Anthropic Company Analysis 2026: Growth And Risks

Anthropic is gaining attention because its financial scale has changed sharply within a short period. The company behind Claude has moved from a fast-growing AI firm to one of the most closely watched private companies in the global technology market.

Anthropic’s latest funding round sharply reset its private market value. In May 2026, the company secured USD 65 billion through its Series H round, taking its post money valuation to USD 965 billion.1 Just three months earlier, its Series G round had brought in USD 30 billion at a USD 380 billion valuation.2

The jump shows that its valuation rose by nearly 154% within a short funding cycle.

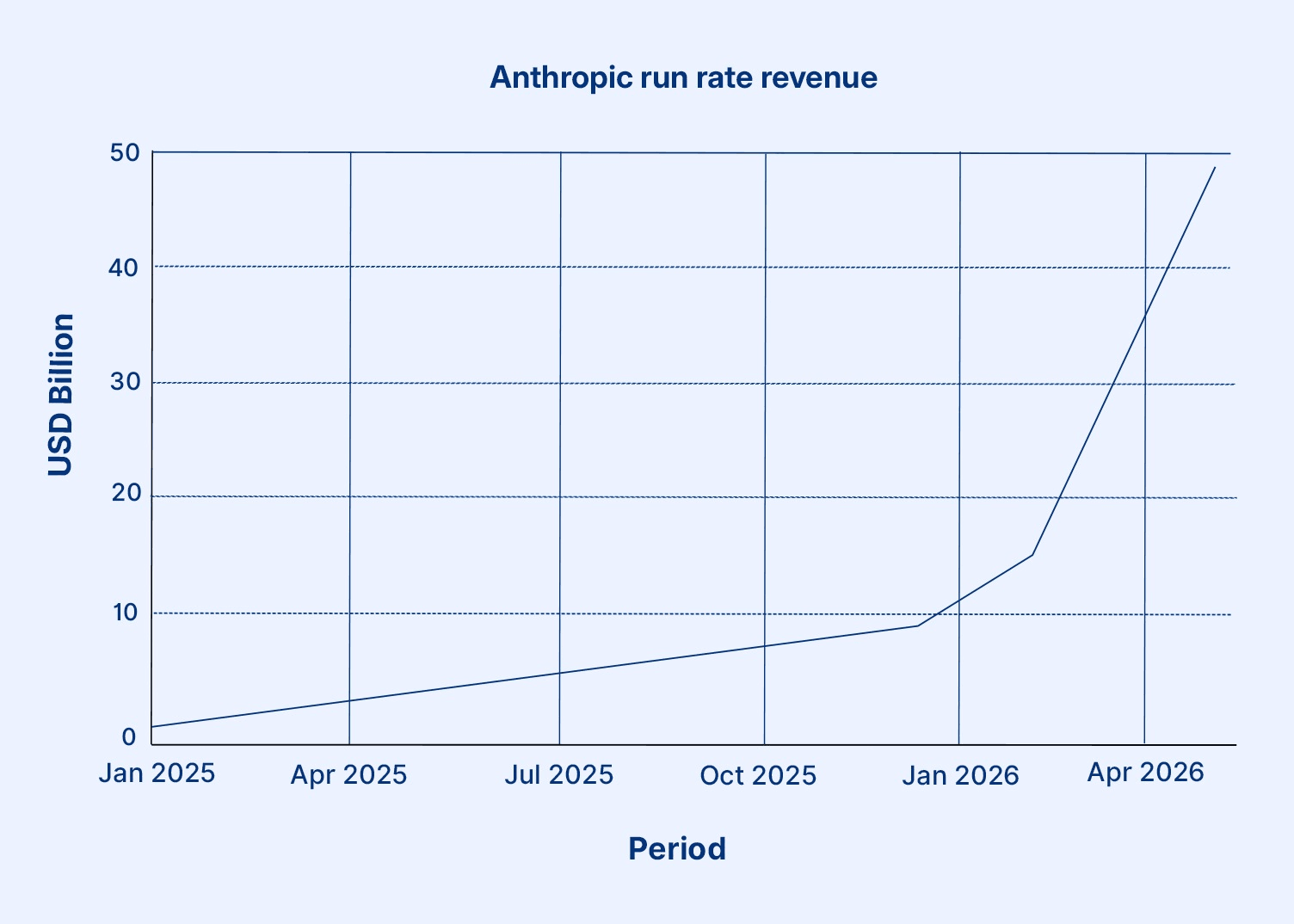

Revenue momentum gives the valuation story more weight. Anthropic’s run rate revenue stood at about USD 1 billion at the beginning of 2025 and crossed USD 47 billion in May 2026.3

Anthropic moved closer to the public markets on 1 June 2026 after submitting confidential paperwork for a planned United States listing.

