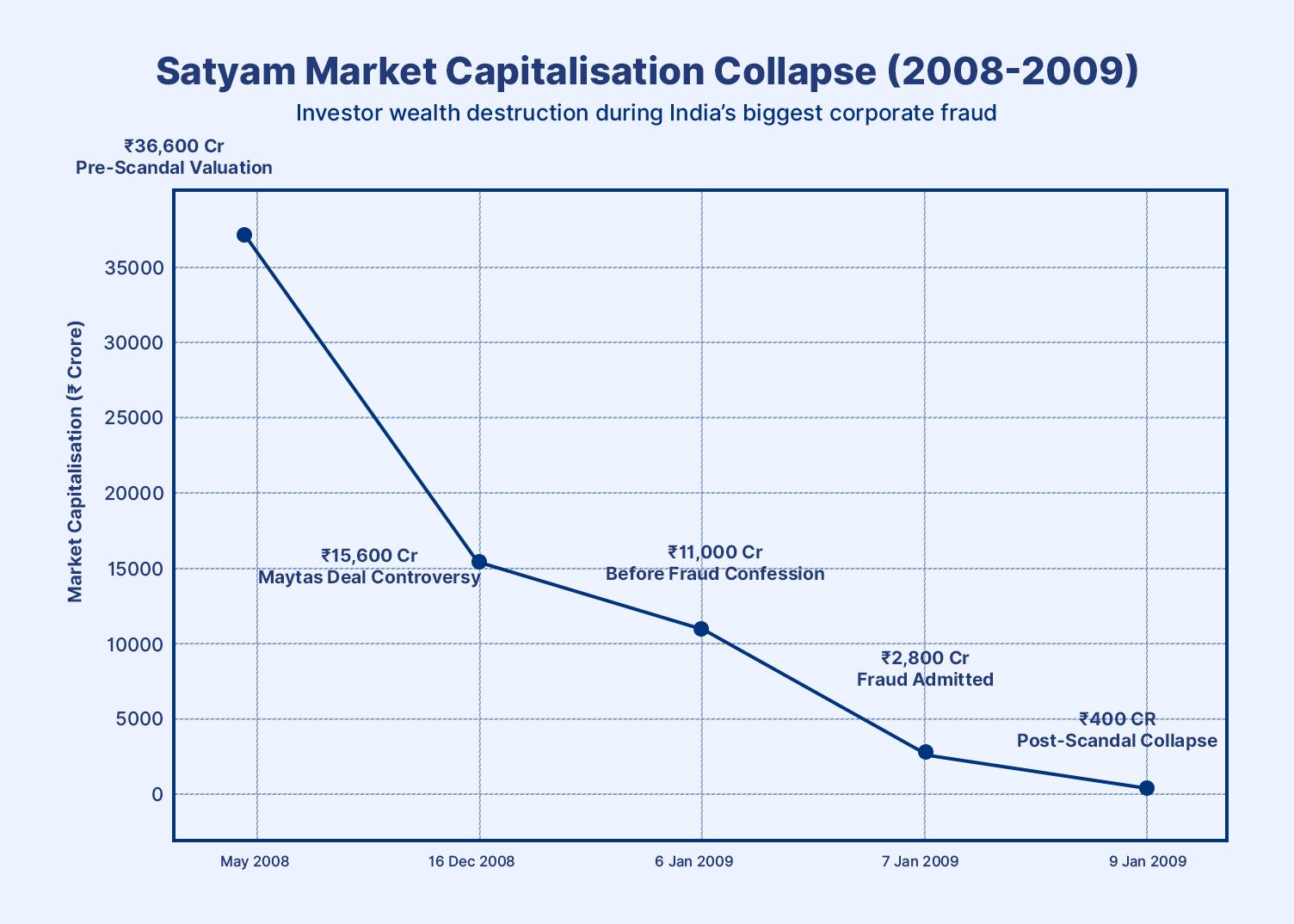

As shown in the graph depicting Satyam Computers share price, the stock lost almost 99% of its market capitalization from its May 2008 peak. The Satyam share price before scam was INR 540, which dwindled down to INR 6 after the scam was revealed.

