UPS Vs NPS: Building A Perfect Retirement Corpus

Retirement planning is one of the most important decisions that you will make in your financial journey. The two primary retirement planning options in India are the National Pension System (NPS) and the Unified Pensions Scheme (UPS). Due to continuous changes in the structure of these options, there has been a debate about these plans in recent years.

NPS was introduced in 2004, and it is linked to the market. It does not guarantee an assured pension like the Old Pension Scheme. Hence, it received a lot of criticism. To bring assured pension benefits, the government brought the Unified Pension Scheme (UPS) in 20241. Now, UPS comes with an assured retirement corpus, but the returns earned in this scheme are lower than the NPS. Hence, the question arises - which one is better?

In this article, we will explore the key differences between the NPS and UPS and understand the benefits and drawbacks of both schemes. Based on the analysis, you can decide which one is better for you, UPS or NPS.

Understanding The Foundations Of UPS And NPS

What Is The National Pension System (NPS)?

The National Pension System (NPS) is a voluntary, market-linked retirement savings scheme which works on the basis of defined contributions from the employee and the employer, i.e. government. It was introduced in 2004, replacing the Old Pension Scheme for government employees. Later on, it was extended to include the private sector employees, self-employed people and NRIs too. Under NPS, the contributions are invested in various assets, including the equity market, government securities and corporate debt2.