This gives the story a strong market angle because investors are now watching how AI companies with large private valuations may perform under public scrutiny.4

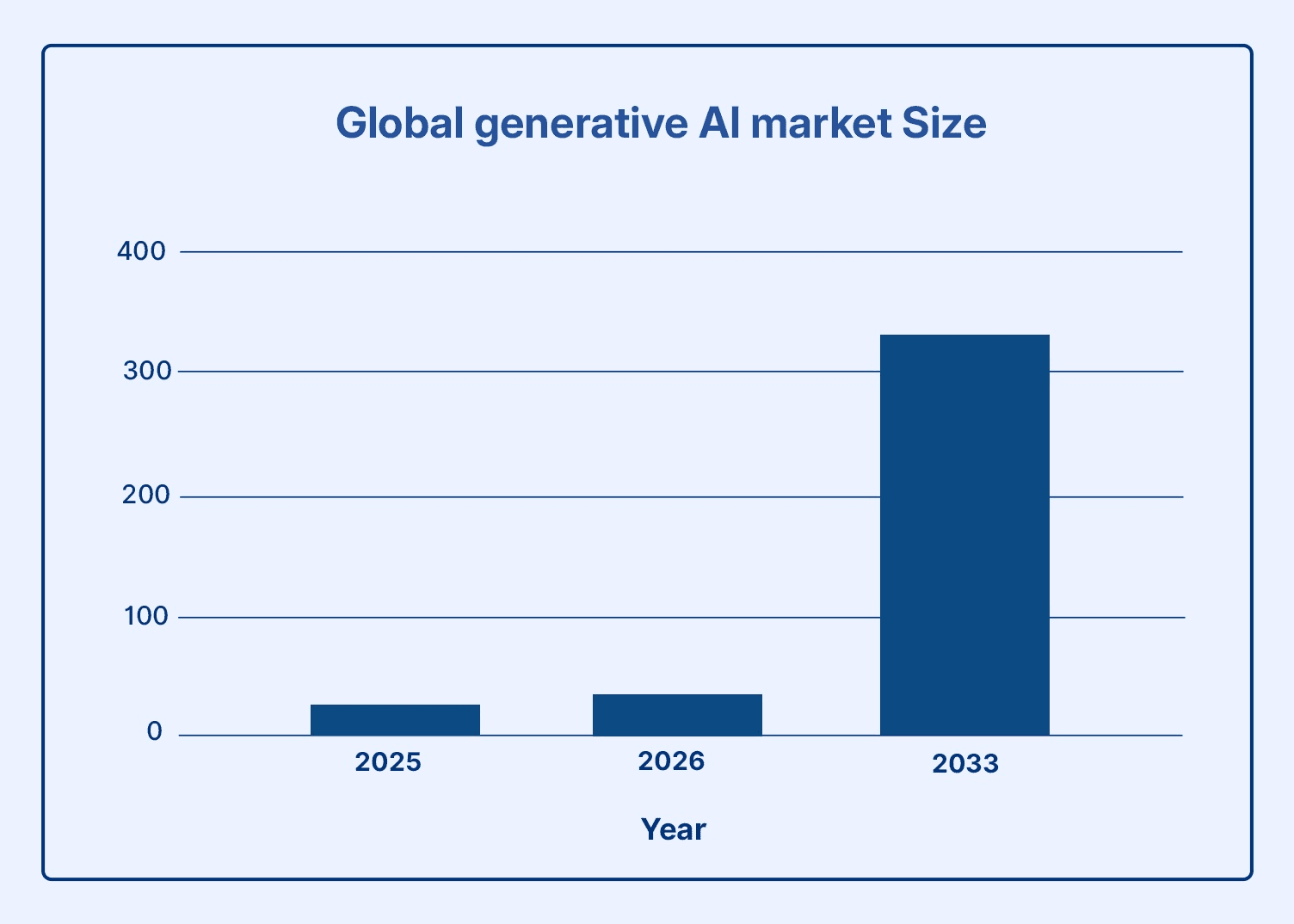

Source: Grand view research,5

The market setting supports the interest. The global generative AI industry is expected to grow from USD 29.6 billion in 2026 to USD 324.7 billion by 2033. For Anthropic company analysis, the larger question is whether Claude can convert that industry expansion into durable revenue.

Source: Grand view research,5

The market setting supports the interest. The global generative AI industry is expected to grow from USD 29.6 billion in 2026 to USD 324.7 billion by 2033. For Anthropic company analysis, the larger question is whether Claude can convert that industry expansion into durable revenue.

Anthropic Business Model: How Does It Generate Revenue?

Anthropic AI company generates revenue through Claude, its family of AI models and products. Claude supports writing, coding, research, analysis, customer service, document review, and internal business workflows.

The company does not rely on one income stream. Its model has several layers.

- Claude subscriptions: Individual users, professionals, and teams pay for access through plans such as Pro, Max, Team, and Enterprise.

- API usage: Developers and companies pay based on token consumption. Higher usage directly increases revenue.

- Enterprise products: Large firms use Claude with admin controls, governance features, and commercial data protections.

- Claude Code: Developers use Claude for coding, debugging, and software engineering tasks.

- Cloud distribution: Claude is available through large cloud platforms, which helps enterprise clients adopt it through existing technology arrangements.

API pricing shows how usage turns into revenue:

Claude model | Input cost per million tokens | Output cost per million tokens |

Haiku 4.5 | USD 1 | USD 5 |

Sonnet 4.6 | USD 3 | USD 15 |

Opus 4.8 | USD 5 | USD 25 |

This structure matters because business use can be heavier than casual use. A company using Claude across coding, customer support and internal research may generate repeated token consumption every day.

