Best Fixed Deposit Plan In Post Office In 2026: Interest Rates, Benefits And How To Choose

In today's world of countless investment options, the Post Office Fixed Deposit (FD) continues to be a trusted choice for millions of Indians. The reason is simple when it comes to protecting your hard-earned money, safety and guaranteed returns often matter more than high-risk gains.

The Post Office Fixed Deposit Scheme, also known as the India Post Time Deposit Scheme, offers government-backed security, fixed returns, and flexible investment tenures, making it an ideal option for conservative investors.

Whether you're saving for your child's education, planning a major purchase, or building a secure financial future, it provides a reliable way to grow your wealth.

However, with 1-year, 2-year, 3-year, and 5-year tenure options available, choosing the best fixed deposit plan in post office can be challenging. This guide will help you compare the options, understand their benefits, and select the one that best aligns with your financial goals.

Let's explore everything you need to know before investing.

Best Fixed Deposit Plan in Post Office: Which Option Should You Choose?

The Post Office Fixed Deposit (FD) Scheme is a government-backed savings option that lets you invest a lump sum for a fixed tenure and earn guaranteed returns. Since the interest rate remains fixed throughout the investment period, it offers stability and is considered one of the safest investment options for conservative investors in India.

Currently, investors can choose from four different tenures:

- 1-Year Fixed Deposit

- 2-Year Fixed Deposit

- 3-Year Fixed Deposit

- 5-Year Fixed Deposit

Each tenure offers a different investment horizon depending on your financial objectives.

Features Of The Post Office Fixed Deposit Scheme

Before investing, it's important to understand how the scheme works.

1. Flexible Investment Tenures-Choose from 1, 2, 3, or 5 years, allowing you to match your investment with your short-term or long-term financial goals.

2. Minimum and Maximum Investment-You can start investing with just INR 1,000, and there is no maximum investment limit. Investors can also open multiple FD accounts.

3. Fixed Interest Rates-Interest rates are announced by the Government every quarter. Once you invest, your applicable interest rate remains fixed until maturity, ensuring predictable returns.

4. Competitive Interest Rates-Interest is compounded quarterly and paid along with the principal amount when the deposit matures.

5. Interest Payment-Although interest is calculated annually, it is compounded quarterly, helping investors earn better effective returns over time. The accumulated interest is paid along with the principal amount when the FD matures.

6. Premature Withdrawal Rules-Premature withdrawal is permitted after six months, subject to applicable conditions and reduced interest benefits.

7. Taxation-Interest earned is taxable as per your income tax slab. However, the 5-Year Post Office FD qualifies for tax deductions under Section 80C, subject to prevailing tax laws.

Always consider your tax liability before making an investment decision.

Features Of Post Office Fixed Deposit Across Different Tenures

Feature | 1 Year | 2 Years | 3 Years | 5 Years |

Minimum Investment | INR 1,000 | INR 1,000 | INR 1,000 | INR 1,000 |

Maximum Investment | No Limit | No Limit | No Limit | No Limit |

Government Backed | Yes | Yes | Yes | Yes |

Tax Benefit | No | No | No | Yes (Section 80C) |

Suitable For | Emergency Fund | Short-Term Goals | Medium-Term Goals | Long-Term Wealth & Tax Saving |

Which Post Office FD Tenure Is Best?

Choosing the best fixed deposit plan in the post office depends on why you're investing.

1-Year FD

Ideal for investors who need their money within a year or want to park surplus funds safely.

Suitable for:

- Emergency funds

- Short-term savings

- Conservative investors

2-Year FD

A balanced option for medium-short financial goals.

Suitable for:

- Vacation planning

- Vehicle purchase

- Home renovation

3-Year FD

A great option for investors planning expenses over the next few years.

Suitable for:

- Child's school admission

- Wedding planning

- Higher education fund

Suppose a family wants INR 8 lakh after three years for their daughter's college admission. Investing systematically in a 3-Year Post Office FD helps preserve capital while earning assured returns.