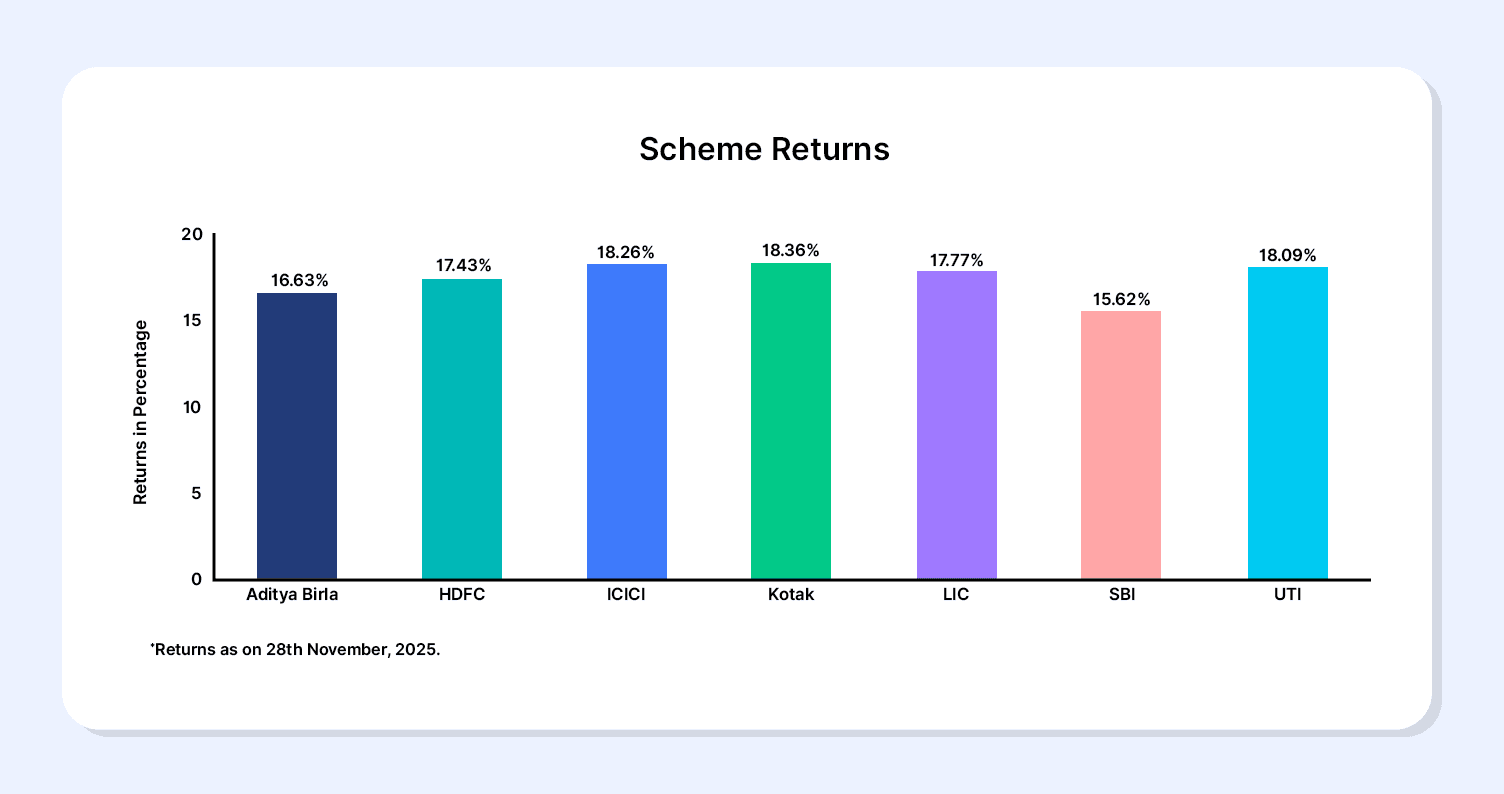

Due to the inclusion of the equity market, the NPS scheme becomes a market-linked scheme and depends on the market performance. Hence, it comes with a risk but offers a high return potential too. A key factor in UPS vs NPS comparison is that the NPS does not offer a guaranteed pension. The graph below represents the last 5 years' returns of the equity scheme of Tier 1 account:

Source: NPS Trust3

What Is The Unified Pension Scheme (UPS)?

The Unified Pension Scheme (UPS) was introduced in 2024 and became effective on April 1, 2025. The basic structure of UPS is hybrid, and therefore, it offers an assured retirement corpus. However, there is a similarity between NPS and UPS - they both work on a contribution model.

The difference comes with the assured benefits for the central government employees who complete at least 25 years of service. For such employees, UPS assures a payout equal to 50% of the average basic salary over the last 12 months prior to superannuation. In the article, we will further explore the key differences between the NPS and UPS and will understand how UPS is able to offer a guaranteed pension.

Key Differences Between NPS And UPS

If you are supposed to select between NPS and UPS, you need to understand the fundamental differences between the schemes. It is essential to know the risk management, returns, and long-term security of UPS vs NPS pension schemes. The choice usually lies between balancing the high returns of NPS and the security of UPS. There are different tools available online, like the NPS vs UPS calculator, that can help you estimate the returns of these schemes.

However, only estimating the returns should not be the criterion of selection. Understanding the difference between core features is the key. The table below is a clear representation of UPS vs NPS pension schemes on the basis of different features that employees expect.

Here is a detailed UPS vs NPS comparison addressing the critical differences:

| Features | National Pension System (NPS) | Unified Pension Scheme (UPS) |

| Type of Scheme | Market-linked returns, defined-contribution pension product | Hybrid Pension Scheme: backed by the government with a guaranteed fixed monthly payout (defined benefit + contribution model) |

| Risk Level | Comes with high risk due to market-linked returns; benefits are not guaranteed | Low risk scheme due to government backing for assured benefits. |

| Applicability | Available for government employees (post 2004), private sector employees, self-employed people and NRIs | Currently available to central government employees. It may get extended to state government employees. |

| Guaranteed Pension | No guarantee of minimum pension | Yes, if the employee serves a minimum of 25 years (50% of the average basic salary over the last 12 months) |

| Minimum Assured Pension | None | INR 10,000 for employees who complete at least 10 years of service |

| Employee Contribution | 10% of basic salary plus Dearness Allowance (DA) | 10% of basic salary plus Dearness Allowance (DA). |

| Government Contribution | 14% of the basic salary and DA | 10% matching contribution plus an additional estimated 8.5% of salary and DA credited to a Pool Corpus. |

| Gratuity | No gratuity payment | Yes, Retirement Gratuity and Death Gratuity are extended to UPS subscribers under the relevant CCS rules |

| Inflation Protection | No provision for automatic Dearness Allowance (DA) increments | Yes, inflation protection is provided by adjusting pensions based on Dearness Relief (DR) |

| Family Benefit | Depends on the annuity plan chosen | Yes, the legally wedded spouse receives 60% of the admissible payout drawn by the subscriber immediately prior to demise |

| Withdrawal Option | You can withdraw 60% of the corpus (tax-free) at retirement; 40% is mandatory to convert to an annuity | Under the guaranteed structure, there is no lump sum option; only a structured monthly pension. However, the subscriber may opt to withdraw up to 60% of the Individual Corpus (IC) or Benchmark Corpus (BC), whichever is lower, but this reduces the assured payout proportionately |

| Investment Flexibility | Comes with the flexibility to choose different fund managers and investment options for the entire corpus | Generally offers no flexibility for the guaranteed payout structure. However, subscribers can choose investment options for the Individual Corpus (IC), such as 100% Government Securities (Scheme G) or Life Cycle Funds (LC-25, LC-50)4 |

Now that you have a clear view of the comparison between UPS and NPS, it should be easy to decide which one is better for you. In many features, NPS says “No”, but then it comes with higher returns and bigger retirement corpus and better flexibility of investment options. Let’s see which can be suitable for you.