For investors, the Satyam scandal serves as a powerful reminder that even well-known companies can hide significant risks. Examining Satyam’s share price history and the events surrounding its collapse offers valuable lessons about transparency, risk management, and diversification.

What Was Satyam Computers?

Talking about the Satyam company history, the enterprise was one of the largest IT services companies in India, serving a range of customers (including Fortune 500 companies) across the world, and particularly in the US. During the 1990s and early 2000s, the global demand for outsourcing and software services helped Indian IT firms grow rapidly, and Satyam was among the biggest beneficiaries of this trend.

By the mid-2000s, the company had a strong global presence with operations in different countries. Its clientele included governments and large corporations. Satyam was listed on major stock exchanges and was considered a respected member of India’s technology sector alongside companies such as Infosys, TCS, and Wipro.

The company reported strong revenue growth, impressive profit margins, and large cash reserves. These factors helped boost investor confidence and drove strong demand for Satyam’s shares. However, it was later reported that the growth figures were inflated and that the company overstated its assets and revenue.

The Corporate Fraud That Shook Markets

Satyam Scandal Explained: Satyam’s stock was considered one of the favourites for long-term investments due to the company's fundamental strength and sustained growth. It was a preferred choice for a large number of mutual funds, institutional and individual investors. However, during the Hyderabad real estate crash, a critical trail linking the company was identified by numerous whistleblowers.

The Satyam scandal SEBI investigation found that the management was responsible for falsifying accounts, inflating revenues and assets, and manipulating share price for the benefit of the founder and other board members. It is a classic example of the problems identified in India's family-owned corporate environment.

The scale of the fraud was staggering. According to investigations, Satyam had inflated its financial position by more than INR 7,000 crore. The company’s balance sheet had shown large cash reserves that simply did not exist, while profits had been exaggerated to maintain the illusion of consistent growth.

For investors and regulators, it was a critical shock, as the company had maintained a strong track record of corporate governance. Interestingly, the company received the coveted Golden Peacock Global Award for excellence in Corporate Governance in 2008, just a year before the revelations. The Institute of Internal Auditors, USA, also awarded the company a Recognition of Commitment.

The scandal also triggered widespread concerns about transparency within corporate India. Regulators, institutional investors, and market participants began reassessing governance standards across listed companies.

Share Price Collapse And Market Reaction

As illustrated in Figure 1.0, Raju's confession led to an unprecedented Satyam

Computers stock crash in 2009, which further eroded 99% of the company’s market capitalisation. Investors rushed to sell their holdings as confidence in the company evaporated almost overnight. The stock lost a significant portion of its value within days, destroying billions of rupees in market capitalisation.

Before the scandal, Satyam had been valued as one of India’s major IT companies. After the confession, however, the company’s market value plunged, leaving retail and institutional investors with heavy losses. There was also a massive issue affecting the future of thousands of employees, and concerns about open orders and ongoing projects involving some of the biggest corporations and governments in the world. Further, the failure of one of the largest IT companies in the country raised serious questions about the strength and sustainability of the sector in a then-struggling economy.

Source: Screener

A new board was appointed to stabilise the company and oversee a transparent resolution process. Eventually, Tech Mahindra acquired Satyam in a government-supervised bidding process in 2009. The company was later rebranded as Mahindra Satyam and eventually merged with Tech Mahindra.

How Satyam Computers Compares With India’s Top IT Stocks

| Name | EPS 12M | P/E | DIV YIELD % | 1YR RETURN % | MAR CAP RS CR |

| TCS | 136.01 | 15.77 | 2.76 | -34.75 | 828505.86 |

| Infosys | 72.59 | 15.9 | 4.07 | -26.07 | 477067.14 |

| HCL Technologies | 61.33 | 18.29 | 4.62 | -30.35 | 317023.94 |

| Wipro | 12.58 | 16.44 | 5.33 | -17.34 | 217550.60 |

| Tech Mahindra | 49.1 | 28.32 | 3.54 | -10.36 | 141652.36 |

| LTM | 169.25 | 21.95 | 1.88 | -21.91 | 118767.16 |

| Persistent Systems | 118.23 | 41.51 | 0.69 | -11.47 | 80320.69 |

Source: Screener

From the above per analysis we observe Tech Mahindra had the best 1-year return performance with a relatively smaller decline of -10.36%, showing stronger resilience during the sector slowdown. Despite this, it trades at a higher P/E ratio of 28.32, suggesting investors expect better future growth compared to larger peers like TCS and Infosys.