5-Year FD

The 5-Year Post Office FD is ideal for long-term investors seeking safety and tax savings. It offers:

- Tax deduction under Section 80C (subject to applicable laws)

- Guaranteed and stable returns

- Government-backed security

- Long-term wealth creation

If your goal is to build wealth while enjoying tax benefits, the 5-Year Post Office FD is a smart and reliable choice.

Post Office FD vs Other Fixed Income Investments

Before investing, compare the Post Office FD with other fixed-income options. They differ in returns, safety, liquidity, and tax benefits, helping you choose the investment that best suits your financial goals.

Investment Option | Expected Returns* | Safety | Liquidity | Tax Benefits |

Post Office FD | Moderate | Very High (Government-backed) | Moderate | Available only on 5-Year FD under Section 80C |

Bank FD | Moderate | High (DICGC Insured up to 5 Lakh) | High (With Penalty) | Tax benefits on select tax-saving FDs |

Moderate to High | Moderate | High (With Penalty) | No specific tax benefits | |

High | Varies with issuer rating | High (if listed) | Depends on the type of bond |

*Returns are indicative and may vary based on prevailing interest rates and market conditions.

Post Office FD vs Bank FD

Bank FDs offer features like online account opening, flexible payouts, and higher liquidity. However, Post Office FDs are government-backed, making them a safer choice for conservative investors.

Post Office FD vs Corporate FD

Corporate FDs may offer higher returns, but they also carry higher credit risk. In contrast, Post Office FDs provide guaranteed returns with greater capital safety.

Post Office FD vs Corporate Bonds

Corporate bonds can deliver better returns and liquidity but are exposed to market and credit risks. Post Office FDs are better suited for investors seeking stable, predictable, and risk-free returns.

Things To Consider Before Investing

1. Tax Implications

Interest earned is taxable as per your income tax slab. However, the 5-Year Post Office FD offers tax benefits under Section 80C, subject to applicable limits.

2. Liquidity Requirements

Premature withdrawal is allowed under certain conditions but may reduce your returns. Choose a tenure that matches your financial needs.

3. Inflation Impact

While Post Office FDs provide guaranteed returns, inflation can reduce their real value over time. Consider balancing your portfolio with inflation-beating investments.

4. Interest Rate Cycle

Post Office FD rates are revised quarterly for new deposits, but your interest rate remains fixed once you invest. Locking in a longer tenure may be beneficial when rates are expected to fall.

5. Your Financial Goals

Select a tenure based on your investment objective, whether it's saving for education, retirement, a home purchase, or building an emergency fund.