Enterprise trust also plays a commercial role. By default, inputs and outputs from commercial products such as Claude for Work, the Anthropic API and Claude Gov are not used to train models. That helps the firm sell into sectors where data control, auditability, and confidentiality matter.

Growth Drivers Behind Anthropic

Anthropic’s expansion comes from three main areas:

1. Enterprise Adoption

Customer growth has widened quickly. Anthropic served over 300,000 business customers by August 2025. The number of large accounts, defined as customers representing over USD 100,000 in run rate revenue, grew nearly seven times in one year.7

The upper end of the customer base is also expanding. Two years before February 2026, only about a dozen customers spent over USD 1 million annually. By February 2026, that number had crossed 500. Eight of the Fortune 10 were also Claude customers.8

2. Developer Demand

Coding is another meaningful engine. In May 2025, Anthropic opened Claude Code for broader use, giving developers direct access to its coding assistant. By August 2025, it had crossed USD 500 million in run-rate revenue. By February 2026, that figure had moved above USD 2.5 billion. Usage had grown more than ten times in three months by August 2025, and weekly active users had doubled since 1 January 2026.

3. Compute Partnerships

Compute access is the next driver. Advanced AI models need chips, cloud capacity, and large energy commitments. Anthropic has built capacity through partnerships rather than relying only on internal infrastructure.

Amazon's agreement added USD 5 billion in immediate investment, with up to USD 20 billion more linked to future milestones.9 This came on top of an earlier USD 8 billion investment. More than 100,000 customers were also building with Claude on a major cloud platform.

Another infrastructure arrangement gives Anthropic access to up to 1 million TPUs,10 with more than 1 gigawatt of capacity expected online in 2026. A separate agreement adds multiple gigawatts of next-generation TPU capacity from 2027.

These numbers show why the company is scaling quickly. They also show why Claude AI analysis remains capital-intensive.

Anthropic Valuation And Competitive Position

Anthropic’s valuation rise has been rapid. The numbers show how Anthropic investors' expectations have moved.