The company also offers a healthy dividend yield of 3.54%, balancing both growth expectations and shareholder returns.

Advantages And Risks Of Buying Satyam Computers Shares

Pros

- Mahindra group backing: Tech Mahindra is backed by the Mahindra group, which is a massive global conglomerate owning 150 brands headquartered in Mumbai which gives it brand and governance credibility.

- High dividend payouts: Tech Mahindra distributes dividends usually twice a year (interim dividend and final dividend). FY2026 dividend is the highest distributed by Tech Mahindra yet, Rs 51 per share. These dividends often attract investors who are income oriented and want predictable returns.

Cons

- Tech Mahindra’s profit margins have increased by 13% from FY2025 to FY2026, however it has not been observed with an appropriate growth in revenue. This indicates that increase in profit has not come from an increase in demand but rather from cost cutting and enhancing operational efficiencies. If this trend is observed in the long run it will have a negative impact on the company’s valuation and stock recommendations.

- AI disruptions and automation threaten traditional IT services which make up a large portion of Tech Mahindra’s revenues. However these pressures can be minimised through rapid adoption of AI and investment in automation.

- Tech Mahindra has significant exposure to US and global markets, a recession in the US could lead to companies cutting down on discretionary IT spending, directly impacting Tech Mahindra negatively.

Investor Lessons From The Satyam Scam

There are numerous lessons that investors can learn from the scam. Here are some of the most critical ones:

1. Importance of Corporate Governance

Corporate Governance is more than just regulatory compliance. It is as critical as a company's financial performance indicators. Transparent reporting, independent boards, and credible auditing practices are essential indicators of a company’s long-term reliability.

2. Risks of blind trust in management

Raju was a veteran in the IT sector, but no individual can be completely relied upon, especially when long-term investments are considered. The leadership was rewarded with accolades, and, prima facie, there was no reason to doubt the company’s success. However, it is important to constantly look for red flags and acknowledge what whistleblowers underline.

3. Diversification is Critical

Investing in a single asset class or sector can result in high returns, but there is a downside to this approach as well. If you have long-term goals in mind, it is important to diversify your portfolio across asset classes, sectors, and instruments to reduce the impact of such events.

Platforms like Grip Invest provide access to curated corporate bond opportunities that offer fixed returns of up to 12.5%, helping investors diversify beyond equities while maintaining potential income stability.

Conclusion

The rise and fall of Satyam remains one of the most defining moments in the company's regulatory and corporate governance history. While the scandal exposed serious failures in governance and oversight, it also reinforced the importance of transparency and investor vigilance.

The biggest investor takeaway is to never underestimate the importance of diversification in ensuring long-term portfolio goals are attained.

FAQs

1. What happened to Satyam Computers shares?

After the fraud was revealed on 7 January 2009, Satyam’s share price collapsed from about INR 544 in 2008 to nearly INR 6.30 within days, wiping out most investor wealth. In 2009, Tech Mahindra acquired the company, and Satyam was later renamed Mahindra Satyam.

2. Who exposed the Satyam scam?

The scam was exposed when founder and chairman B. Ramalinga Raju confessed to the fraud in a letter to the board on 7 January 2009, admitting that the company’s accounts had been falsified for years.

3. Is Satyam still listed?

No. Satyam Computers is no longer listed. After being acquired by Tech Mahindra in 2009 and renamed Mahindra Satyam, the company merged with Tech Mahindra in 2013, ending its separate listing.

1. Screener, accessed from: https://www.screener.in/company/SATYAMCOMP/consolidated/

2. Screener, accessed from: https://www.directors-institute.com/post/satyam-scandal

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001