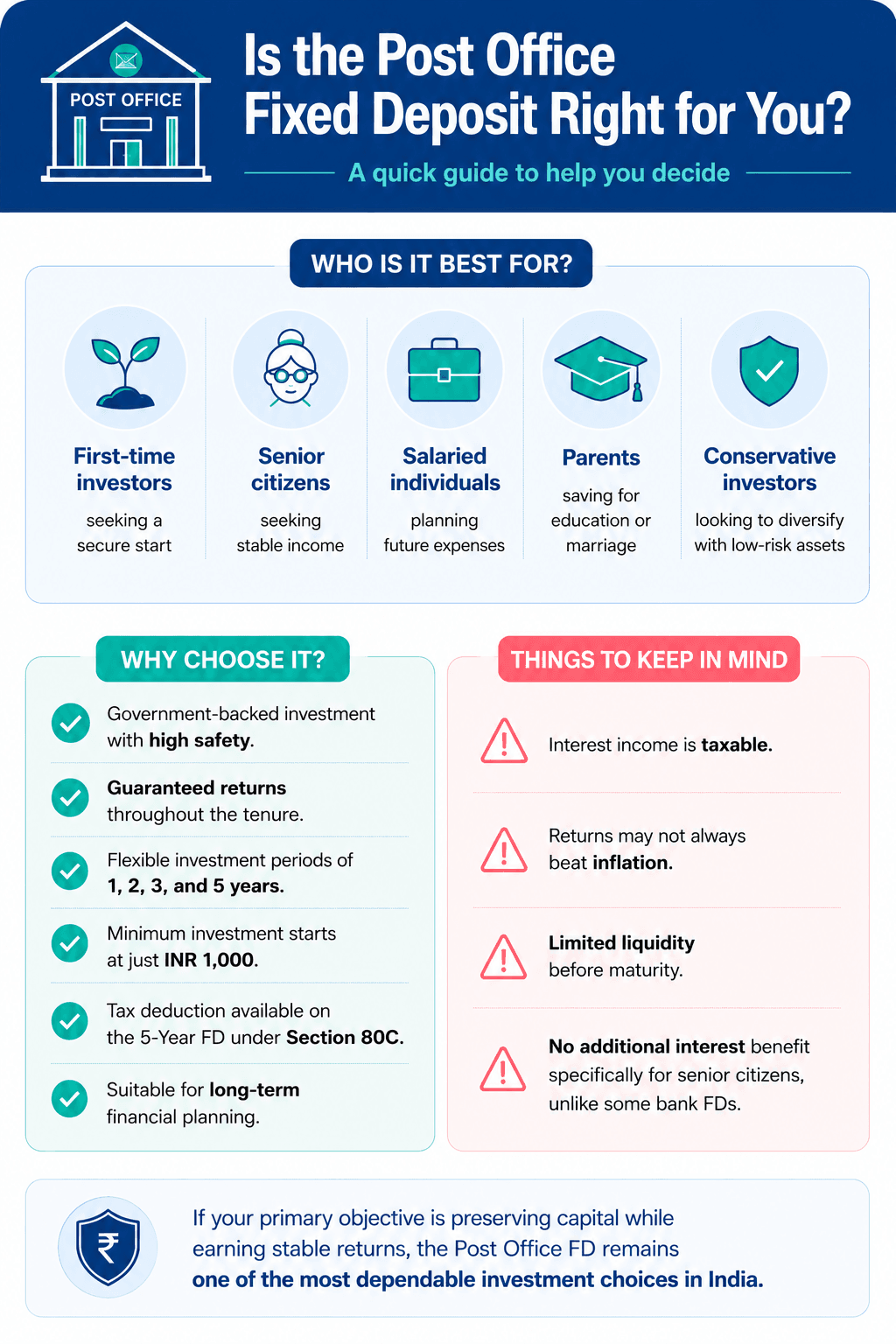

Is The Post Office Fixed Deposit The Right Choice For You?

The Post Office Fixed Deposit Scheme is ideal for investors seeking safe, stable, and guaranteed returns. It is best suited for:

- First-time investors looking for a secure investment.

- Senior citizens seeking stable income.

- Salaried individuals planning future expenses.

- Parents saving for education or marriage.

- Conservative investors looking to diversify with low-risk assets.

Pros

- Government-backed investment with high safety.

- Guaranteed returns throughout the tenure.

- Flexible investment periods of 1, 2, 3, and 5 years.

- Minimum investment starts at just INR 1,000.

- Tax deduction available on the 5-Year FD under Section 80C.

- Suitable for long-term financial planning.

Limitations

- Interest income is taxable.

- Returns may not always beat inflation.

- Limited liquidity before maturity.

- No additional interest benefit specifically for senior citizens, unlike some bank FDs.

If your primary objective is preserving capital while earning stable returns, the Post Office FD remains one of the most dependable investment choices in India.

Conclusion

The best fixed deposit plan in post office depends on your financial goals, investment horizon, and risk appetite. With government-backed security, guaranteed returns, and flexible tenure options, the Post Office Fixed Deposit Scheme remains a reliable choice for conservative investors.

While alternatives like bank FDs, corporate FDs, and bonds may offer different return potential, Post Office FDs stand out for their safety and stability. By choosing the right tenure based on your financial needs, you can build a secure and dependable savings portfolio with confidence.

FAQs On Post Office FDs

Author: Grip Invest Editorial Team The Grip Invest Editorial Team is a group of Chartered Accountants, MBA (Finance) graduates, and Qualified Research Analysts dedicated to helping you invest smarter. We dive deep into India's fixed income landscape to deliver content that is accurate, up-to-date, and easy to understand. Whether you're exploring bonds, fixed deposits, or other fixed income opportunities, our guides cut through the noise and give you the clarity to make better financial decisions. |

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001