How To Choose The Right Option Between UPS Vs NPS

The determination of UPS vs NPS, which is better, depends primarily on the risk profile of the employees and their employment status.

- If you are looking for flexibility in building your retirement corpus and your risk appetite is higher, you can go for NPS. It is available for government employees, private sector employees, self-employed people, as well as NRIs. The market-linked assets can offer high returns but come with high risk too.

- On the other hand, if your risk appetite is low and you are looking for assured pension benefits, then UPS is ideal for you. It comes with a guaranteed pension and inflation protection, and family benefits too. However, the flexibility is limited in UPS and once opted it is considered final.

Therefore, before deciding the best pension scheme for you, think thoroughly and analyse every aspect of the scheme.

Diversify For A Stable Retirement Corpus

Whichever plan you choose from the options, the core of the decision is better returns with stability. In fact, UPS came into existence due to this unpredictable corpus of NPS. But UPS has many limitations, which can result in a lower retirement corpus. In such a scenario, it is essential to add additional assets into your retirement plan so that you are able to balance it with returns as well as stability. And fixed income opportunities like Corporate Bonds can play a vital role here.

Although the NPS structure already recognises the importance of fixed income assets, employee contributions can be invested in government securities and corporate debt too. But for better options and flexibility, you can further add individual corporate bonds with different ratings to your retirement investments. This way, you can increase the contribution of the corporate debt according to your risk appetite and retirement goals.

Adding corporate bonds (or other low-risk options like (Corporate Fixed Deposits) to a portfolio offers assured returns and stability. This strategy helps mitigate the market risks inherent in the equity portion of NPS and complements the guaranteed structure of UPS.

Conclusion

NPS and UPS both offer distinct retirement planning benefits, but they cater to different types of investors. The National Pension System (NPS) is better suited for individuals with a higher risk appetite who are comfortable investing in market-linked assets such as equity and corporate debt. In contrast, the Unified Pension Scheme (UPS) provides assured benefits with a guaranteed pension, making it ideal for those who prioritise stability and predictable post-retirement income. Understanding these differences is essential when comparing UPS vs NPS for long-term financial security.

However, depending solely on either scheme may not be enough to build a truly resilient retirement corpus. Diversifying your portfolio with high-quality Corporate Bonds can offer stable returns, reduce portfolio volatility, and create an additional income stream during retirement. Corporate Bonds also provide better visibility on returns compared to traditional pension schemes, helping you strike a balance between growth and safety.

To explore reliable fixed-income opportunities and build a stronger retirement strategy, visit Grip Invest today.

FAQs On UPS vs NPS

1. Is UPS better than NPS for government employees?

UPS is better if the government employees are looking for assured pension benefits. UPS offers a guaranteed pension (50% of average basic salary if service is 25+ years). It also comes with inflation protection via Dearness Relief. However, the returns received from UPS can be lower than NPS. Hence, if the government employee is willing to take a risk, he can opt for NPS with market-linked assets.

2. Can a Central Government employee switch from NPS to UPS?

Yes, existing Central Government employees under NPS can opt for the UPS. UPS is an optional scheme under the NPS architecture only. Employees willing to switch to UPS can do it by November 30, 2025, or within extended timelines. Once the employee switches to UPS, it is considered final.

3. What is the key difference regarding the pension guarantee?

NPS is market-linked and does not offer an assured pension; returns depend on market performance. UPS is government-backed and guarantees a fixed monthly payout, assuring 50% of the average basic salary for those with 25+ years of service and a minimum of INR 10,000 for 10+ years.

References

1. Protean, accessed from: https://proteantech.in/articles/ops-vs-nps-vs-ups-retirement-plan-em1822025/

2. India First Life, accessed from: https://www.indiafirstlife.com/knowledge-center/retirement-planning/difference-between-nps-and-ups

3. NPS Trust, accessed from: https://npstrust.org.in/weekly-snapshot-nps-schemes

4. PFRDA, accessed from: https://www.pfrda.org.in/web/pfrda/schemes/national-pension-system/unified-pension-scheme

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001