Date | Funding round | Amount raised | Post-money valuation |

Mar 2025 | Series E | USD 3.5 billion | USD 61.5 billion |

Sep 2025 | Series F | USD 13 billion | USD 183 billion |

Feb 2026 | Series G | USD 30 billion | USD 380 billion |

May 2026 | Series H | USD 65 billion | USD 965 billion |

From March 2025 to May 2026, the valuation rose by about 1469%. The pace creates both opportunity and pressure. A company valued close to USD 1 trillion has to deliver more than user growth. It must show stronger revenue quality, better margins, and customer retention.

Anthropic competes with OpenAI, Google, Meta, xAI and open source model providers. Its sharper edge lies in enterprise workflows, coding tools and safety oriented positioning.

The revenue multiple gives another lens. Based on USD 965 billion valuation and USD 47 billion run rate revenue, Anthropic trades at roughly 20.5x run rate revenue. This is not a profit measure. It only shows how much investors are paying for current revenue scale.

Now, can Anthropic keep attracting large companies while token prices fall and model performance becomes harder to differentiate? The firm’s enterprise traction is useful, but the AI market can shift quickly when lower cost models improve.

Risks For Anthropic

Anthropic has strong commercial momentum, but its risk profile is substantial.

1. Valuation pressure: A USD 965 billion private market valuation leaves little room for slower growth or weak margins.

2. Compute cost: Run rate revenue crossed USD 47 billion, but frontier AI needs expensive chips, cloud capacity, and energy.

3. Cloud reliance: Large partners provide scale, but they also create dependence on external infrastructure.

4. Competitive compression: If rival models become cheaper or open source alternatives improve, pricing power may weaken.

5. Regulatory scrutiny: AI safety, data privacy, cyber risk, and national security concerns can bring stricter rules.

6. Model misuse: AI systems can support fraud, cybercrime, and harmful automation if controls fail. For example, a recent model protection case involved more than 28.8 million exchanges through almost 25,000 fraudulent accounts between 22 April and 5 June 2026.11 The alleged activity centred on extracting model capabilities at scale.

AI Industry Outlook: Opportunity vs Risk

The broader AI market still offers considerable headroom. In 2025, 88% of surveyed organisations used AI regularly in at least one business function, compared with 78% in the previous year.13 The adoption curve is widening, but commercial value remains uneven.

Scale is the harder test. Nearly two-thirds of organisations had not expanded AI across the enterprise, while only about one-third had moved into broader implementation. For large model providers, this matters because occasional trials must turn into repeated workflow usage.

Agentic systems show a similar divide. Around 23% of organisations had scaled at least one agentic AI system, while another 39% remained in the experimentation stage.14 Even so, more than 40% of agentic AI projects may be cancelled by the end of 2027 due to high costs, uncertain returns, or weak control frameworks.

This leaves Anthropic with a balanced outlook. Demand is visible, budgets are rising, and business use is moving beyond simple chatbot activity into coding, analysis, and workflow support. The next test is whether these tools can deliver measurable returns at enterprise scale.

For market participants, artificial intelligence investment offers sizeable expansion potential, but its risk profile remains elevated. Allocation decisions, therefore, need discipline, not only exposure to emerging technology themes. One practical route is to combine AI-linked investments with corporate bonds, which may add income visibility and reduce dependence on a single growth sector.

Grip Invest can support this balance by giving access to curated debt-based opportunities within a wider investment plan.

Conclusion

Anthropic has emerged as one of the most valuable private AI companies, driven by rapid revenue growth, strong enterprise adoption, and increasing demand for Claude across business and developer use cases. Its expanding customer base, strategic infrastructure partnerships, and confidential IPO filing highlight the company's ambition to strengthen its position in the fast-evolving artificial intelligence market.

At the same time, Anthropic's near trillion dollar valuation brings significant expectations. Sustaining its growth will depend on its ability to maintain technological leadership, control infrastructure costs, and differentiate its products in an increasingly competitive AI landscape.

For investors, the company reflects both the immense opportunities and inherent risks associated with the AI sector. As with any high growth theme, building a diversified portfolio that balances emerging technology exposure with relatively stable income generating assets can help manage long term investment risk.

FAQs On Anthropic Company Analysis

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001